Mortgage Renewal Canada 2026: What the $835 Jump Means for You

Quick Answer: Why Mortgage Renewal In Canada is still high?

Why is my mortgage payment jumping so much even though rates came down? Because rates dropped from the ceiling, not back to the basement. If you locked in near 2% during the pandemic, even today’s lower rates around 4% to 4.5% nearly double your original deal. That gap can mean $400 to $835 more per month on a typical mortgage, and no further cuts are expected this year.

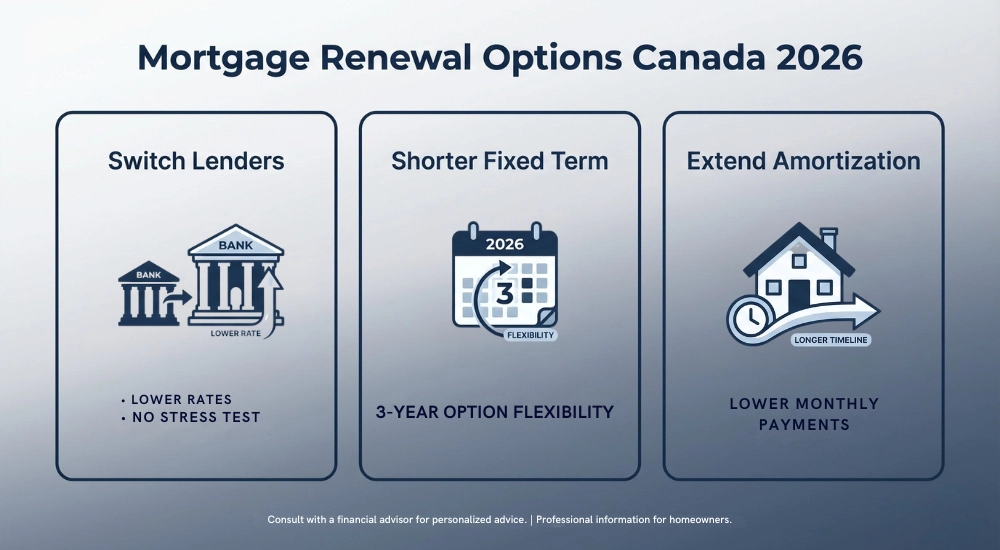

Can I switch lenders to get a better rate without re-qualifying? Yes. Current OSFI rules let you move your mortgage to a new lender without passing the stress test, as long as you don’t increase your balance or extend your amortization. This means you’re no longer trapped with your current lender’s offer. Shopping around, ideally through a broker, can save hundreds a month.

Is extending my amortization worth it? It costs more in total interest over the life of the loan, but it can meaningfully reduce the monthly hit. Stretching from 20 years back to 25 could shrink an $835 increase down to something far more manageable. Many families are treating it as a short-term pressure valve, with plans to increase payments or make lump sums once things stabilize.

🎧 Pressed for time? Listen to a summary of the heart of this story. Full data and guidance are detailed in the article below.

