Why Single Professionals in Toronto Fall Behind Financially

Quick Answer: Why Single Professionals in Toronto Fall Behind Financially?

Why do single professionals in Toronto still struggle despite earning a decent salary? Because one income now carries the full weight of rent, groceries, utilities, and transport with no one to split it with. Ordinary life in Toronto is priced around two incomes, not one. The problem isn’t carelessness. It’s structural.

Why doesn’t working harder fix it? Because extra hours bring marginal gains after tax while draining the energy you need to make smarter financial moves. For many single earners, the real path forward isn’t more force. It’s more leverage, through repositioning, skill-packaging, or redesigning fixed costs.

Can someone look successful and still be falling behind? Yes. Many single professionals in their 30s and 40s show up polished and pay the bills, while privately living month to month with almost no breathing room. The gap between how life looks and how it feels is where much of this stress lives.

Table of Contents

Mahnoor adjusted the throw pillow on a velvet sofa in the IKEA showroom and stepped back to look at the room she had just finished arranging. Everything was clean, balanced, and calm. The lighting worked. The storage worked. The flow worked.

A young couple nearby whispered to each other about how open the kitchen display felt. Mahnoor smiled and gave them the kind of answer she had learned to give after years of helping people imagine better homes for themselves.

“It’s not always about having more space,” she told them. “Sometimes it’s about using what you already have better.”

It was a good answer. She knew it was. She had spent years learning how to make rooms feel more functional, more breathable, more liveable. But the thought that waited for her after work was not breathable at all.

It was rent.

Mahnoor was in her early 40s, lived in the Greater Toronto Area, and had what many people would call a respectable job. She was also one of many single professionals in Toronto who look stable on paper but feel increasingly squeezed in real life. She worked hard, earned a decent salary, showed up professionally, and carried herself like someone who had built a stable adult life.

On paper, she looked fine. In reality, she was often living paycheck to paycheck in Toronto, despite doing what most people would consider all the right things.

In real life, she was often one difficult month away from panic. That gap between how life looks and how it feels is the real Toronto trap. It is where many single professionals in their late 30s and 40s now live: earning enough to look secure, but not enough to feel safe.

Why a decent salary no longer feels like enough

One of the most frustrating parts of modern urban life is that the language people use to describe income has not caught up with reality. A salary can still sound good in conversation while failing completely in practice.

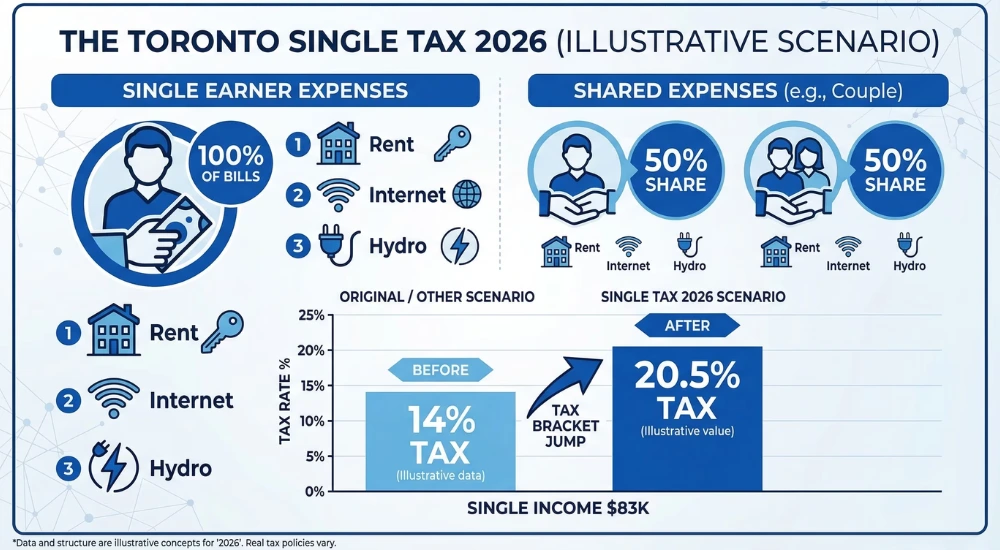

That is especially true for single earners in expensive cities. Rent, groceries, utilities, transport, internet, tenant insurance, professional appearance, occasional family obligations, and ordinary day-to-day expenses now hit one income stream with full force.

