The Hidden Cost of Living in Canada: How Bills Quietly Drain You

Quick Answer: What is the cost of living in Canada?

Why does the cost of living in Canada still feel so high even after inflation slowed? Because prices don’t come back down when inflation cools. They settle at a new, higher floor. Electricity, water, insurance, internet, and subscriptions have all climbed since 2020, and those increases are now baked into every month. The squeeze isn’t one big bill. It’s dozens of ordinary charges that rose quietly and never reversed.

How much are Canadian households losing to bills they don’t even notice? More than most people think. Research suggests the average household underestimates subscription spending alone by about $130 a month. Add in loyalty-taxed phone plans, auto-renewed insurance, and forgotten cloud storage, and many families are quietly losing $1,500 to $3,000 a year to charges they haven’t reviewed in months.

What’s the most practical thing a household can do about it? Set aside one afternoon and go line by line through every recurring charge on your bank and credit card statements. Look for plans that have drifted above current market rates, subscriptions you’ve forgotten, and insurance renewals you accepted without comparing quotes. It’s not glamorous. But most households that do it find $100 to $200 a month they can claw back.

Priya noticed it on a Tuesday. She was standing at the kitchen counter in her Mississauga semi-detached, scrolling through her bank app while the kettle boiled. She wasn’t looking for anything specific. She just had that feeling again, the one where you know you haven’t done anything extravagant, haven’t booked a trip or bought new furniture, and still your chequing account looks thinner than it should by mid-month.

She tapped on her recent transactions. Hydro. Internet. Two streaming services. Insurance. Her daughter’s phone plan. A cloud storage subscription she forgot she had. The water bill from last quarter, auto-paid without her even opening the envelope. None of these charges were new. None of them were large enough, on their own, to explain the tightness. But together, silently, month after month, they were doing real damage.

That feeling Priya has, that quiet, creeping squeeze, is one of the most common financial experiences in Canada right now. And it has almost nothing to do with reckless spending.

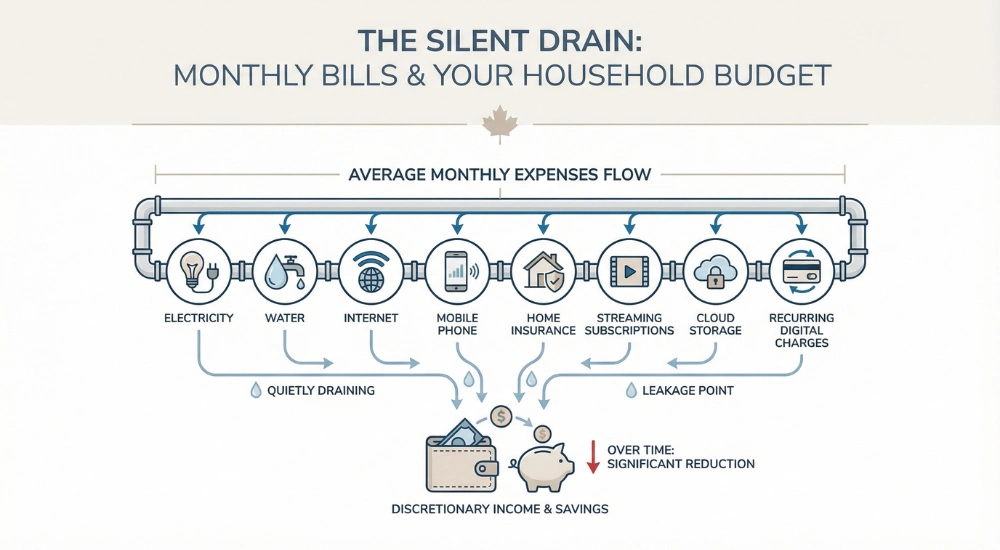

The cost of living in Canada has shifted in a way that doesn’t always show up in headlines. It’s not one dramatic bill that breaks a household. It’s the accumulation of dozens of ordinary, automated charges that slowly push a family’s budget past its limits. Most of these charges rise a little every year, and most of them are deducted before anyone sits down to think about them. That’s the mechanism. That’s the drain.

