Why Canadian Parents Still Financially Support Adult Children

Quick Answer: Why Canadian Parents Still Financially Support Adult Children?

Why do so many Canadian parents keep financially supporting their adult children? Because the cost of living has made it harder for young adults to become fully independent, and parents feel the strain up close. What starts as occasional help often becomes a quiet recurring pattern. Most parents don’t set out to fund their child’s lifestyle. They just keep saying yes one month at a time.

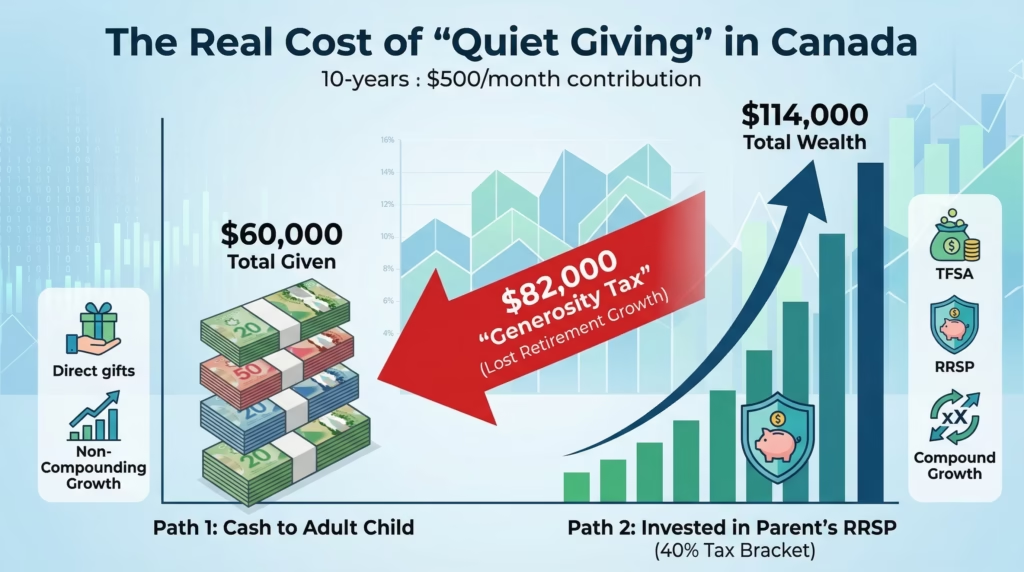

How much does “small” monthly help actually cost over time? More than most parents realise. Giving $500 a month for ten years isn’t just $60,000 in cash. It’s also the savings growth that money could have generated for retirement. The real cost of ongoing support isn’t the transfer itself. It’s what that money stops doing for your own future.

How do you set financial boundaries without damaging the relationship? By being calm, specific, and honest, not angry or accusatory. A good boundary doesn’t say “figure it out yourself.” It says “I can’t keep covering this, but I’ll help you build a plan.” That kind of clarity protects both the parent’s finances and the adult child’s growth.

On a quiet Sunday afternoon in Mississauga, Zainab looked down at her phone and felt the familiar tightening in her chest.

It was another message from her son.

Not a crisis. Not an emergency. Just one more gap to cover.

His rent was high. Car insurance had gone up. Groceries cost more than he expected. Payday was still a few days away. Could she send $300?

Zainab loved her son. That was not the problem.

The problem was that this kind of help no longer felt occasional. It had become part of the household rhythm. A transfer here. A top-up there. A phone bill. A grocery bill. An insurance payment. Each request looked manageable on its own, but together they kept nibbling away at money she and her husband were supposed to be setting aside for their own later years.

She wanted to help. She also wanted to retire with dignity.

That is where the real conflict begins for many parents. The hardest part is often not the amount itself. It is the guilt of saying no and the challenge of setting financial boundaries with adult children.

Sometimes the pressure goes even further: the parent is not only giving from savings, but working longer or returning to work to keep helping.

The New Reality of the “Bank of Mom and Dad” Canada

Zainab is not unusual. More and more parents supporting adult children in Canada are facing the same quiet pressure. Across Canada, supporting adult children financially has become much more common than many families are comfortable admitting. A TD survey released in late 2024 found that 57% of Canadian parents expected to continue supporting their children financially after adulthood, while 61% said they were not very confident in their ability to do so.

That matters, because it shows this is no longer just about generosity. It is also about pressure.

