Why Responsible People Feel Financial Pressure in Their 50s in Canada

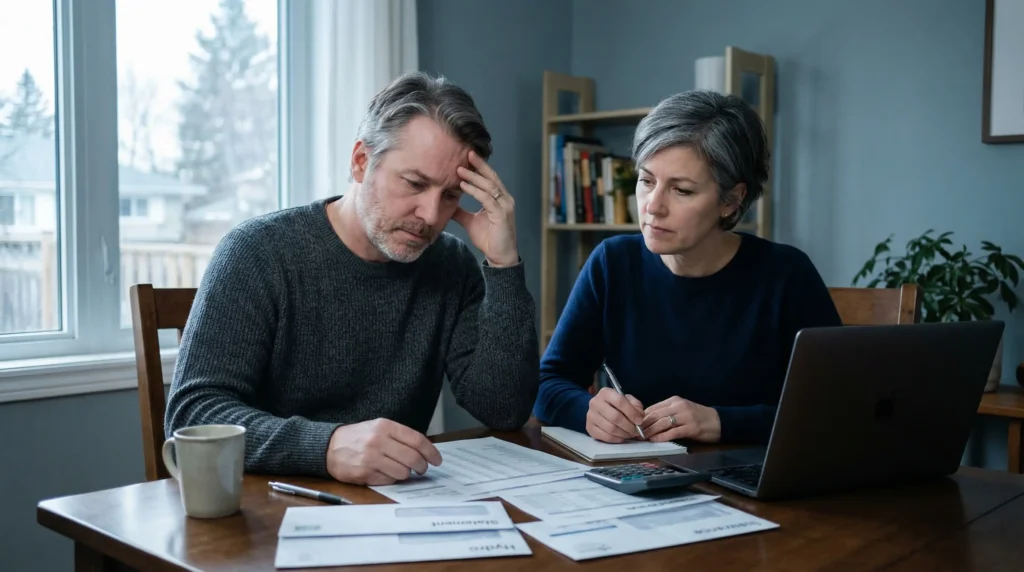

There is a kind of financial pressure in their 50s in Canada that rarely looks dramatic from the outside.

It does not always belong to people who were reckless or careless with money. More often, it belongs to those no one expects to struggle at all. People who worked steadily, paid their bills, avoided unnecessary risks, and believed that discipline would eventually lead to security.

In Canada, many people in their late 40s and 50s are now facing something unsettling: responsibility did not protect them in the way they thought it would. They built stable lives. They made careful decisions. They did what a responsible adult was supposed to do.

And yet, many now find themselves under pressure they never planned for.

Mortgage renewals feel heavier. Everyday costs rise faster than income. Supporting children and aging parents quietly stretches their finances. Retirement begins to feel less certain. That is what makes this experience difficult to explain.

Because when someone struggles after taking risks, the story makes sense. But when the people struggling are the ones who tried to do everything right, the outcome feels harder to accept.

This is not a story of failure in the usual sense. It is a story of people who followed the rules, only to realize the rules changed while they were still trying to live by them.

The Old Promise of Responsibility

For a long time, that belief felt reliable. There was a simple promise people trusted.

Work hard. Stay disciplined. Avoid unnecessary risks. Save what you can. Build slowly. It was not a promise of luxury. It was a promise of stability.

Many people built their entire lives around that idea. They chose steady careers over uncertain ones. They avoided debt where possible. They stayed consistent, even when progress felt slow. They made sacrifices quietly, believing that those sacrifices would eventually add up to something secure.

And for a while, that belief worked. Or at least, it felt like it did.

Because responsibility used to create direction. Even if life was not easy, there was a sense that things were moving forward. That effort mattered. That discipline had weight.

That is the version of responsibility many people still carry in their minds today. But the world that supported that promise has changed.

What Changed for Canadians in Midlife

When Ordinary Costs Stop Feeling Ordinary

What makes this moment so difficult is that many people did not suddenly become careless.

Their habits did not collapse overnight. Their values did not disappear. What changed was the world around them.

For much of the Canadian middle class, especially those moving toward retirement, financial insecurity no longer comes from obvious recklessness. It comes from ordinary life becoming more expensive than older assumptions allowed for.

For a long time, a careful person could trust the basic math of everyday life. If you earned a stable income, managed your spending, reduced debt, and saved consistently, there was usually a sense that your effort was building toward something.

Maybe not wealth. But at least stability. That sense has weakened.

Why Stability No Longer Feels Stable

Today, the pressure is quieter, but heavier.

Housing costs rise even after years of ownership. Mortgage renewals bring new uncertainty. Groceries, utilities, insurance, and everyday expenses slowly take a larger share of income.

Nothing feels dramatic on its own. But together, they shift the balance.

