Older Canadians Earning Income to Support Their Adult Children

Quick Answer

A growing number of older Canadians are working past retirement, returning to work, or picking up new income not only to stay active, but because adult children are struggling with rent, groceries, childcare, and debt. This support often comes from love, but it can quietly erode retirement savings, affect OAS, CPP contribution choices, health, and family relationships. The pressure is real, the sacrifices are often hidden, and the financial rules around working after 65 are more complicated than most families realise.

🎧 Pressed for time? Listen to this summary that covers how older canadians earning income to support their adult children.

Gordon is up at 5:40 on a Tuesday in Hamilton. He fills his thermos, checks his knee brace, and laces up the same work boots he thought he’d retired three years ago. His phone buzzes on the counter. A text from his daughter, Meena: “Thanks again for the help last week, Dad. You’re the best. Hope you’re enjoying staying busy.”

He reads it twice, sets the phone face down, and pulls on his coat.

Meena thinks he took the hardware store job because he was bored after retiring from the municipal works department. He hasn’t corrected her. The truth is simpler and harder: her rent went up again, her son needs new winter boots, and the child care fees she’s covering on a contract salary don’t leave room for groceries by the third week of the month. The $800 he sends her each month isn’t coming from savings. It’s coming from his paycheque.

Gordon is one of a growing number of older Canadians earning income to support their adult children. Not from a pile of retirement money sitting in the bank. From new work. Early shifts. Sore joints. Labour traded for love, quietly, without complaint, and often without anyone in the family fully understanding what it costs.

Why Older Parents Keep Working

There are plenty of older Canadians who genuinely enjoy working into their sixties and seventies. They like the structure, the social contact, the sense of usefulness. Nobody should dismiss that.

But the numbers tell a wider story. According to Statistics Canada, the labour force participation rate for Canadians aged 65 and older hit a record 15.2% in 2025, representing roughly 1.2 million people. The average retirement age reached 65.4 years, up from lows near 60.9 in the late 1990s.

Some of that is personal choice. But Statistics Canada data from 2022 found that 21% of seniors aged 65 to 74 were working out of absolute necessity. And 5.2% of part-time workers in this group specifically cited “family responsibilities” as the reason for their work arrangement.

“I just like staying busy” is sometimes true. But it’s also a sentence that shields people from harder conversations. For some older parents, the real answer is closer to: “My daughter can’t make rent, and I’m the only backup she has.”

The Adult Child Pressure

This isn’t about adult children being lazy or entitled. It’s about an affordability problem that has moved from the housing market into family kitchens.

Youth unemployment (ages 15 to 24) reached 14.6% in mid-2025, a 15-year high according to Statistics Canada. Even for those with jobs, wage growth for younger workers was just 1.8% in early 2026, compared to 5.2% for workers 55 and older.

Meanwhile, CMHC and rental market data show that a one-bedroom apartment in Toronto averaged $2,156 a month in late 2025, requiring roughly 42% of after-tax income for a typical earner. In Ottawa, the same apartment ran around $1,600. In Calgary, over $1,500. In Vancouver, north of $2,000.

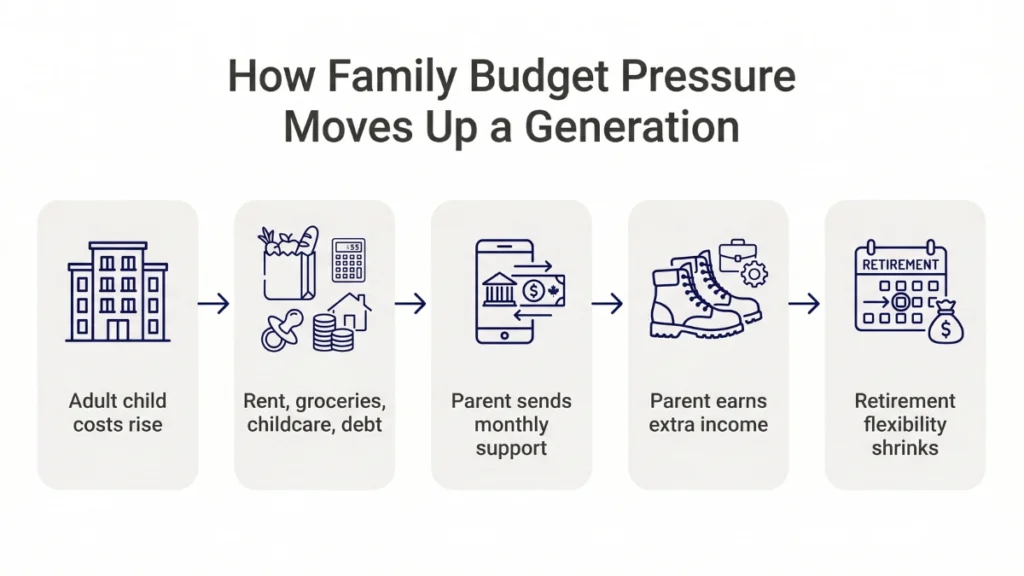

When adult children can’t cover rent and groceries on unstable contract work, the pressure doesn’t stay inside their apartment. It moves up a generation. And for many older Canadians earning income to support their adult children, the response isn’t a single cheque or a one-time gift. It’s a monthly transfer, sometimes for years, funded by work they thought they were finished doing.