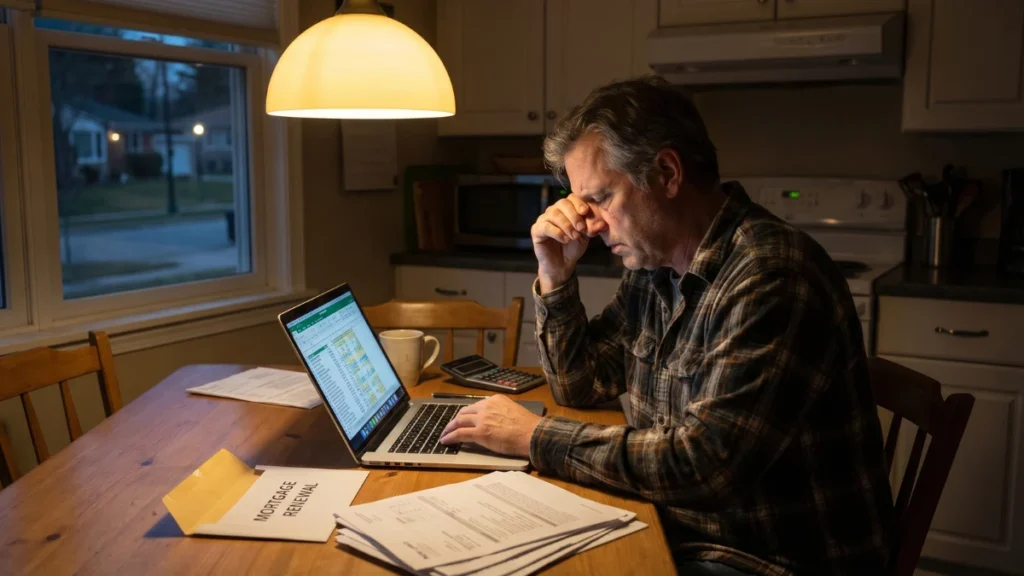

Mark Anderson sits at the kitchen table in his Auburn Bay home, laptop open, the house finally quiet. His kids, nine and twelve, are asleep down the hall. Sarah’s shift at the dental office ended hours ago, and she’s reading in the other room with the door cracked.

On the screen is the spreadsheet he’s kept since the day they bought this place in the summer of 2021. He calls it his “Rainy Day” file. Tonight, it feels more like a flood warning.

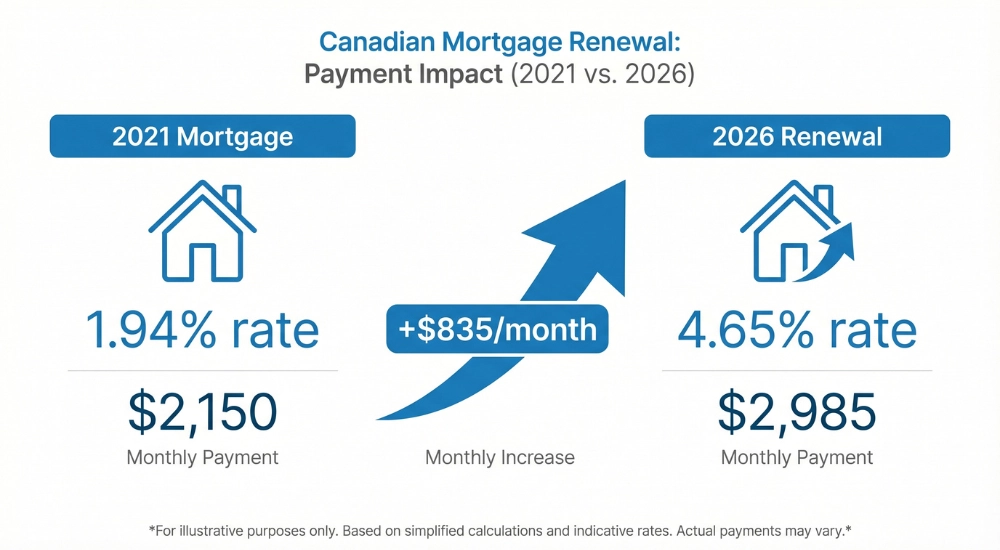

The renewal notice arrived last week. His five-year fixed rate of 1.94% is done. The best offer sitting on the counter is 4.65%. He’s run the numbers three times now.

The monthly payment jumps from $2,150 to $2,985. That’s an extra $835 a month, pulled from a household budget already stretched across groceries, hockey registration, car insurance, and utility bills that never seem to stop climbing.

Mark doesn’t panic. He’s a lead HVAC technician. He troubleshoots systems for a living. But Mortgage Renewal Canada 2026 is the kind of problem that doesn’t respond to duct tape or a good diagnostic. And he’s far from alone.

Mortgage Payment Shock Hits Home

Here’s what confuses Mark the most. Rates are supposed to be lower than they were two years ago. The Bank of Canada cut aggressively through 2024 and into early 2025. Headlines called it relief.

Politicians said families would feel the difference. And for people buying today, maybe that’s partly true.

But for households like the Andersons, locked into pandemic-era contracts now reaching maturity, the math runs in a completely different direction. That 1.94% wasn’t the norm. It was a product of emergency-level rate cuts during COVID, the kind of number that only existed because the world was falling apart. The bill for returning to something normal just landed on the kitchen table.

Across Canada, roughly 1.15 million households face this exact situation in 2026. They signed five-year terms at rates below 2%, and now they’re renewing into an environment where even the lowest available rates nearly double what they had. If rates came down, why does the payment go up? The question keeps people awake.