There is no second salary quietly absorbing half the fixed costs. That changes everything.

For single earners, the pressure is not just about rent and bills. Canada’s federal tax brackets also shape how much of each salary increase actually reaches their bank account.

For someone relying on a single income in Toronto, even a “reasonable” salary can start to feel thin once housing alone takes a large bite out of take-home pay. After that come groceries, hydro, transit, phone bills, and the dozens of smaller costs that never feel dramatic on their own but keep draining the account. Life becomes a steady sequence of payments rather than a platform for progress.

That is what many people still do not understand about single professionals living paycheque to paycheque. The problem is not always irresponsibility. Sometimes the problem is structural. Sometimes the problem is that one income is now expected to carry what urban life increasingly prices around two.

This is one reason many careful adults later find themselves feeling real financial pressure in their 50s in Canada, even though they were never reckless to begin with.

Monthly Stability Gap Calculator

Monetary Leaf Monthly Stability Gap Calculator

See how much room you really have left each month after covering essentials.

The hidden penalty of living alone

Mahnoor was not living wildly. She was not spending weekends buying designer bags or flying off for luxury getaways. Her spending was ordinary. That was exactly the problem.

Ordinary had become expensive.

Living alone often means paying 100% of costs that couples split without thinking about them. Rent is not shared. Internet is not shared. Hydro is not shared. Everyday household purchases are not shared. Even grocery efficiency changes when one person is buying and storing food alone.

Single people often pay more, proportionately, for less.

That does not make them victims. But it does mean the usual personal finance lecture about “just budgeting better” is often too shallow. Budgeting matters, but budgeting cannot fully solve a structural cost problem.

And yet many single professionals blame themselves anyway.

They assume they must be doing something wrong because they are tired, pressed, and still not moving forward.

That self-blame is one of the cruellest parts of the trap.

Why “working harder” stops working

For many people in Mahnoor’s position, the automatic solution is simple:

Work more.

Say yes more often.

Take on extra projects.

Stay useful.

Push harder.

Hope the next raise fixes everything.

That response is understandable. It also has limits.

The first problem is that extra effort often produces only marginal gain after tax. The second is that fatigue changes the quality of your judgement. When you are already stretched, more work does not always create more stability. Sometimes it just creates more exhaustion.

A person can be highly functional and still be quietly wearing down.

That is where many single professionals in Toronto get stuck. They are not lazy. They are not unserious. They are doing what responsible adults are supposed to do. But they are trying to solve a structural squeeze with sheer effort alone.

That works for a while. Then it stops working.

The real risk is not just burnout in the dramatic sense. It is slower than that. It shows up as chronic financial anxiety, decision fatigue, stopped savings, emotional flatness, poor sleep, and the feeling that life has become one long act of maintenance.

A person may still look polished, still deliver at work, still pay the bills most months, and still feel like they are slowly disappearing under the weight of ordinary life. That is the reality for many single professionals in their 40s who appear competent on the outside but feel increasingly cornered by the cost of ordinary life.

The immigrant version of the pressure

For someone like Mahnoor, there may also be another layer.

From a distance, her life may look successful to family and relatives. She has a professional job. She lives in Canada. She works at a recognised brand. She can send photos of a tidy apartment, a good office setup, a Toronto skyline view, or a well-presented workspace.

What those pictures do not show is the constant arithmetic underneath.

Many immigrants carry a silent burden of presentation. They do not always want to tell the full truth about financial stress because they fear sounding ungrateful, unsuccessful, or unstable. They feel pressure to appear established. They become curators of a life that is harder than it looks.

That silence can become expensive.

It cuts people off from useful conversations, practical support, and emotional honesty. It also deepens the false belief that everyone else is coping better.

So what actually helps?

This is the point where many articles become unhelpful. They either say “earn more” as if that is a light switch, or they drift into vague self-help. The better question is not whether Mahnoor should grow her income. She should.