For many families, the support is not dramatic enough to look like a major financial event. It is quieter than that. It comes in the form of “just this once” transfers that keep recurring. A parent does not always feel like they are funding an adult child’s life. They feel like they are helping them get through a difficult month.

Over time, that pattern becomes one more reason many parents start feeling real financial pressure in their 50s.

The “Bank of Mom and Dad”: A 2026 Reality Check

Parents Are Still Carrying Financial Pressure

In a recent TD survey, 57% of Canadian parents said they expect to support their children financially after adulthood, while 61% said they are not very confident in their ability to do so.

The Long-Term Cost of “Small” Monthly Help

Even modest recurring support can create a serious opportunity cost. For example, a parent who gives $500 a month for ten years is not just giving away $60,000 in cash. They are also giving up the potential growth that money could have earned if it had remained invested for retirement.

Retirement Already Feels More Expensive

According to BMO’s 2026 retirement survey, Canadians now believe they need an average of $1.7 million to retire comfortably, and 14% say they plan to never retire. Source

But when difficult months become normal, so does dependency.

In expensive cities such as Toronto, Mississauga, Vancouver, and Victoria, it is easy to understand how this happens. High rent, transport costs, groceries, debt payments, and unstable career starts can leave even working adults financially stretched. Parents see that strain and feel compassion. Many also feel responsible, especially if they compare today’s cost of living with what they themselves faced decades earlier.

The emotional logic is understandable. The financial consequences are still real.

Why Small Monthly Help Is Not Always “Small”

One of the biggest mistakes parents make is thinking in monthly fragments instead of long-term totals.

A transfer of $300 or $500 may not feel life-changing in the moment, especially if the parent still has income coming in. But money has an opportunity cost. Every recurring amount that leaves your hands is money that is no longer strengthening your own financial position.

If a parent gives an adult child $500 a month for ten years, the direct out-of-pocket cost is $60,000. But the real cost may be much higher, because that money is no longer available for saving, investing, or preserving financial flexibility later in life.

This matters even more in a year like 2026, when Canadians say retirement feels more expensive than before. In BMO’s 2026 retirement survey, Canadians said they believed they would need an average of $1.7 million to retire comfortably, up from $1.54 million the year before.

That does not mean every household literally needs $1.7 million. It does mean many people already feel behind.

So when a parent keeps sending money to an adult child without clear limits, they may not just be giving help. They may be quietly reducing their own retirement margin, which is why retirement and adult children have become such a difficult financial balancing act for many families.

This is where guilt becomes dangerous. Guilt makes a parent look at one transfer. Good financial judgement makes them look at the pattern.

Two Different Households, One Common Pressure

The pressure does not look the same in every family.

In one home, there may be cultural expectations around family support, honour, and duty. A parent may feel that saying no is cold, disrespectful, or shameful. In another home, the pressure may come from a different place: a fear of watching a child struggle in an economy that looks far harsher than the one their parents entered.

The emotional packaging changes. The financial drain often does not.

A mother in Mississauga may feel pulled by family expectations and the instinct to protect. A retired teacher in Victoria may feel pulled by worry, guilt, and the fear that her daughter will never quite get stable footing. Both may tell themselves the support is temporary. Both may slowly absorb costs that their adult children should be learning to manage.

That is why the real issue is not whether parents should ever help. Sometimes help is right and necessary.

The real issue is whether the help is:

- occasional or ongoing,

- purposeful or automatic,

- stabilizing or dependency-producing,

- affordable or quietly corrosive.

That is the boundary line, and it is where healthy family financial boundaries begin.

When Helping Becomes Harmful

Financial boundaries are not only about protecting money. They are also about protecting roles.

A parent’s job is not to remove every difficult consequence from an adult child’s life. If parents keep cushioning every shortfall, adult children can remain emotionally and financially underdeveloped for longer than they realize.

For many households, setting clear limits is also part of learning how to recover financially in your 50s without sacrificing your own future.

That does not mean parents should become harsh. It means they should distinguish between support and substitution.

Support says: I will help you think through this.

Substitution says: I will keep stepping in so you never have to carry the full weight of your own life.

That second pattern may feel loving at first. Over time, it can produce resentment on one side and passivity on the other.

In many families, the parent starts to feel anxious every time the phone lights up. The adult child, meanwhile, starts to assume help is part of the system. Neither side likes the arrangement fully, but both adapt to it.

That is why saying no is often less destructive than continuing a pattern that quietly poisons the relationship.

How to Set a Boundary Without Turning It Into a Fight

The worst way to set a boundary is in the middle of resentment.