The answer is simple and painful. The Bank of Canada held its overnight rate at 2.25% on March 18, marking the fourth consecutive hold. That’s well below the peaks of 2023 and 2024.

But it’s still more than a full point above the emergency floor that gave people like Mark their original deal. Rates dropped from the ceiling. They just didn’t drop back to the basement.

And there’s a reason they can’t. Conflict in the Middle East, particularly the blockade of the Strait of Hormuz, has disrupted about 35% of the world’s seaborne energy shipments and pushed oil toward $97 a barrel. That kind of pressure threatens to reignite inflation just as it was cooling off. The Bank of Canada has said as much, calling it the biggest risk on their radar right now.

So the overnight rate stays put. The markets are pricing in an 84% chance of another hold at the April 29 announcement, and most of the Big Six banks expect 2.25% to last through the year.

For someone sitting in Auburn Bay with a renewal letter and a calculator, that means no rescue is coming from another round of rate cuts.

The Renewal Cliff Nobody Saw Coming

What’s unfolding this spring is sometimes called the Mortgage Renewal Cliff Canada has been bracing for. The phrase sounds dramatic. For families absorbing a 20-plus percent jump in their single largest monthly expense, it fits.

The mechanics are clear. A homeowner who took out a $440,000 mortgage in 2021 at 1.94% on a 25-year amortization schedule was paying roughly $1,851 a month. After five years, the remaining balance sits near $367,420 with 20 years left. Renewing that balance at today’s average five-year fixed rate of 4.19% from a major bank pushes the payment to about $2,253, a jump of more than $400 monthly, close to $4,800 a year.

For uninsured borrowers renewing at higher posted rates, the increase is steeper. And for families in cities like Calgary, where housing surged in 2021, the starting mortgage amounts were often larger. While Calgary is feeling the pressure now, many families are looking at how this compares to the high-stakes lessons from the Toronto trap. Bigger balance, higher rate, same paycheque.

What makes 2026 so frustrating is the wider picture. Cost-of-living data from Statistics Canada tells a story of an economy that actually shrank in the last quarter of 2025. Unemployment sat at 6.7% by February. People are losing jobs, spending less, tightening up.

In a normal cycle, that would mean lower rates. But the energy shock from abroad keeps the Bank of Canada interest rate stuck where it is.

For the Andersons, the timing feels almost personal. Mark’s careful budgeting kept the family stable through five turbulent years. Now the reward for making every payment on time is a renewal letter asking for $835 more a month.

Like Mark, your first step in managing the twenty-twenty-six transition is knowing the exact size of the gap you need to bridge. Use this tool to calculate your estimated payment shock and see how a tactical amortization adjustment might change the math for your household.

Payment Shock Calculator

Payment Shock Calculator

Current Payment:

New Payment:

Monthly “Shock”:

Tactical Move: A 25-year extension would drop this to .

Best Mortgage Rates Canada 2026

The single most useful thing Mark can do right now is refuse to passively accept his lender’s first offer. That sounds obvious. In practice, an enormous number of Canadians do exactly that. They sign the renewal letter, maybe negotiate a quarter point, and move on.

In 2026, this is a costly mistake, and there’s a specific regulatory reason why.

OSFI’s updated residential mortgage guidelines exempt certain mortgage switches from the stress test requirement for borrowers who switch lenders without increasing their balance or amortization period. Before this rule change, moving your mortgage to a new institution meant re-qualifying at the contract rate plus 2%, a bar near 6% that most responsible borrowers couldn’t clear on paper, even if they’d never missed a payment in their lives.

You were essentially trapped with your current lender. That trap is gone.

If Mark finds a better deal at another bank, he can switch without proving he could survive a rate that nobody expects to arrive. The lowest five-year fixed rates available for uninsured borrowers hover near 3.69%, compared to the 4.52% average posted by the Big Six. That gap can mean hundreds of dollars a month.

Some banks are sweetening the deal for people willing to move. BMO has been running cash-back promotions up to $4,100 for borrowers who switch over. That’s not loyalty. That’s competition.

And it only works in your favour if you’re willing to pick up the phone, call a broker, and compare not just rates but prepayment privileges, penalty structures, and lender negotiation flexibility.