The better question is how to grow it without sacrificing the little mental and physical capacity she has left.

The smartest path is not usually more hours. It is more leverage.

That means looking at your work life and asking:

- What do I know how to do well that other people struggle with?

- What do I repeatedly solve at work that could be turned into a service, guide, template, or process outside work?

- Which part of my skill set is actually valuable in the market, even if my current salary does not fully reward it?

- Which extra work would produce real upside, and which would simply eat my evenings for too little return?

That shift matters.

Mahnoor had spent years helping people think about layout, function, space, design logic, and better use of what they already had. Those are not small skills. But when people are stuck in financial survival mode, they often fail to see the market value of what has become normal to them.

That is why “working harder” is failing many single professionals in their 40s. They are adding effort without redesigning the earning model underneath.

Better ways to grow income without burning out

For someone like Mahnoor, income growth has to be strategic.

That could mean:

1. Turning repeat skill into packaged value

If you solve the same problem repeatedly at work, there may be a way to package that knowledge into:

- a digital guide

- a consultation offer

- a small paid service

- a niche freelance package

- a workshop or template

That kind of work has more leverage than simply trading more hours for more salary.

2. Repositioning rather than grinding

Sometimes the next income jump comes less from effort and more from role design. A person may need:

- a better employer

- a better title match

- a stronger salary negotiation

- a move into a more valuable niche

- a change from operational work to strategic work

That is not laziness. That is intelligent repositioning.

3. Cutting the wrong kind of side hustle

Not every side hustle is worth it. If something consumes evenings, drains concentration, and brings in too little, it may actually make the person poorer in the long run by damaging performance in the main job.

4. Redesigning fixed costs without shame

For some people, the biggest pay raise comes from reducing structural costs, not increasing income immediately. That may mean:

- changing neighbourhood

- changing housing arrangements

- renegotiating recurring expenses

- sharing certain costs

- questioning the prestige spending that comes with trying to maintain an image

This is not glamorous advice. It is real advice.

From survival to strategy

The real turning point for Mahnoor is not that she suddenly becomes rich. It is that she stops treating overwork as her only path out.

That mental change matters first.

When people are stuck, they often think in terms of rescue. They wait for a raise, a better month, a manager’s approval, lower grocery prices, or some future relief that will finally make life manageable.

A stronger approach is to become more deliberate.

Not frantic.

Not heroic.

Deliberate.

That means:

- knowing what your monthly floor really is

- knowing which costs are fixed and which are negotiable

- knowing which skills can become income

- knowing when extra work is helping and when it is simply consuming you

- protecting your energy because tired people make expensive decisions

Conclusion

Mahnoor’s problem is not that she is not working hard enough. Her problem is that hard work alone is no longer a complete plan.

That is the uncomfortable truth for many single professionals in Toronto and other expensive cities. A decent salary can still leave a person with no room to breathe. And when that happens, the answer is not always more force. Sometimes the answer is clearer design.

That may mean redesigning income.

It may mean redesigning costs.

It may mean redesigning expectations.

It may mean admitting that survival is taking too much out of you and that the current model is not working.

For many readers, this is not just about surviving the next rent cycle. It is also about learning how to recover financially in your 50s before years of pressure harden into permanent instability.

That is not failure. That is the beginning of a more intelligent way forward.

Frequently Asked Questions

Why do single professionals in Toronto still live paycheque to paycheque?

Because one income now often carries high rent, groceries, utilities, transport, and other fixed costs without the benefit of sharing them. A decent salary can still feel thin in a high-cost city.

Is working harder the best way to fix the problem?

Not always. Extra effort can help for a while, but if the underlying problem is structural, more hours may simply increase fatigue without creating real stability.

What is the smarter alternative?

Look for leverage. That means role repositioning, better pay strategy, packaging valuable skills, and reducing the fixed-cost pressure that keeps swallowing income.

Can this happen even if someone looks successful from the outside?

Yes. That is one of the most common and least discussed parts of the problem. Many people appear stable professionally while privately struggling to keep up with ordinary monthly costs.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.