What Extra Income Looks Like

The image of a retired parent “helping out” often brings to mind someone writing a cheque from a comfortable savings account. The reality for many families looks different.

Gordon works four shifts a week at a hardware store. His knees ache by noon. He used to walk his grandson to school on Wednesdays, but the shift schedule doesn’t allow it anymore. He hasn’t seen his physiotherapist in two months because the appointment times overlap with work.

Statistics Canada data shows that 90.1% of seniors holding multiple jobs work in service sectors: retail, health care, social assistance, and professional services. About 43,500 Canadians aged 65 and older are working more than one job.

For some, the work is part-time retail. For others, it’s consulting, seasonal jobs, freelance contracts, gig driving, or renting out a room. The work varies, but the pattern is the same: income that was supposed to be unnecessary is now essential, and the physical cost of earning it at 64 or 68 is higher than it was at 50.

Tired legs. Slower recovery. Less time for health appointments, rest, or the grandchildren the whole arrangement is supposed to be helping. The dignity of staying active and the exhaustion of needing to are not easy to separate.

The Retirement That Moved Away

What often starts as a short-term plan becomes a long-term reality. “I’ll just work one more year.” “Just until her lease renews.” “Just until the daycare bill comes down.” Each extension feels small. But the cumulative effect is large.

RBC survey data found that 33% of parents believe they’ll have to delay retirement specifically because they’re helping their adult children financially. And 36% worry that this support will permanently reduce their own retirement savings.

The arithmetic matters more at 65 than it does at 45. There’s less time to rebuild savings, fewer years to absorb a market downturn, and a smaller window before health needs start rising. A financial model cited in the research suggests that a 60-year-old spending $2,000 a month supporting adult children, instead of investing it at a modest return, could face a shortfall of roughly $155,000 by age 65. That’s not a rounding error. That’s three years of delayed retirement just to get back to even.

If you’re in your fifties and already feeling the squeeze, the article on how to recover financially in your 50s in Canada may be worth reading alongside this one.

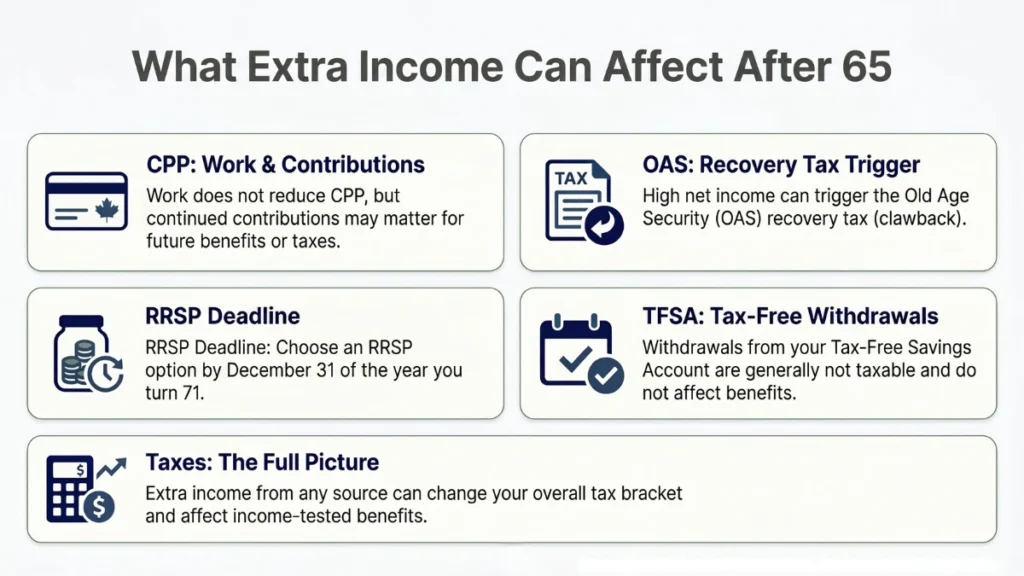

CPP, OAS, and Work

One of the most common questions older working Canadians have is whether earning income affects their government pensions. The short answer is: CPP is simple, but OAS has a catch.

