Car Insurance in Ontario: What Actually Lowers Your Premium (2026)

Anita opened the envelope on a Tuesday evening. She was standing at the kitchen counter in her Brampton townhouse, still wearing her coat, groceries half-unpacked behind her. The renewal notice from her insurer showed a number she had to read twice: $2,240 for the year. Up from $1,980. No accidents. No tickets. Not even a parking violation. She put the letter down on the counter and stood there for a moment, doing quiet math in her head, wondering where exactly that extra $260 was supposed to come from.

If that scene sounds familiar, and you’re trying to figure out how to lower car insurance premium in Ontario in 2026, you’re not imagining things. And you’re not alone.

Ontario car insurance premiums have been climbing steadily, and if you’re trying to understand why car insurance feels so expensive in Ontario right now, the answer goes deeper than just inflation. And for a lot of households, the renewal letter has become one of those small dreads that arrives once a year and lingers for days. But here’s the thing most people don’t hear clearly enough: you can actually learn how to lower your car insurance premium in Ontario. Not through some loophole or magic trick, but through a handful of specific, deliberate actions that most drivers either don’t know about or haven’t gotten around to trying.

You can bring that number down, but only if you actively work the system instead of waiting on it.

Why Ontario Premiums Are So High in the First Place

Before getting into what works, it helps to understand the landscape quickly. Ontario is one of the most expensive provinces in Canada for car insurance. In the GTA, premiums regularly exceed $2,000 a year, and even outside the city, the provincial average sits roughly between $1,500 and $1,800 annually.

The reasons aren’t mysterious: vehicle repair costs have gone up sharply thanks to all the sensors and cameras built into modern cars. Auto theft has surged, especially across the GTA. Insurance fraud remains a persistent problem. And general inflation has pushed up the cost of parts, labour, and claims payouts across the board.

None of that is Anita’s fault. But all of it lands in her renewal letter.

The real question isn’t why insurance is expensive anymore. It’s what actually lowers your premium.

But before you can lower the bill properly, it helps to understand what your Ontario policy actually covers, from liability limits to OPCF endorsement codes.

Are Car Insurance Rates Going Down in Ontario in 2026?

It’s a fair question, and a lot of people are quietly hoping the answer is yes. After a few years of consecutive increases, the idea that premiums might finally level off feels overdue. The short answer, though, is not meaningfully, not yet.

The Financial Services Regulatory Authority of Ontario, known as FSRA, projects future collision loss trends growing somewhere between 6.6 and 10.6 percent annually over the coming years. Those aren’t numbers that suggest relief is just around the corner. And because the provincial regulatory system works on a twelve to twenty-four month delay, meaning the data used to set your 2026 premium was collected from claims paid out in 2023 and 2024, the pressure built up during those expensive years is still working its way through the system.

What this means practically is that waiting for the market to fix itself isn’t a strategy. The drivers who are paying less right now aren’t doing it because rates dropped. They’re doing it because they made specific decisions that separated their premium from the provincial average. That’s what the rest of this article is about.

