Why Your Car Insurance Ontario Went Up Again in 2026

Ontario car insurance premiums rose 8.2% in 2026, even as inflation cooled to 1.8%. Here’s the real reason your renewal keeps climbing.

Quick Answer: Why Your Car Insurance Ontario Went Up Again in 2026?

Why does car insurance in Ontario keep rising even though inflation has cooled? Because car insurance premiums aren’t tied to grocery prices or gas. They’re driven by claims costs, and those have surged. Modern vehicles are far more expensive to repair, stolen cars that are never recovered trigger full replacement payouts, and the regulatory system works on a delay. The increase hitting your mailbox now is the system catching up to damage from two years ago.

Will the July 2026 reforms actually lower my premium? They might, but only for some drivers. The new modular system lets you waive certain optional benefits like income replacement and death coverage. If you already have strong employer-provided insurance, there could be savings. But the reform also shifts first-payor responsibility to your auto insurer, which adds cost to the mandatory base. For many households, the two forces may roughly cancel each other out.

What can Ontario drivers actually do to pay less? Shop around every renewal cycle, even if you’ve been loyal to your insurer for years. Use a licensed broker, raise your deductible if you can absorb the risk, ask about telematics pricing, bundle home and auto, and claim every discount you’re entitled to. None of it is dramatic, but together these steps can keep an extra $80 to $100 a month in your pocket.

🎧 Pressed for time? Listen to a summary of the heart of this story. Full data and guidance are detailed in the article below.

Mark checks the mail on a Tuesday evening in late March. His twelve-year-old is doing homework at the kitchen table, his wife is heating up leftovers, and for a moment the house feels like it’s humming along the way it should. He flips past the flyer for a pizza chain and finds the envelope from his insurer. He already knows what it is. He opens it standing up, coat still half on.

His car insurance renewal has jumped again. Eight-point-something percent, printed in plain black ink. He does the math quickly: between his Civic and his wife’s RAV4, they’re looking at close to six hundred dollars a month for two cars in Mississauga. He puts the letter face-down on the counter.

Just last week, he’d seen a headline that CPI had cooled to under two percent. He remembers feeling a flicker of hope. Maybe things were finally levelling off. Maybe the grocery bill would stop its slow, stubborn climb. Maybe the next renewal would hold steady. He was wrong about the renewal.

And he’s not the only one confused. Across Ontario, drivers are opening similar letters and asking the same question: if inflation is supposedly under control, why does car insurance Ontario households depend on keep getting more expensive?

When Inflation Cools but Your Premium Doesn’t

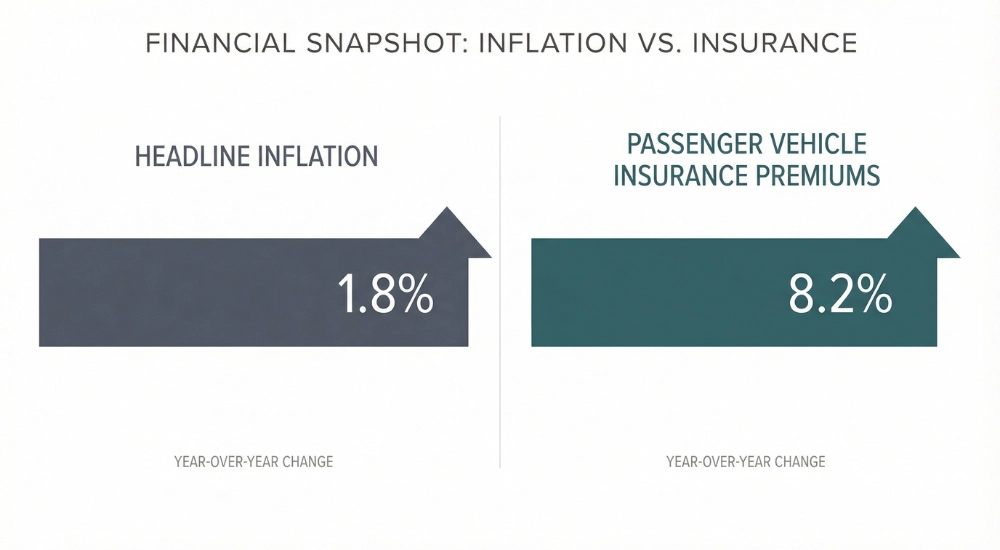

In February 2026, Statistics Canada reported that headline consumer price index inflation had settled at 1.8 percent year-over-year. After several brutal years of price hikes on food, housing, and fuel, a figure below two percent was supposed to feel like a turning point.