You can work and collect CPP at the same time. Your CPP payments won’t be reduced because you’re earning a salary. However, if you’re between 60 and 65 and already receiving CPP, you’re required to keep making CPP contributions. These fund something called the Post-Retirement Benefit (PRB), a small additional monthly payment that starts the following year. Between 65 and 70, those contributions become optional. You can stop them by filing Form CPT30 with the CRA and your employer. At 70, contributions end regardless.

OAS works differently. There’s no penalty for working, but higher total income can trigger the OAS recovery tax. If your total net income crosses a certain threshold, the government begins recovering your OAS through what’s known as the OAS recovery tax, often called the OAS clawback. The money is typically deducted from your monthly OAS payments starting in July of the following year.

For the 2026 tax year, the research places the OAS recovery threshold at $95,323 in net world income. Once you cross that line, you repay 15 cents for every dollar above it. It’s worth confirming the exact threshold with CRA before making any decisions, because it adjusts annually.

The OAS Clawback Surprise

This is where things catch families off guard. A parent who takes on extra work to help a child with rent might not realise that the additional income, combined with RRIF withdrawals, pension income, or capital gains, can push them over the OAS threshold. The clawback doesn’t just apply to salary. It applies to total net income.

For example, a senior earning $105,000 in 2026, perhaps through a combination of consulting income and pension, would exceed the $95,323 threshold by about $9,700. That means roughly $1,450 in OAS repayment, deducted from monthly pension cheques starting the following July.

It’s not a devastating amount on its own. But for someone already stretching to help family, it’s another quiet cost that nobody warned them about.

What Extra Income Can Affect After 65

| Area | Why It Matters |

|---|---|

| CPP | No reduction for working. Contributions between 60 and 65 are mandatory. Between 65 and 70, optional. Creates Post-Retirement Benefit. |

| OAS | Not reduced by working directly, but total net income above $95,323 (2026) triggers the recovery tax at 15% of the excess. |

| RRSP/RRIF | RRSPs must convert to a RRIF by age 71. RRIF withdrawals count as taxable income and affect OAS clawback calculations. |

| TFSA | Withdrawals are generally not taxable and do not count toward OAS recovery tax calculations. |

| Taxes | Extra employment income can push you into a higher tax bracket, especially when combined with pension and RRIF income. |

The Sustainability Line

There’s a line between helping your child and quietly harming yourself. It’s not always easy to see, especially when the helping feels like the most natural thing in the world.

But the line exists. And it usually shows up in small, private ways: skipping dental appointments, eating less meat, letting a prescription lapse, pulling money from savings that were meant for the next decade. Sometimes it shows up as secrecy. A parent hiding the extent of what they’re giving from a spouse, from other children, or from themselves.

According to BMO research from late 2025, 45% of Canadian parents and grandparents plan to provide financial help to adult children in the next year. RBC data from 2024 shows that many grandparents supporting adult children are doing so at a cost to their own savings, with 54% giving at least monthly and 58% helping with everyday essentials like food and clothing.

When the support is monthly, when it’s funding groceries and rent rather than a one-time gift, and when the parent is earning the money through new work rather than drawing on existing wealth, the sustainability question becomes urgent.

Love doesn’t remove arithmetic. A parent who gives away $800 a month for five years has given away $48,000. If that money was earned through part-time shifts at 66, it also cost them time, energy, health, and flexibility they won’t get back.

If you’re trying to figure out where the line is in your own family, the article on financial boundaries with adult children goes deeper into that conversation.

Before It Becomes Resentment

The hardest conversation isn’t about money. It’s about honesty.

Gordon has never told Meena the real reason he’s working. She doesn’t know that his knee is getting worse or that he cancelled a fishing trip with his old crew because he couldn’t afford both the gas and the e-transfer. She doesn’t know he lies awake some nights wondering what happens when he can’t do the shifts anymore.

He’s not angry at her. He’s proud of her. But the silence is getting heavier.

The conversation doesn’t need to be dramatic. It might sound like: “I want to keep helping, but I need you to understand what this is actually costing me.” Or: “I’m working partly because of this support, and I need us to have a plan.” Or even: “I can’t rebuild this money later, and I’m starting to worry.”

It’s not about withdrawing love. It’s about making sure that the help has a shape, a timeline, and a shared understanding. Families that talk about money before resentment builds have a better chance of protecting both the parent’s retirement and the relationship itself.

Key Facts for Working Older Canadians

- Labour force participation among Canadians 65 and older reached a record 15.2% in 2025, representing approximately 1.2 million people (Statistics Canada).

- The average Canadian retirement age rose to 65.4 years in 2025 (Statistics Canada).