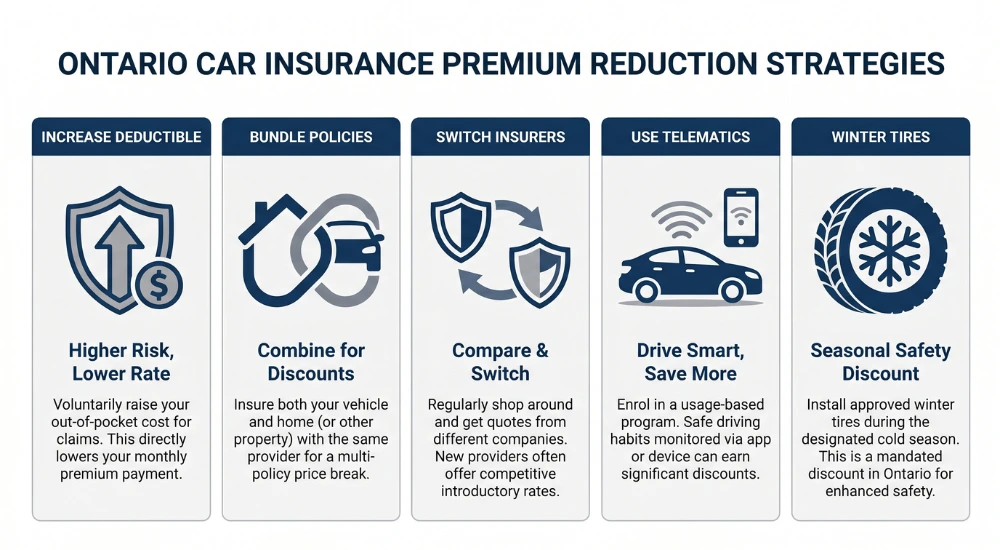

Raising Your Deductible Can Make a Real Difference

This is one of the simplest levers most people overlook. Your deductible is the amount you’d pay out of pocket before your insurance kicks in during a claim. A lot of Ontario drivers are still sitting on a $500 deductible because that’s what they signed up with years ago and never thought to change.

Moving from $500 to $1,000 can reduce your premium noticeably. The trade-off is real: if you do have an accident, you’re covering more upfront. But if you’re a careful driver and you’ve gone years without a claim, you’re essentially paying higher premiums to protect yourself from a scenario that hasn’t happened. For many households, accepting that slightly higher out-of-pocket risk makes the monthly math work better.

Bundling Your Policies the Right Way

If you have home insurance, tenant insurance, or even condo insurance, bundling it with your auto policy under the same provider almost always triggers a discount. Most major insurers in Ontario offer this, and the savings can be meaningful.

What people sometimes miss is that this works both ways. If your home and auto are already with separate companies, it’s worth getting a bundled quote from each of them to see which combination actually costs less. Bundling isn’t about loyalty. It’s about leverage.

Telematics Programs Reward the Way You Actually Drive

Usage-based insurance, sometimes called telematics, is one of those things that sounds a bit intrusive but can genuinely save money. You install an app or a small device in your car, and your insurer tracks basic driving behaviour: how hard you brake, how fast you accelerate, what time of day you drive.

If you’re a calm, consistent driver, this can work in your favour. Several Ontario insurers now offer telematics programs, and the discounts for safe driving can be substantial. It’s not for everyone, and some people aren’t comfortable with the tracking. But if you’re looking for every possible way to reduce your car insurance in Ontario, it’s worth at least exploring.

Switching Insurers Is the Move Most People Avoid

Here’s something that’s become almost common knowledge among drivers who’ve figured out how to get lower car insurance in Ontario: shopping around at renewal time is one of the single most effective things you can do.

Insurance companies don’t always reward loyalty. In fact, many drivers who’ve stayed with the same insurer for years are quietly paying more than a new customer would for the same coverage. The quotes can vary dramatically between companies for the exact same driver, the exact same car, and the exact same postal code.

Getting three or four quotes takes an afternoon. It’s not exciting work. But it’s the kind of afternoon that can save you hundreds of dollars a year.

Winter Tires and Group Discounts Most People Forget

Ontario insurers are required to offer a discount if you have certified winter tires installed during the winter season. It’s not a huge amount on its own, but it adds up, especially if you’re already buying winter tires for safety reasons.

Group discounts are the other one that flies under the radar. Many employers, alumni associations, and professional organizations have arrangements with insurance providers that give members access to lower rates. It’s worth checking with your HR department, your university alumni office, or any professional body you belong to. These discounts don’t always show up unless you ask.

Adjusting Coverage on Older Vehicles

If you’re driving a car that’s ten or twelve years old and fully paid off, it might not make sense to carry full collision and comprehensive coverage. The premium you’re paying to insure against damage might be close to what the car is actually worth.

Dropping optional coverage on an older vehicle is a straightforward way to bring your premium down. It’s not the right call for everyone, and it depends on your car’s value and your financial cushion, but for a lot of Ontario households hanging onto a reliable older car, it’s a conversation worth having with your broker.

When Does Car Insurance Actually Go Down in Ontario?

Most people assume their premium will automatically decrease as they get older and more experienced. Sometimes it does. But it rarely happens on its own without you understanding what actually triggers a reduction, and nudging the process along.