But car insurance in Ontario didn’t follow the trend. During the exact same twelve-month window, passenger vehicle insurance premiums across Canada rose by 8.2 percent. And that’s not a one-year spike. Since late 2020, the cumulative increase in vehicle insurance costs nationally has been nearly nineteen percent.

For households like Mark’s, this creates a painful gap between what the news says and what the bills say. Car insurance rates in Ontario have moved so far ahead of general inflation that the two numbers barely seem related. And it’s one of the few bills you can’t simply decide to skip. If you drive in Ontario, you pay.

What Modern Vehicles Actually Cost to Repair

One of the biggest factors pushing auto insurance rates higher is the changing nature of the cars themselves.

The shift toward advanced driver-assistance systems, radar units behind the front grille, ultrasonic sensors in the bumpers, cameras mounted near the rearview mirror, has turned even a small fender bender into a significant repair event. A decade ago, backing into a post might mean a new bumper and a paint job. Today, the same tap can misalign a cross-traffic radar sensor and shatter a camera bracket. The repair invoice isn’t just for bodywork anymore. It now includes diagnostic scans, sensor recalibrations, and hours of specialist labour using factory-level equipment.

Industry data puts the average cost of a repairable physical damage claim at roughly five thousand dollars. That’s a national figure, not a worst case. And vehicle parts and maintenance costs across Canada have risen more than twenty percent compared to 2019.

Mark drives a relatively modest car. But the technology inside it isn’t modest. Even a Civic now carries features that would’ve been considered high-end ten years ago. The same safety systems that are supposed to protect families are making every small collision considerably more expensive to fix. That cost doesn’t stay with the body shop. It flows into the claims pool, and from there, straight into premiums.

Why Fewer Thefts Haven’t Lowered Premiums

You’ve probably heard that auto theft in Ontario dropped significantly. That’s true. In 2025, the raw number of vehicle thefts fell by twenty-two percent, dropping to about 19,300 reported incidents. That’s a real decline, driven by enforcement crackdowns, port monitoring, and the growing use of physical tracking devices.

So why hasn’t it shown up in premiums?

Because the number of cars stolen is only half the story. The other half is how many come back. In Ontario, only fifty-one percent of stolen vehicles are recovered. The rest are shipped overseas by organized criminal networks or stripped for parts. When a vehicle is never found, the insurer doesn’t pay for a bumper repair. They pay out the full replacement value, which, for the SUVs and trucks these groups prefer, can run forty to sixty thousand dollars.

At the national level, auto theft claims cost insurers more than $360 million in the first half of 2025 alone. Even with the decline in frequency, the sheer replacement costs of unrecovered vehicles keep theft losses high. And comprehensive coverage handles more than just theft. It also covers weather damage, glass breakage, and wildlife collisions. The cost to replace a modern windshield, the kind with embedded safety cameras, has climbed so steeply that repair inflation inside the comprehensive pool is absorbing much of whatever savings the drop in theft numbers might have offered.

Mark heard on the radio that car thefts were down. He assumed his premium might hold. It didn’t.

Why You’re Still Paying for 2023 Damage in 2026

There’s a mechanical reason auto insurance rates in Ontario don’t respond to the economy the way grocery prices or gas prices do. The system is built to move slowly.

Under provincial law, insurers can’t simply raise prices when they want to. They must submit detailed actuarial rate filings to the Financial Services Regulatory Authority of Ontario, known as FSRA. The data that supports those filings comes from the General Insurance Statistical Agency, which processes historical claims from across the industry. The cycle is long. The benchmarks being used in 2025 and 2026 filings are based on validated data from as far back as late 2023 and 2024, a period when parts costs were at peak inflation and supply chains were still recovering.

What this means in practice is that the premium increase hitting Mark’s mailbox this March is the insurance system catching up to repair bills that were already paid out two years ago. And looking ahead, FSRA’s own actuarial guidance projects future collision loss trends growing at somewhere between 6.6 and 10.6 percent annually. There is little sign that this pressure is easing yet.

This regulatory lag also explains why premiums don’t drop the moment theft statistics improve or headline inflation cools. The system doesn’t work in real time. It works on a twelve- to twenty-four-month delay, which means the pressure that built up during the worst years is still being processed and passed through to drivers. On top of that, accident frequency has returned to pre-pandemic levels as roads have gotten busy again. When you combine that normalized volume of collisions with the inflated cost of every repair, the total payout pool grows quickly.