When The Numbers Don’t Match The Feeling

If you’ve been paying attention to official reports, you’ve probably heard that inflation has cooled. Grocery prices have stabilized somewhat. Interest rate cuts have begun. On paper, things should be getting easier.

But for households like Priya’s, two earners, two kids, a reasonable rent, no extravagant habits, the relief hasn’t landed. The reason is structural. Even when inflation slows down, prices don’t come back down. They settle at a new, higher floor. And recurring monthly expenses in Canada have been climbing that floor steadily for years, across almost every category that matters. [Related: Surging cost of ground beef].

Total household spending in Canada grew from roughly $1.16 trillion in 2020 to an estimated $1.59 trillion by 2024. Within that, utility and service costs have risen sharply: electricity spending grew by about 22.5%, water and sanitation by over 28%, and telecom services by nearly 24%. These aren’t luxury categories. They’re the cost of keeping the lights on, the taps running, and the internet working so your kids can do homework.

For Priya, the frustration isn’t about any single bill. It’s the way all of them rose at once and none of them came back down.

If you want the bigger picture behind this squeeze, read our article on why is everything still feels expensive in Canada even after inflation cooled.

The Bills That Set The Floor

Some monthly expenses are almost impossible to cut. Electricity, water, car insurance renewal and home insurance form the heavy base of any Canadian household budget, and all three have been climbing for reasons that have nothing to do with how much you personally use.

The average hydro bill in Ontario jumped significantly in late 2025 after the Ontario Energy Board approved a 29% increase in the regulated electricity supply cost. That increase was driven largely by a $648-million deficit that needed to be recovered from past energy costs, money the system had already spent but hadn’t yet collected. Even if your family used the exact same amount of power as the year before, you were paying roughly $15 to $25 more per month. The government offset some of this through the Ontario Electricity Rebate, but the net impact still landed.

In British Columbia, the pressure looks different but feels similar. BC Hydro’s rate increases of 3.75% in 2025 and 2026 are tied to the massive Site C dam project coming online, which triggered a 22.3% spike in depreciation costs that ratepayers now absorb. The average electricity bill in BC has been climbing not because people are using more power, but because the infrastructure behind it costs more to build and maintain.

Water bills are quieter still. Toronto raised water and sewer rates by 3.75% in 2026, pushing the average household’s annual cost above $1,100. In Calgary, the typical monthly metered water bill hit $119.21, a 3.76% increase. These charges often arrive quarterly, which means the increase is easy to miss until you add it up over a year.

Mortgage payments are one of the biggest examples of how a Bank of Canada rate hold can still leave households under pressure.

Home insurance is the one that’s been moving fastest. According to Ratehub, national home insurance inflation in Canada reached about 4% in early 2026, but in some provinces it’s far worse. Nova Scotia saw increases above 12%, driven largely by climate-related claims. Insurance is non-optional, usually auto-renewed, and rarely questioned, which makes it one of the easiest places for costs to rise without resistance.

Priya renewed her home insurance last spring without comparing quotes. She meant to shop around. She just didn’t get to it before the renewal date passed.

The Bills That Drift

If utilities set the floor, telecom and subscription costs are what slowly fill the room.

Canada’s wireless market has become more competitive in recent years, and the CRTC’s mobile wireless trends report shows significant price declines for several mobile plan baskets since 2020. That is real progress. But many households are still paying older rates because they have not switched plans, renegotiated, or compared current offers in a while.

This is what analysts call contract drift, and it’s essentially a loyalty tax. If Priya signed a $65-per-month plan in 2022, she might still be paying that same $65 in 2026, while new customers get twice the data for $25 less. The CRTC has introduced rules to reduce switching friction, including banning cancellation fees and requiring clearer plan summaries. But the responsibility to actually pick up the phone and negotiate still falls on the consumer. And most people, stretched thin by everything else in their week, simply don’t.

Then there’s the subscription layer. The average Canadian household now subscribes to roughly 3.5 video streaming services plus at least one music service, and that number keeps growing. Netflix, Disney+, Crave, Spotify, a news app, a cloud storage plan, maybe a fitness app or an AI tool, individually, each one seems modest. Together, they often rival the hydro bill.