- 45% of Canadian parents and grandparents plan to provide financial support to adult children within the next year (BMO, 2025).

- Grandparents aged 55 and older provide an average of $6,945 annually to adult children aged 25 and up, with 54% giving at least monthly (RBC, 2024).

- For the 2026 tax year, the OAS recovery tax begins at a net world income of $95,323, according to Government of Canada pension figures. Readers should verify the current threshold directly before making decisions.

- TFSA withdrawals are not taxable and do not count toward the OAS clawback, making TFSAs a useful tool for parents providing family support.

The Family Budget Is Changing

Canadian retirement is becoming less of an individual milestone and more of a family project. The old model, where parents saved, retired, and occasionally helped with a down payment or a wedding, is giving way to something more ongoing: monthly transfers, shared grocery costs, grandchild expenses, and rent subsidies funded not by savings but by labour.

This pattern is connected to larger structural pressures. Rent has risen faster than young workers’ wages. Contract and gig work has replaced the stable jobs that once let people in their twenties and thirties stand on their own. Childcare costs remain high. And older Canadians earning income to support adult children are absorbing the overflow.

The evidence doesn’t point to one clean cause. It points to a pattern: older Canadians are working longer, younger Canadians are struggling with basic costs, and the family is absorbing what the economy can’t resolve. If you’re feeling the weight of that pattern in your own household, you’re not imagining it. The article on financial pressure in your 50s in Canada explores this from another angle.

None of this is a reason for despair. But it is a reason for honesty. The pressure on older parents isn’t personal failure. It’s a shift in what retirement looks like when the cost of living reshapes family life.

Gordon finishes his shift at 2 p.m. His back is tight. He sits in his truck for a few minutes before driving home, the way he always does now.

He doesn’t need to become hard. He doesn’t need to stop caring about Meena or her son. But he does need to stop pretending the work is only about staying busy. And Meena deserves the chance to understand what her father is actually doing for her, so the two of them can figure out what comes next together.

The problem isn’t that older parents love too much. The problem is that love is being asked to carry costs that used to be manageable through ordinary wages, affordable rent, and a working safety net. Clarity won’t remove that pressure. But it gives a family the chance to talk honestly before one person’s future is quietly spent keeping everyone else afloat.

At Monetary Leaf, we believe the calmest financial decisions start with the clearest view of what’s really happening. That’s worth more than any paycheque.

Frequently Asked Questions

Why are older Canadians still working past retirement age?

Some work because they enjoy it. But a significant number are working out of financial necessity, including the rising cost of living, gaps in retirement savings, and the need to support adult children and grandchildren. Statistics Canada found that 21% of seniors aged 65 to 74 were working by necessity, and the average retirement age has climbed to 65.4 years. For some families, the parent’s paycheque is the only thing keeping the household stable.

Can I earn income while collecting CPP and OAS in Canada?

Yes. CPP payments are not reduced by employment income. If you’re between 60 and 65 and already receiving CPP, you must continue contributing, which funds the Post-Retirement Benefit. Between 65 and 70, contributions are optional. OAS is different: while there’s no direct work penalty, your total net income can trigger the OAS recovery tax if it exceeds the annual threshold, which for 2026 is placed at $95,323 based on available government data.

Can I collect OAS and still work full time?

Yes, you can work full time and collect OAS. The pension itself is not reduced because you have a job. However, if your total net income from all sources, including salary, pension, RRIF withdrawals, and capital gains, crosses the OAS recovery threshold, you’ll repay a portion of your OAS at a rate of 15 cents per dollar above the limit. The repayment is usually deducted from your monthly OAS cheques starting the following July.

What is the OAS clawback threshold in 2026?

Based on the research used for this article, the OAS recovery tax threshold for the 2026 tax year is $95,323 in net world income. This threshold adjusts annually, so it’s important to check the current figure directly with the CRA or on the Government of Canada website before making any financial decisions.

When should parents stop financially supporting adult children?

There’s no single right answer. But it’s worth asking whether the support has become monthly and open-ended, whether it’s affecting the parent’s own health, savings, or retirement timeline, and whether the adult child has a realistic plan to reduce dependence over time. The goal isn’t to cut anyone off abruptly. It’s to make sure the help is sustainable, transparent, and understood by everyone involved.

How does supporting adult children affect retirement in Canada?

The effects can include delayed retirement, reduced savings, higher tax exposure through the OAS recovery tax, less flexibility for unexpected health costs, and emotional strain. RBC data suggests that 33% of parents expect to delay retirement because of family support, and 36% worry it will permanently affect their savings. When support is ongoing and funded by current work rather than existing assets, the long-term impact on the parent’s financial security can be significant.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.