The July 2026 Benefit Reforms

On July 1, 2026, Ontario is rolling out a significant change to the way auto insurance benefits are structured in the province. The system is moving from a one-size-fits-all statutory accident benefits model to a modular, pick-and-choose approach.

Under the new rules, medical care, rehabilitation, and attendant care remain mandatory. But a long list of supplementary benefits, income replacement, caregiver benefits, death benefits, funeral benefits, and several others, will become optional. If you sign a written declaration, you can waive them.

For families who already carry solid workplace disability insurance and life insurance through an employer, this could be a genuine opportunity to shed duplicate coverage and trim the premium. And for some, it likely will help.

But there’s a catch that may cancel out the savings. The reform also designates the auto insurer as the first payor for medical and rehabilitation claims. Until now, if you were injured in a crash, your employer’s extended health plan would often absorb the initial costs before the auto policy kicked in. Under the new structure, that order flips. The auto insurer pays first.

Insurers will have to price that exposure into the mandatory portion of the policy. There’s a real chance that the cost added by first-payor liability offsets whatever a driver saves by opting out of the supplementary benefits. The net result for the average cost of car insurance in Ontario could end up being close to a wash, or, for drivers who waive coverage they actually needed, something worse.

Mark hasn’t read the details yet. He’s seen a mention of it in the news, something about being able to customize your coverage. It sounded promising. But no one has explained the trade-offs in plain language. And the consequences of waiving income replacement, for someone without a strong employer disability plan, could be serious after a bad accident.

For a plain-language walkthrough of the coverages, renewal notice terms, OPCF codes, and broker questions, read our Ontario car insurance survival guide 2026.

The Newcomer Premium Gap

Ontario receives more newcomers than any other province, and for many of them, car insurance is one of the first and most disorienting financial shocks after arrival.

Insurance pricing in Ontario is heavily driven by localized Canadian driving experience and your postal code. A skilled professional who arrives in the GTA with fifteen years of clean driving in another country can still be quoted three or four thousand dollars a year, simply because they have no Canadian record. The system treats them as unknowns, and unknowns get sorted into the highest risk brackets.

FSRA has issued guidance encouraging insurers to recognize foreign driving experience from certain countries, but the practical friction is still high. Processing international records takes time, and not every insurer accepts them the same way.

This financial pressure makes newcomers especially vulnerable to ghost broker scams. Fraudulent operators offer suspiciously low rates, collect cash or electronic transfers, and issue counterfeit policies that look legitimate but provide zero actual coverage. A newcomer involved in a collision while holding a fake policy faces not only the physical damage, but also the legal consequences of driving without valid insurance in Ontario.

Practical Steps That Can Help

If your car insurance costs in Canada have become a source of quiet dread, there are a few things worth trying. Not miracles. Just moves that can shift the number.

The first is to actually shop around, even when it feels pointless. Many Ontario drivers assume their insurer is giving them the best rate because they’ve been loyal. That’s rarely how it works. Get at least three quotes every renewal cycle. Use a licensed broker, not just online aggregators. Brokers can sometimes access smaller carriers or group rates that don’t appear on comparison websites.

The second is to look hard at your deductible. Raising it from five hundred to a thousand dollars can meaningfully reduce your premium. It means more out-of-pocket risk in a collision, but for drivers with clean records who are primarily concerned about the monthly cash flow, the math often works in their favour.

Third, ask about every available discount. Usage-based insurance, where a telematics device tracks your driving habits, can lower your rate if you’re a calm, predictable driver. Bundling home and auto policies with the same company still produces real savings in most cases. Winter tire discounts are available from many Ontario carriers and are sometimes overlooked.

Fourth, pay attention to the July reforms. If you carry strong employer-provided disability and life insurance, you may benefit from opting out of some newly optional coverages after July 1. But don’t waive anything before reading the fine print and understanding what your workplace plan actually covers.

And fifth, watch out for ghost brokers. If anyone offers you car insurance at a price that seems dramatically lower than every other quote, that’s a warning sign, not a deal. Legitimate policies come through licensed brokers and licensed insurers. You can verify a broker’s licence directly through FSRA’s public registry.

These aren’t magic fixes. They won’t erase the structural pressure. But for someone like Mark, keeping an extra eighty or a hundred loonies in his pocket every month would take some of the serious sting out of that renewal letter.

Why the Pressure Isn’t Personal

It’s easy to feel like you’re doing something wrong. Like maybe you picked the wrong car, or live in the wrong neighbourhood, or missed some trick that everyone else figured out. Mark has had that thought more than once. He’s a careful driver. He’s never filed a claim. And still, the bill goes up.