The house that once symbolized security starts demanding more just to maintain it. What changed was not only income, but the weight of ordinary life.

| Pressure Point | What Changed | Why It Matters |

|---|---|---|

| Inflation | Everyday prices rose quickly | Savings bought less than they once did |

| Mortgage renewals | Higher borrowing costs increased payments | Monthly cash flow tightened |

| Groceries and essentials | Basic living costs climbed steadily | Stable incomes felt weaker |

| Insurance and property costs | Homeownership became more expensive to maintain | Security started costing more |

| Family support | More adults in midlife supported children and parents | Retirement plans were pushed further back |

Savings that once felt sufficient begin to feel thin. Income that once covered everything now requires constant adjustment. What used to feel stable now feels fragile. And that is the kind of change responsible people rarely prepare for.

For many households, the pressure is no longer abstract. It now shows up in ordinary monthly math.

What makes this shift especially difficult is that it does not feel like a sudden crisis. There is no single moment where everything breaks. Instead, it feels like a gradual tightening. A little more pressure each year. A little less room to recover.

And because it happens slowly, many people keep adjusting quietly rather than stepping back and asking a harder question:

Has the system I trusted changed?

When Playing It Safe Quietly Becomes Expensive

The Hidden Cost of Feeling Safe

Most responsible people are taught to fear visible risk.

They are told to avoid volatility, avoid bad investments, avoid mistakes.

So they do.

They focus on protecting what they have. They keep money in places that feel secure. They avoid decisions that could lead to loss.

But while they are protecting themselves from visible risk, a quieter risk begins to grow in the background.

Their money stays still while life keeps getting more expensive. Their habits still feel careful, but the outcome becomes weaker over time.

When Caution Stops Creating Security

This is one of the most difficult truths for responsible people to accept: playing it safe can carry risk too.

For many Canadians in midlife, the pressure does not come from one dramatic mistake. It builds quietly through four overlapping forces.

This is where the difference between saving and investing starts to matter more, especially for people who spent years treating low-risk preservation as the safest path forward.

Not dramatic risk. Not the kind that creates headlines.

A slower risk. A quieter one.

The risk of becoming too defensive in a world that no longer rewards caution the way it once did.

In Canada, many middle-aged savers built their financial habits in a different environment. Avoiding debt, saving consistently, and staying conservative used to be enough.

But when money sits in places where it barely grows, while the cost of living continues to rise, safety begins to lose its meaning.

This is where purchasing power becomes an invisible force.

On paper, the numbers may still look stable. The savings account still shows a balance. Nothing appears to be “lost.”

But in reality, what that money can support is quietly shrinking.

The gap between financial appearance and financial reality slowly widens, often without being fully noticed until much later.

That is where safety becomes expensive.

The Behavioural Trap Behind Financial Stagnation

Why Loss Aversion Feels Responsible

At the center of this problem is not just economics. It is psychology.

People do not resist change because they are lazy. They resist it because change feels risky.

Loss aversion is powerful. The fear of losing what you have often feels stronger than the desire to grow it.

So people protect what they built.

They stay with what feels familiar. They avoid decisions that might disrupt their sense of control.

And in many cases, that feels like responsibility.

Anchored to an Older Economic Reality

But the environment has changed.

And behaviour often does not change as quickly as reality.

Many people remain anchored to an earlier version of how money worked. A time when inflation was lower, housing was more manageable, and steady employment felt more predictable.

They expect things to return to normal. They assume this is temporary. They wait.

In other words, risk aversion can feel responsible even when it slowly weakens long-term financial resilience.

That is where the trap deepens.

People continue making decisions that once made sense, without realizing those same decisions are now working against them.

Over time, these habits become part of identity.

People begin to see themselves as “careful,” “disciplined,” or “not the type to take risks.” That identity feels earned.

But it can also make change feel uncomfortable.

Because adjusting behaviour no longer feels like a financial decision.

It starts to feel like a personal one.

The Sandwich Generation Squeeze

I recently spoke with a friend, let’s call her Sarah, who perfectly illustrates this ‘quiet squeeze.’ Sarah is 52, lives in the GTA, and has always been the ‘responsible one.’ Last month, she found herself at her kitchen table with two tabs open on her laptop.

On one tab was her daughter’s university residence deposit, an amount that had jumped 15% since last year. On the other was a quote for her 85-year-old mother’s new home-care assessment. Sarah realized that in a single afternoon, her ’emergency’ savings were being pulled in two opposite directions. She wasn’t overspending on herself; she hadn’t bought new clothes in a year or taken a vacation. She was simply doing what we do: being the bridge between a generation trying to start their lives and a generation trying to finish theirs with dignity.

For Sarah, and for many of us, the stress isn’t about greed. It’s about the heart-wrenching math of trying to be a good daughter and a good mother at the same time, while watching your own retirement clock tick louder in the background

For many Canadians in midlife, financial pressure does not come from one direction.

It comes from both sides.

They are supporting children longer than expected. Helping with education, housing, or simply helping them get established.

At the same time, they are beginning to support aging parents. Whether financially, physically, or emotionally.