Streaming prices have been climbing fast. Netflix moved from $20.99 to $23.99. Disney+ rose to $16.99. Apple TV+ jumped over 44% across two years to $12.99. And here’s the number that should stop every household in its tracks: the average Canadian is losing roughly $204 per year to subscriptions they don’t even use. Forgotten free trials that converted. Annual renewals that auto-charged. Shared accounts that nobody tracks.

Health costs can create the same kind of quiet pressure, especially for families comparing private health insurance in Canada for families without workplace benefits.

Research suggests that people estimate their monthly subscription spending at about $86, when the real figure is closer to $219. That gap, that invisible $130 per month, is one of the clearest examples of how living expenses in Canada have become harder to see, not just harder to pay.

How People Are Coping

What Priya does is what a lot of Canadian households are doing: adjusting quietly, without any formal plan, in ways that are practical but exhausting.

She’s shifted laundry and the dishwasher to after 11 p.m., when Ontario’s Ultra-Low Overnight rate drops to 3.9 cents per kilowatt-hour. It saves real money. It also means she’s folding clothes at midnight. She cancelled one streaming service, then re-subscribed when her kids complained, then cancelled a different one. She switched grocery stores twice in six months. Groceries are still one of the clearest weekly pressure points, and we explained that in more detail in our article on why are groceries so expensive in Canada.

Some of the most effective steps are less dramatic. Calling your internet or mobile provider and mentioning a competitor’s current bring-your-own-device rate can often trigger a retention offer. In 2026, with CRTC rules now banning cancellation fees, the leverage is better than it’s been in years. If a provider won’t match a $45-per-month plan with 50GB of data, switching your number can be done in minutes using eSIM.

For electricity, checking which pricing plan you’re on matters more than most people realize. Ontario now offers three options: Time-of-Use, Tiered, and Ultra-Low Overnight. A household that can shift heavy usage to nighttime hours, running the dryer, charging an EV, using the oven, can cut supply costs dramatically. It won’t erase a 29% rate hike, but it softens it.

For subscriptions, some households have adopted a hard cap: no more than a set number of recurring digital services, or no more than 2% of net income going to subscriptions. The rule is simple, if you want to add something, you have to cancel something first.

On insurance, increasing your deductible from $1,000 to $5,000 can meaningfully lower your premium. It means you’re self-insuring against small claims, which is a trade-off, but with premiums rising at double the pace of general inflation, it’s a trade-off more people are making.

None of this is glamorous advice. It’s the kind of thing you do on a Sunday afternoon with a cup of coffee and your laptop open, and it can easily save a household $1,500 to $3,000 a year.

Where Monthly Bills In Canada Quietly Drain The Budget

A bills audit becomes easier when you stop looking at the month as one blur and start looking at the categories that quietly keep pulling money out of it.

| Bill category | Why it quietly gets expensive | What to review |

|---|---|---|

| Electricity / hydro | Rate increases, fixed charges, and pricing plans that no longer suit the household | Check your current pricing plan, heavy-usage timing, and whether your usage pattern has changed |

| Water / sewer | Quiet annual increases and quarterly billing make the cost easy to overlook | Check the annual trend, billing cycle, and whether higher seasonal use is pushing up the total |

| Internet | Promotional pricing expires, and old plans often become poor value over time | Compare your speed and price with current market offers and call before renewal periods |

| Mobile plans | Older plans may stay expensive even as better market offers appear | Review data usage, device financing, and current competitor plans |

| Home insurance | Auto-renewals and premium increases often go unchecked | Compare quotes before renewal and review deductible options |

| Streaming and digital subscriptions | Small recurring charges fade into the background and pile up over time | Cancel unused services, check annual renewals, and look for overlapping subscriptions |

| Cloud storage, apps, and add-ons | These often stay on autopilot long after the original need has passed | Review bank and card statements for low-visibility recurring charges |

| Other recurring household services | Device protection, memberships, and service fees often continue without review | Ask whether the service is still useful and whether it still earns its place in the budget |

Why This Isn’t Your Fault

There’s a reason the squeeze feels personal even when it isn’t. Recurring bills are designed to be invisible. Automatic payments remove the moment of decision. Digital transactions eliminate the tactile sense of money leaving your hands. And when a charge repeats often enough, your brain stops registering it as a cost at all, it becomes background noise, like the hum of a fridge.