The reality is that car insurance premiums in Ontario are being pushed upward by forces that have nothing to do with individual behaviour. The vehicles themselves have become more expensive to repair. Organized theft networks still extract large payouts from the system. Fraud, from staged collisions to falsified claims, adds hundreds of millions to insurer losses every year, and that cost is spread across every policyholder. Severe weather events are pushing reinsurance costs higher globally, and that pressure eventually flows into local premiums.

And the regulatory structure, by design, creates lag. What you’re paying today reflects damage that happened years ago. The system doesn’t adjust in real time. It absorbs shocks slowly and passes them forward.

Car insurance isn’t rising because you’re failing at money. It’s rising because the whole ecosystem, parts, labour, technology, crime, regulation, reinsurance, has shifted to a higher cost floor. Lower inflation elsewhere in the economy hasn’t changed that, and it may not close the gap any time soon.

What Comes Next

The honest answer is that meaningful relief is unlikely in the near term. FSRA’s actuarial projections point to ongoing collision loss growth in the range of 6.6 to 10.6 percent per year. Repair costs aren’t retreating. Vehicle technology is only becoming more complex. The first-payor shift in July 2026 adds a new layer of cost into the mandatory base coverage.

There are some bright spots. The decline in raw theft numbers is real, and if recovery rates improve even modestly, the severity drag could start to ease. Greater adoption of telematics-based pricing could eventually reward lower-risk drivers more meaningfully. And the modular benefit structure, once it settles, might give some households real flexibility, provided they make informed choices about what to keep and what to waive.

But the broader reality is that car insurance in Ontario is unlikely to return to what it cost in 2019. The cost floor has moved. The best anyone can do is make informed decisions within the system as it exists, and not blame themselves for the gap between the headline number and the bill in the mailbox.

Before You Go

If you’ve been staring at a renewal notice and feeling like the ground shifted without anyone telling you, you’re not imagining it. The cars got more expensive to fix. The thefts got more costly to settle. The regulation moves slowly. And the bill lands in your hands, every year, without much explanation.

You’re not bad with money. You’re not missing some obvious hack. You’re dealing with a cost increase that was years in the making and is still working its way through the system. It is one more example of how the cost of living in Canada can keep rising in ways that headline inflation does not fully capture.

Take the time to shop your renewal. Look at your deductibles. Read the fine print on the July changes. Protect yourself from scams. And give yourself a break. The cost of car insurance Ontario families are carrying has changed, but that doesn’t mean you’ve lost your grip on your finances. It means the financial ground changed under people’s feet.

Frequently Asked Questions

Why is car insurance in Ontario still rising even though inflation has slowed down?

Car insurance premiums are tied to claims costs, things like vehicle repair bills, theft payouts, and medical expenses, not to grocery prices or gas prices. Those claims costs have risen sharply in recent years due to more complex vehicle technology, expensive parts, and organized theft. Because of regulatory lag, the premium increases hitting households now are still catching up to damage from 2022 to 2024. Headline inflation and insurance inflation operate on different timelines.

How much does car insurance cost in Ontario on average?

The average cost of car insurance in Ontario depends heavily on where you live. In Toronto, the average annual premium in 2025 was close to four thousand dollars. In Ottawa, it was about twenty-five hundred. Premiums in suburban rings around the GTA tend to sit somewhere in between. Your driving record, vehicle type, postal code, and coverage choices all affect the final number.

Will the July 2026 insurance reforms lower my premium?

They might, but only if you understand what you’re giving up. The new modular system lets you waive certain benefits like income replacement or death benefits. If you already carry strong employer-provided disability and life insurance, you could save money. But the reform also shifts first-payor responsibility to your auto insurer, which adds cost to the mandatory base. For many drivers, the savings and the added cost may roughly cancel out.

Why don’t fewer car thefts lead to lower premiums?

Because the financial damage from theft isn’t just about how many cars are stolen, it’s about how many are never recovered. In Ontario, roughly half of stolen vehicles are never found. When that happens, the insurer pays the full replacement value instead of a small repair bill. Those payouts are extremely expensive, and they keep the overall cost high even when the number of thefts drops.

What can I actually do to lower my car insurance costs in Ontario?

Shop around every renewal, even if it feels like a hassle. Use a licensed broker, not just online tools. Raise your deductible if you can absorb the risk. Ask about telematics or usage-based pricing if you’re a low-mileage or cautious driver. Bundle your home and auto policies. Claim every eligible discount, including winter tires. And after July 2026, review your coverage options carefully, but don’t waive anything without understanding your full insurance picture.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.