Mark’s already pulled quotes from three lenders. He doesn’t love the process. But the spreadsheet doesn’t lie. Shopping aggressively could shave his payment increase by hundreds. That’s a season of hockey fees for his twelve-year-old.

Fixed vs Variable Mortgage 2026

The question Mark keeps turning over is whether to lock in again or ride a variable rate. The spread between the two has narrowed. The lowest five-year variable rate for insured mortgages sits around 3.35%, while the best available fixed rates are roughly in the high -3% to low -4%. For uninsured borrowers, the gap tightens further.

A variable rate tied to prime, currently 4.45%, offers lower initial payments. But it carries a real risk this year. If oil stays above $95 and the Strait of Hormuz situation worsens, inflation could push the Bank of Canada toward tightening later in 2026. That’s unlikely, but it’s not impossible, and any surprise hike hits variable-rate borrowers immediately.

What a lot of renewing homeowners are doing instead is going shorter. A three-year fixed rate near 3.89% is gaining traction as a middle path. It locks in certainty for the near term while leaving the door open to renew again in 2029, when global conditions may look very different. For families who can handle a slightly higher payment than the five-year fixed but want protection from variable swings, the three-year term has become a serious option worth modelling.

Buying Time: Extend Mortgage Amortization Canada

Mark doesn’t love this one. Stretching his amortization back from 20 years to 25 feels like driving in reverse. He’ll pay more interest over the life of the loan. The total cost of the house goes up.

But as a monthly cash-flow tool, it works.

Under the Canadian Mortgage Charter, lenders are now required to offer permanent amortization relief to at-risk borrowers and to waive fees for these adjustments during renewal. They’re also required to contact homeowners four to six months before renewal, which is how Mark’s letter arrived when it did.

The math is persuasive. Re-amortizing a balance of $367,420 at 4.19% over 25 years instead of 20 brings the monthly payment down to about $1,971. The jump from the old 2021 payment shrinks from a gut-punch to something closer to a hard nudge. For Mark, that could mean the difference between pausing RESP contributions and keeping them going. Between Sarah picking up extra shifts and Sarah having a Saturday with the kids.

The mortgage costs more in total, yes. But the family holds together. And if things improve in three to five years, he can always bump up payments or make a lump-sum contribution to claw back lost ground.

He’s still deciding. But the option is on the spreadsheet.

Why the Squeeze Won’t Let Up

Part of what makes this renewal cycle so heavy is that it doesn’t arrive alone. In Alberta, household budgets face pressure from several directions at once.

The Government of Alberta’s 2026 budget raised the provincial education property tax by 7.2%, adding roughly $340 a year to the bill for a median Calgary home.

Auto insurance premiums, tracked by the Automobile Insurance Rate Board, now average $1,835 annually, making Alberta the second most expensive province in the country for car coverage. A promised shift to a no-fault model won’t arrive until January 2027. For families renewing this spring, those savings are still just a promise.

Electricity rates in Calgary sit around 12 cents per kilowatt-hour before transmission, distribution, and green surcharges are stacked on. For a typical household, the total utility bill clears $300 a month during shoulder seasons and climbs higher in winter. Mark knows this number by heart.

The federal government has made some moves. The lowest federal income tax bracket dropped from 15% to 14% last year, saving a two-income household up to $840 annually. The national school food program, now permanent, saves families with two children roughly $800 a year on groceries. A temporary suspension of the 10-cent-per-litre fuel excise tax through Labour Day targets the energy shock from abroad.

These are real savings. They just don’t close an $835-a-month gap. When Mark adds them up against the new insurance premium, the property tax bump, and the utility bills, the relief feels like a coupon on a car payment.

The Quiet Weight of Running in Place

What the numbers don’t show is the feeling. Mark changes his own furnace filters. He patches drywall himself. He tracks every dollar on a spreadsheet that’s four years old and colour-coded by category.

He did what you’re supposed to do. Saved the down payment. Bought within his means. Locked in a rate. Kept every payment current for five years straight.

And now, through no decision of his own, the cost of his home jumped by more than ten thousand dollars a year.

That kind of shift leaves a mark. It’s the sense of being penalized for doing things right. It’s glancing at the RESP contributions and wondering whether they’ll have to pause. It’s Sarah picking up an extra half-day not because she wants to, but because the spreadsheet says she has to. It’s the kids not knowing why this summer’s camping trip got shorter.