For recently arrived families, choosing the best bank for newcomers in Canada can also affect monthly fees and first-year cash flow.

Behavioural research confirms this. Payment decoupling, the gap between using a service and feeling the cost, weakens our sense of spending. Automated renewals push the transaction out of sight entirely. Studies suggest that buy-now-pay-later users are over 22% more likely to make a purchase simply because their “current balance” feels higher than it truly is once future obligations are counted.

This isn’t a failure of character. It’s a design feature of modern billing.

At the same time, the structural costs behind these bills, aging electrical grids, climate-driven insurance claims, massive infrastructure projects, are being passed through to households on fixed schedules that most people never see coming. Utility companies recover past deficits through rate adjustments. Insurers price in wildfire and flood risk across entire provinces. Telecom providers count on the fact that most customers won’t call to renegotiate.

For households trying to decide what to do with their next savings dollar, it also helps to understand how RRSP Canada actually works before locking money away.”

The system relies on passivity. And passivity isn’t laziness, it’s what happens when you’re already stretched thin by the hundred other demands of ordinary adult life.

The Weight Of It

Something that doesn’t get talked about enough is how tiring this is. Not the individual bills, the vigilance. The sense that keeping your head above water now requires a level of attention that used to be optional. Priya doesn’t feel poor. She feels heavy. Like running the household has become a second administrative job that nobody trained her for and nobody pays her for.

A 2025 financial stress survey found that roughly 48% of Canadians couldn’t cover three months of expenses in an emergency. Among adults aged 35 to 54, the definition of financial wellness has shifted from building wealth to simply paying off debt. That shift tells you something. People aren’t dreaming about retirement portfolios. They’re just trying to get the monthly obligations under control.

The shame is quiet. It shows up as avoiding conversations about money with a partner. It shows up as a vague feeling that you should be doing better, even though you can’t point to anything you’ve done wrong. It shows up in the way people describe their finances online, not with panic, but with a kind of worn-down resignation. The recurring theme isn’t desperation. It’s fatigue.

If that sounds familiar, it’s worth hearing clearly: the problem is real, it’s structural, and it’s affecting millions of Canadian households at once. You’re not behind because you failed to pay attention. You’re navigating a system that was built to avoid your attention. This kind of monthly pressure is not limited to families. We explored a similar pattern in our piece on why hard working single professionals in Toronto still keep falling behind financially.

What Comes Next

The honest outlook is mixed. Headline inflation has cooled, which helps at the margins. Telecom prices continue to drop for new plans, which means there are genuine savings available for anyone willing to make a phone call. The CRTC’s consumer protection measures are slowly adding friction for providers and reducing it for customers. Federal banking fee reforms are also making basic accounts cheaper.

But electricity costs in Ontario and BC are unlikely to retreat. The infrastructure investments driving those rate hikes are long-term commitments that will be recovered over years, not months. Home insurance premiums will keep rising as long as climate-related claims do, and there’s no sign that trend is reversing. And the subscription economy is still expanding, AI tools like ChatGPT Plus are now entering household budgets as a new category of recurring cost that didn’t exist two years ago.