This is often called the sandwich generation.

But the reality behind that term is heavier than it sounds.

Because this responsibility is not optional. It comes from care, from values, from a sense of duty.

And that makes it harder to question.

Many people do not sit down and calculate what this support is costing them long term.

They simply give.

And over time, that quiet giving reshapes their own financial future in ways they may not fully see until much later.

Why 50 Feels Like a Breaking Point

When Time Stops Feeling Abstract

There is something about 50 that changes the emotional meaning of money.

At 30, there is time. At 40, there is pressure. But at 50, there is clarity.

The future no longer feels distant. It begins to feel measurable.

By this age, retirement savings, debt, housing costs, and health concerns begin to feel less theoretical and more connected to everyday reality.

That awareness changes how everything is viewed.

It is no longer just about managing the present.

It becomes about understanding the direction of the future.

The Emotional Weight of Midlife Financial Stress

Many people reach this stage and feel something they cannot easily explain.

Not failure. Not panic.

But a quiet unease.

A sense that despite doing many things right, the outcome does not match the effort.

There is also a quiet comparison that begins to happen.

People look at where they thought they would be… and where they actually are.

They remember earlier expectations. Earlier plans. Earlier timelines.

And even when life has been lived with sincerity and effort, that gap can feel heavier than any single financial number.

Because it is not just about money.

It is about meaning.

Responsibility Needs a New Definition

Responsibility itself is not the problem.

In many ways, it is still the foundation.

Discipline matters. Consistency matters. Avoiding unnecessary risk still matters.

But responsibility without adaptation becomes rigidity.

And rigidity, in a changing environment, becomes a risk.

The people who feel this most deeply are not reckless individuals.

They are the ones who followed the rules.

They are the ones who trusted the system.

They are the ones who believed that doing the right things would be enough.

What has changed is not their character.

What has changed is the environment those habits were built for.

And that means responsibility now requires something more.

Not abandoning caution.

But updating it.

Not rejecting discipline.

But expanding it.

Because the goal was never just to avoid mistakes.

The goal was always to build a life that could sustain itself over time.

The Sandwich Generation: A 5-Point Survival Checklist

Caring for aging parents and growing children simultaneously is a marathon, not a sprint. Use this checklist to protect your finances and your peace of mind.

- Audit the “Quiet Giving”: Track every dollar spent on adult children (rent help, phone bills) and aging parents (medication, home help). Seeing the total number helps you decide if it’s sustainable or if you need to set firmer boundaries.

- Secure the Legal Basics: Ensure your parents have an updated Will and Power of Attorney (for both health and property). Handling these before a crisis prevents expensive legal battles and emotional burnout later.

- Research 2026 Caregiver Credits: Check for federal and provincial tax credits like the Canada Caregiver Credit. These are designed to help you recover some of the costs associated with supporting a dependent relative.

- The “Oxygen Mask” Rule: Never stop your own RRSP or TFSA contributions to pay for a child’s discretionary expenses. Your children can borrow for an education; you cannot borrow for your retirement.

- Start the “Transparent Talk”: Sit down with your adult children. Explain the “New Midlife Squeeze” and discuss a timeline for their financial independence. Openness reduces resentment on both sides.

Conclusion

The idea that responsible people can still struggle financially is uncomfortable.

It challenges a belief many people were raised with.

That if you do the right things, you will be safe.

But the reality today is more complex.

Many people are not struggling because they failed.

They are struggling because the conditions around them changed faster than their habits did.

And until that truth is understood more clearly, many will continue blaming themselves for outcomes they were never fully equipped to control.

That is the quiet shift happening beneath the surface.

And it is one that deserves more attention than it usually receives.

Now that you understand the pressure, are you ready for the solution? Read my full guide:

How to Recover Financially in Your 50s (Even If You Feel Behind)

Frequently Asked Questions

Why are financially responsible people struggling in their 50s?

Many people in their 50s are not struggling because of poor decisions, but because the economic environment has changed. Costs like housing, groceries, insurance, and healthcare have risen faster than incomes. What used to be a stable financial plan no longer works the same way.

Is saving money still enough for financial security?

Saving is still important, but on its own it is often not enough anymore. Inflation reduces purchasing power over time, which means money sitting in low-growth accounts can lose value. A balance between saving and investing has become more important.

Why does financial pressure feel heavier after 50?

At this stage of life, financial issues become more real and urgent. Retirement is closer, income years are limited, and responsibilities like supporting children or parents may still exist. What once felt manageable starts to feel more serious.

What is the biggest financial mistake people make in midlife?

One of the most common mistakes is becoming too cautious. Many people stick to low-risk strategies that no longer keep up with rising costs. What once felt safe can slowly become a risk.

How can Canadians in midlife improve their financial situation?

The first step is awareness. Understanding that the rules have changed helps people adjust their strategy. This may include reviewing investments, managing expenses more actively, and making decisions based on today’s economic reality instead of past assumptions.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.