Families across Canada in this exact position are describing the same thing in their own words. Some call their old rate a “ghost rate,” a number from a world that doesn’t exist anymore. Others talk about new mortgage payments “stealing from the future,” pulling money from savings, vacations, and their children’s plans to cover a house they already bought.

When a mortgage renewal squeezes monthly cash flow, many households start rethinking retirement saving too, especially if they are unsure whether an RRSP still makes sense when money is tight.

The frustration is quiet, mostly. It sits in the chest at eleven o’clock at night when the laptop’s still open. If you recognize it, you’re not failing. The ground shifted. You’re just trying to find stable footing.

Where Rates Go from Here

Nobody knows for sure where rates land by the spring of 2027. But the direction of travel tells us something.

The Bank of Canada is unlikely to cut further while oil remains elevated and the Strait of Hormuz conflict stays unresolved. If global energy markets stabilize and domestic demand continues to soften, modest cuts are possible in late 2026 or early 2027, likely 25 basis points at a time. The Big Six banks project the policy rate holding at 2.25% through at least the end of this calendar year.

For mortgage holders renewing right now, the honest truth is this: what you see today is close to what you’ll get. Waiting for a dramatic drop is not a plan. Acting on the tools that already exist is.

The stress-test exemption for lender switching, amortization extensions under the Mortgage Charter, shorter fixed terms: they all sit within reach. The families that come through Mortgage Renewal Canada 2026 steadiest will be the ones that treated the renewal letter like a negotiation, not a sentence.

Steady as You Go

Mark will figure this out. He’s not the kind of person who won’t. He’ll compare lenders. He’ll probably stretch the amortization. He’ll negotiate hard, shop wide, and make the spreadsheet work one more time. The April decision also matters because the Bank of Canada rate hold may change how mortgage holders think about renewal timing.

But he shouldn’t have to feel like he failed to get here. The rates changed. The rules changed. The world changed. Mark didn’t.

If your renewal letter is sitting on the counter right now, or arriving soon, open it with clear eyes. Run the numbers. Use the tools available. Talk to a broker, not just your bank.

And know that the pressure you’re feeling is shared by more than a million other Canadian families this year. You’re not alone in this, and you’re not behind. The ground moved. You’re still standing.

P.S. For households trying to decide whether extra money should go toward savings, flexibility, or tax planning, our RRSP vs TFSA Canada guide can help.

Frequently Asked Questions

How much will my mortgage payment increase when I renew in 2026?

It depends on your original rate, remaining balance, and the rate you renew at. A homeowner who locked in near 2% in 2021 and renews at today’s average around 4.2% could see their monthly payment climb by $300 to $800 or more. The exact figure hinges on your loan size and remaining amortization. Running the numbers with a broker before signing anything is the most practical first step.

Can I switch lenders without doing the stress test?

Yes. Under current OSFI rules, if you move your mortgage to a new lender without increasing your principal or extending your amortization, you don’t need to re-qualify at the stress-test rate. This “straight switch” rule lets homeowners shop for better rates without being locked to their current institution by qualification barriers.

Is extending my amortization a bad idea?

It increases the total interest you pay over the life of the mortgage, so the long-run cost goes up. But as a monthly cash-flow tool, it can be the difference between a household that stays stable and one that starts falling behind. Many financial professionals view it as a reasonable short-term tactic, especially if you plan to increase payments or make lump sums once your finances improve.

Should I go fixed or variable in 2026?

There’s no universal answer. Variable rates are slightly lower right now but carry more risk given the unpredictable global energy situation. Fixed rates offer certainty. Many renewing homeowners are choosing shorter fixed terms, like three years, to lock in stability while keeping the option to renew at potentially lower rates in 2029. Your best choice depends on your tolerance for uncertainty and how tight your monthly budget is.

Will the Bank of Canada cut rates again this year?

Most major banks expect the policy rate to stay at 2.25% through the rest of 2026. The Bank is holding steady because global energy disruptions, particularly around the Strait of Hormuz, pose ongoing inflation risk. If those pressures ease, modest cuts could arrive in late 2026 or early 2027, but no forecaster is projecting a return to pandemic-era lows.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.