If a parent waits until they are already angry, frightened, or fed up, the conversation often comes out as accusation. The adult child hears rejection instead of clarity.

A better approach, especially when you are figuring out how to say no to adult children about money, is calm, specific, and grounded in reality.

For example:

“I love you, and I understand that things are expensive right now. But I cannot keep covering recurring expenses. I need to protect my own finances as well. I’m happy to sit down with you and look at options, but I’m not able to keep sending cash every time there is a shortfall.”

That kind of response does three useful things:

- it makes the boundary clear,

- it avoids humiliation,

- and it offers guidance without offering unlimited rescue.

For some families, a phased approach may work better than an abrupt stop.

For example:

“I can help with this expense this month, but after that I need you to take it over fully. Let’s plan now so it doesn’t become a recurring emergency.”

That gives the adult child time to adjust while still marking the end of the pattern.

Better Ways to Help, if You Truly Can Afford to Help

Some parents do have room to help. The question then becomes how to help wisely.

If the goal is long-term stability rather than monthly rescue, some forms of help are stronger than others.

Tax-Smart Generosity: A 2026 ‘Better Way’

If you have the means to help, the Canadian tax system offers more useful ways to support an adult child than sending repeated cash transfers for everyday bills.

1. The FHSA Gift (First Home Savings Account)

Help your child contribute up to $8,000 a year to their FHSA. It is a more purposeful form of support because it helps build a tax-free down payment asset instead of simply covering another monthly expense.

2. The MHRTC (Multigenerational Home Renovation Tax Credit)

Under CRA’s 2026 guidance, the MHRTC is 14.5% of qualifying renovation costs, up to a maximum of $7,250 per eligible claim.

For first-time home buyers, the FHSA remains one of the most useful tools. The CRA says FHSA participation room is generally $8,000 in the first year an account is opened, with contributions generally deductible and qualifying withdrawals tax-free for a first home.

That means helping an adult child build an FHSA may be more constructive than repeatedly covering lifestyle shortfalls that leave no lasting asset behind.

Similarly, if a family is considering multigenerational living, the MHRTC may be worth understanding properly. The CRA says the Multigenerational Home Renovation Tax Credit can apply to qualifying renovations that create a self-contained secondary unit for a senior or an adult eligible for the disability tax credit. For 2026 guidance, CRA states the credit is 14.5% of qualifying costs, up to a maximum of $7,250 per eligible claim.

That is important because many people still repeat the older 15% / $7,500 wording. For your article, I would use the current CRA figures, not the old ones.

In other words, if parents are going to help, the strongest help is often:

- structured,

- limited,

- linked to a real plan,

- and not disguised as endless household subsidy.

A Better Question Than “Should I Help?”

The wrong question is: “Should I help my child?”

Most parents already know the answer to that in their hearts. Of course they want to help.

The better question is: “What kind of help protects both of us?”

That question changes everything.

Sometimes the right help is money.

Sometimes it is budgeting.

Sometimes it is helping them compare insurance quotes, phone plans, bank fees, or housing options.

Sometimes it is saying, “I cannot fund this, but I will help you make a plan.”

That is not abandonment. That is adult-to-adult help.

Love Without Self-Erasure

Zainab’s real problem was never that she loved her son too much. It was that love, without a boundary, was turning into self-erasure.

Parents are not selfish for protecting their retirement, their savings, or their peace of mind. In fact, one of the kindest things a parent can do is avoid becoming financially dependent later because they gave away too much too soon.

A healthy boundary does not say, you are on your own and I do not care.

It says, I care about you, but I also have limits, and those limits matter.

That is a far more honest legacy than endless rescue.

Frequently Asked Questions

Is it wrong to say no when my adult child is genuinely struggling?

No. Saying no is not the same as being uncaring. The real question is whether your help is solving a short-term emergency or quietly turning into a long-term system.

Should I use my TFSA or RRSP to keep helping my adult child?

Not casually. Money withdrawn or not contributed is money that is no longer strengthening your own future. If support becomes routine, the long-term cost can be much larger than the monthly amount suggests.

What is a better alternative to repeated cash transfers?

A better alternative is often practical guidance with clear limits: a spending review, a timetable for taking over bills, or structured help aimed at savings or housing rather than ongoing rescue.

Is the FHSA a better way to help than paying everyday bills?

Often, yes. If the child is eligible and the family can afford it, helping with an FHSA may build something lasting rather than simply covering recurring shortfalls.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.