There are a handful of specific milestones that typically move your rate in the right direction. The most significant one is age. Drivers under twenty-five are statistically involved in more collisions, and insurers price accordingly. Once you cross into your mid-twenties, particularly around age twenty-five, many Ontario drivers see a noticeable drop at renewal, sometimes ten to fifteen percent, assuming a clean record. The drop doesn’t always happen automatically; it sometimes requires shopping around or prompting your broker to refile your risk profile.

Claim-free years are the other major lever. Each year you go without filing a claim builds what’s called a loss-free record, and most Ontario insurers apply a discount for every consecutive claim-free year, up to a point. The jump from zero years to three years of clean history can move your premium more than almost any other single factor outside of switching insurers entirely.

Upgrading your license class matters too. If you’re still on a G2, graduating to a full G license removes a restriction that insurers treat as elevated risk. For some drivers, that transition alone can reduce premiums by eight to twelve percent.

The table below is a rough guide, actual savings vary by insurer, driving history, vehicle, and postal code, but it gives you a useful frame for which milestones are worth tracking:

| Milestone or Event | Typical Premium Impact | Notes |

|---|---|---|

| Turning 25 (clean record) | −10% to −15% | Shop around at renewal; not all insurers apply this automatically |

| Each claim-free year (1–3 yrs) | −3% to −5% per year | Compounding effect; biggest savings after year 3 |

| G2 → Full G license upgrade | −8% to −12% | Tell your broker immediately after upgrading |

| Moving to a lower-risk postal code | −5% to −20% | GTA to smaller city moves can be dramatic |

| Vehicle turns 10+ years old | −5% to −10% | Consider dropping collision/comprehensive |

| Adding winter tires | −5% to −10% | Mandatory discount under Ontario law |

| Going 6+ years claim-free | Rate plateaus | Maximum discount tier reached with most insurers |

The point isn’t to wait passively for these milestones to arrive. It’s to know when they’re coming so you can shop for quotes at the right moment, armed with a record that now works in your favour.

If You’re a New Driver in Ontario, the Numbers Start Much Higher

Anita’s $2,240 renewal felt like a shock. For a new driver in Ontario, that number would look like a relief.

Young and newly licensed drivers in the province regularly pay anywhere from $3,500 to $6,000 a year, sometimes more, depending on where they live and what they drive. Insurers aren’t being punitive for the sake of it. The actuarial data is clear: drivers in their first three years behind the wheel have significantly higher claim rates. The premium reflects that reality, even when the individual driver in question has never had so much as a close call.

The good news is that there are a few specific moves that can bring that number down faster than simply waiting it out.

Staying on a parent’s policy for as long as possible is the most immediate option. If you’re a young driver living at home and using a shared vehicle, being listed as an occasional driver on an existing policy is almost always cheaper than taking out your own. The distinction matters: you need to be accurately classified as occasional, not as the primary driver of a vehicle you use daily. Misrepresenting this is considered misrepresentation on an insurance application and can void your coverage.

Choosing the right vehicle makes a bigger difference than most new drivers realize. A ten-year-old Honda Civic and a used Dodge Charger can come with dramatically different insurance costs, even for the same driver with the same history. Before buying a car, it’s worth calling your insurer or broker and asking for a quote on that specific make, model, and year. That conversation takes ten minutes and can save hundreds of dollars a year.

Taking a certified driving course is another concrete discount trigger. Many Ontario insurers offer a reduction for completing a Ministry-approved driver education program, and some extend a version of this discount for a few years after graduation. If you haven’t already taken one, the cost of the course often pays for itself in one renewal cycle.

The rates will come down. Every clean year helps. But these three decisions, staying on a parent’s policy when possible, choosing a lower-risk vehicle, and completing a certified driving course, can meaningfully compress how long the expensive phase lasts.

What Doesn’t Actually Work

There are a few persistent myths worth clearing up.

Loyalty doesn’t protect you. Staying with the same insurer for a decade doesn’t guarantee you a better rate. It often means the opposite.