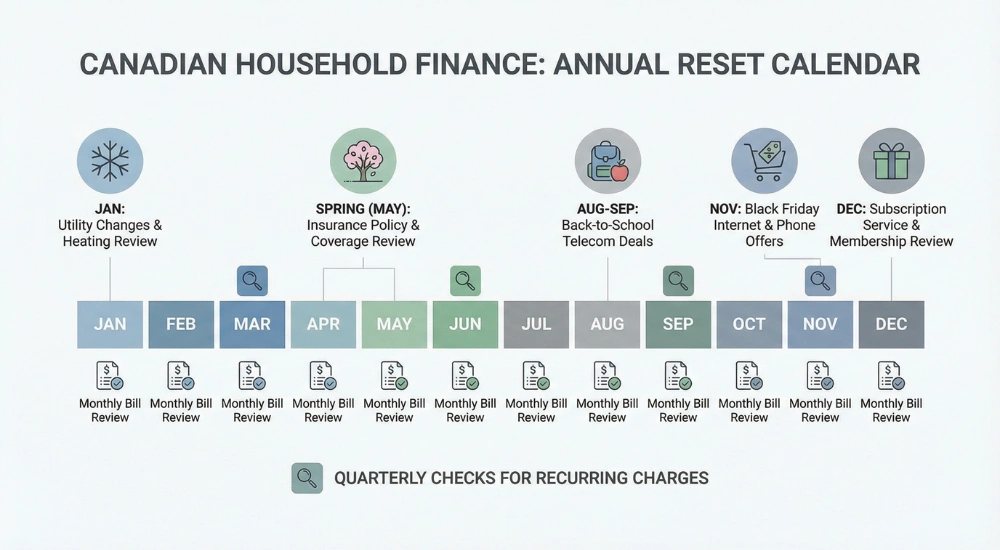

The baseline cost of ordinary life in Canada is higher than it was, and it’s likely to keep climbing in specific, predictable categories. The households that will feel steadiest are the ones that build a habit of reviewing their recurring costs at least once a year, ideally timed to the market. November, during Black Friday promotions, is the strongest window for telecom negotiations. January is when utility rates reset. February and March are the time to shop insurance before spring renewals land.

It doesn’t require a spreadsheet or a financial advisor. It requires one weekend a year where you sit down and look.

Self-employed workers feel this pressure differently when personal health insurance Canada becomes another monthly cost replacing old workplace benefits.

You’re Not The Problem

Priya eventually did the audit. She sat down one Saturday in November, opened every account, and went line by line. She found a cloud backup plan she hadn’t used in two years. She found a mobile plan that was $22 more than the current market rate for the same data. She found an insurance premium that had risen 9% without a single claim. In total, she identified just over $170 a month in costs she could reduce or eliminate. That’s more than $2,000 a year.

She didn’t feel proud, exactly. She felt something closer to relief. And a little anger, at how long it had taken her to see it, and at how easy the system made it to not see it.

If the cost of living in Canada has taught us anything in the last few years, it’s that financial pressure doesn’t always arrive as a crisis. Sometimes it arrives as a slow, quiet accumulation of charges you never consciously agreed to increase. The reality has changed. Your worth hasn’t. Your intelligence hasn’t. You just need one clear afternoon to look at what’s actually leaving your account, and decide what gets to stay.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.

Frequently Asked Questions

Why does the cost of living in Canada feel so high even though inflation has slowed down?

Inflation measures the rate of price increases, not the price level itself. Even when inflation cools, prices settle at their new, higher floor. Recurring monthly costs like electricity, insurance, water, and subscriptions have all climbed significantly since 2020, and those increases don’t reverse when inflation slows. The squeeze people feel is real, it’s the cumulative weight of a higher baseline that hasn’t come back down.

How much are Canadians actually spending on subscriptions without realizing it?

Research suggests that the average household estimates their subscription spending at about $86 per month, but the real figure is closer to $219. The gap comes from forgotten free trials, auto-renewed annual plans, and shared accounts that nobody tracks closely. Canadian households lose roughly $204 per year on subscriptions they don’t actively use.

Is it worth calling my internet or phone provider to negotiate a lower rate?

Yes, and 2026 is a particularly good time to do it. Wireless prices have dropped significantly in recent years, but many customers are still on older, more expensive plans. Since June 2024, providers can no longer charge fees for cancelling or switching, which gives you real leverage. Mentioning a competitor’s current rate during a retention call often triggers a better offer.

Why did Ontario hydro bills jump so much in late 2025?

The Ontario Energy Board approved a roughly 29% increase in the regulated electricity supply cost in November 2025, primarily to recover a $648-million deficit from past energy costs. The government partially offset this through an increased rebate, but most households still saw a net increase of $15 to $25 per month. The rise wasn’t driven by higher personal usage, it was a system-level cost recovery.

What is the single most effective thing I can do to reduce my monthly bills?

Set aside one afternoon, ideally in November when telecom deals are strongest, and review every recurring charge on your bank and credit card statements over the past three months. Look for subscriptions you’ve forgotten, plans that have drifted above market rates, and insurance renewals you accepted without comparing quotes. Most households that do this find $100 to $200 per month in costs they can reduce or cut entirely.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.