Minimum coverage isn’t always cheaper in the way people think. Ontario’s mandatory minimums are set by regulation through the Financial Services Regulatory Authority of Ontario (FSRA), and going bare-bones on coverage can leave you dangerously exposed. The savings are often small compared to the risk you’re taking on.

And timing your renewal differently doesn’t reset your rate. Some people believe that switching mid-term or waiting for a certain month will get them a better deal. There’s no evidence that this works in any consistent way. What works is comparing actual quotes.

One More Thing Before Your Next Renewal: The July 2026 Benefit Changes

There’s a change coming to Ontario auto insurance on July 1, 2026 that most drivers haven’t heard about yet, and the renewal letter certainly won’t explain it clearly.

The province is restructuring how statutory accident benefits work. Under the current system, a standard package of benefits, medical care, income replacement, caregiver coverage, death and funeral benefits, comes bundled into every Ontario auto policy automatically. Under the new rules, only medical care, rehabilitation, and attendant care remain mandatory. A significant number of supplementary benefits will become optional, meaning drivers will need to actively choose and pay for coverage they previously had by default.

On paper, this sounds like it could lower premiums, since you’re carrying less coverage. And for some drivers, particularly those with strong workplace benefits plans or disability insurance through their employer, waiving certain optional coverages may be a reasonable financial decision. But for households without that safety net, quietly opting out of income replacement or caregiver benefits to save a few dollars a month is a trade-off worth understanding clearly before signing anything.

The practical thing to do before July 1 is to sit down with your broker and ask one direct question: under the new benefit structure, what am I keeping, what am I losing, and what does it cost to maintain what I have now? That conversation might take twenty minutes. It could be one of the more important financial decisions you make this year.

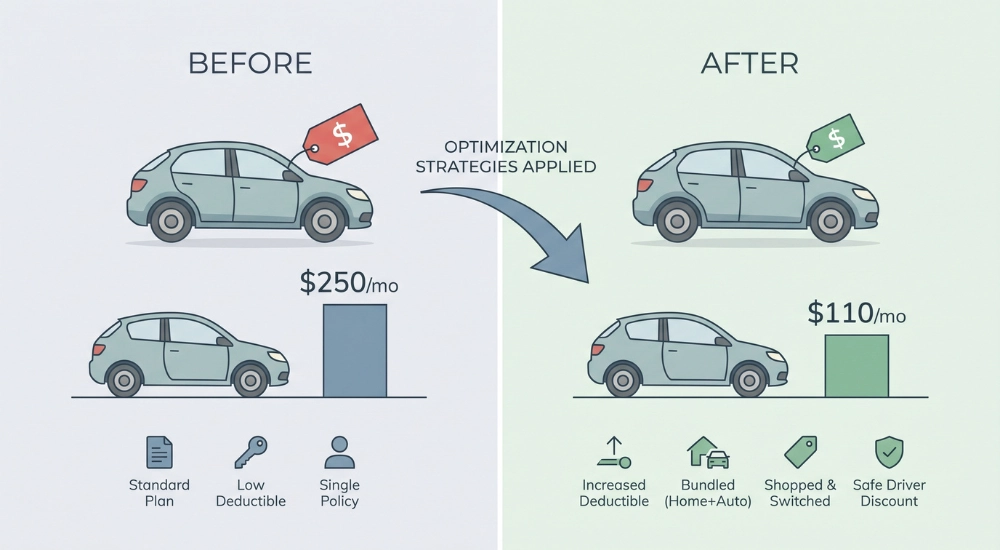

What Anita Did, and What It Saved Her

Let’s go back to Anita. After staring at that $2,240 renewal notice for a few days, she spent a Saturday morning getting quotes online. She reached out to three other insurers. She raised her deductible from $500 to $1,000. She confirmed her winter tire discount, which her previous insurer had never applied. And she bundled her auto policy with her tenant insurance.

Her new premium came in at roughly $1,700.

That’s about $540 saved in a year. Not from one dramatic change, but from stacking a few deliberate ones together. She didn’t switch to a lesser policy. She didn’t drop coverage she needed. She just stopped passively accepting whatever number showed up in the envelope.

A Quick Reference: What Each Strategy Typically Saves

Every situation is different. Your premium depends on your age, your driving record, your vehicle, and your postal code. But the table below gives a realistic range for what each tactic in this article can deliver in annual savings for a typical Ontario driver. Use it as a starting point when you’re deciding where to focus your energy first.

| Strategy | Typical Annual Saving | Best For |

|---|---|---|

| Switching insurers at renewal | $200 – $500 | Almost every driver, this is the highest-impact move |

| Raising deductible ($500 → $1,000) | $80 – $150 | Careful drivers with no recent claims |

| Bundling home and auto | $100 – $300 | Homeowners and renters with existing home/tenant insurance |

| Telematics / usage-based program | $100 – $300 | Calm, low-mileage drivers comfortable with app tracking |

| Winter tires discount | $50 – $100 | Any driver who already uses winter tires |

| Group or alumni discount | $50 – $150 | Worth checking, most people never ask |

| Dropping collision on older vehicle | $200 – $600 | Vehicles 10+ years old, fully paid off, lower market value |

| G2 → Full G license upgrade | $150 – $350 | New drivers still on restricted license |

| Each claim-free year | $50 – $150 | Compounds over time, biggest effect after year 3 |

None of these require a financial adviser or a complicated negotiation. They require knowing the levers exist, and then pulling them deliberately. Anita found a few hundred dollars by spending a Saturday morning on it. Most people who go looking find something. The ones who don’t find anything are usually the ones who never look.

The Mindset Shift Happening Across Ontario

There’s a growing frustration among Ontario drivers, and it’s changing behaviour. More and more people are treating their insurance renewal the way they treat a phone plan: something you renegotiate or walk away from every year or two. The old assumption that loyalty would be rewarded has given way to a quieter, more practical instinct. Shop every renewal. Compare every quote. Don’t assume your current insurer is giving you the best deal.

It’s not cynicism. It’s just pattern recognition. People have watched their premiums climb year after year despite clean records, and they’ve started doing the only thing that consistently makes a difference: they’ve started moving.

The Quiet Weight of It

None of this is fun. Nobody wants to spend their weekend comparing insurance quotes or calling brokers. And there’s a particular kind of exhaustion that comes from feeling like you’re doing everything right and still watching your costs go up. You haven’t caused an accident. You drive carefully. You follow every rule. And the number still climbs, just like how everyday expenses have quietly gone up.

That frustration is valid. The system isn’t designed to reward you for being a good driver as much as you’d think it should. But knowing how to lower your car insurance premium in Ontario, even by a few hundred dollars, gives you back some control in a situation that can feel like it has none.

Looking Ahead

Insurance premiums in Ontario aren’t likely to drop dramatically anytime soon. Repair costs continue to rise with vehicle complexity. Theft remains a serious issue, especially for certain makes and models. And the broader cost pressures that affect the insurance industry aren’t going away.

But the tools available to individual drivers are real. Telematics programs are expanding. Comparison tools are getting easier to use. And the cultural shift toward active shopping is putting more pressure on insurers to compete.

The outlook isn’t about hoping things get cheaper. It’s about getting better at navigating the system as it is.

A Few Deliberate Changes

Lowering your premium isn’t about one trick. It’s about understanding where your money is actually going and making a few deliberate changes. Raise your deductible if you can absorb the risk. Bundle where it makes sense. Ask about every discount you might qualify for. And shop your renewal like your money depends on it, because it does.

You’re not failing because your insurance costs too much. The landscape has shifted. But you can shift with it, and you don’t need anyone’s permission to start.

Frequently Asked Questions

Can you actually lower car insurance in Ontario, or is the price basically fixed?

You can lower it, but not by waiting. The most effective strategies are raising your deductible, bundling policies, using telematics, and shopping around at every renewal. None of these are guaranteed to cut your bill in half, but stacking a few of them together can save hundreds of dollars a year.

Is it worth switching car insurance companies in Ontario?

In most cases, yes. Many Ontario drivers report significant savings just by comparing quotes from three or four insurers at renewal time. Loyalty rarely translates into better pricing, and the same driver can be quoted very different rates by different companies for identical coverage.

What is telematics insurance, and does it really save money in Ontario?

Telematics, also called usage-based insurance, tracks your driving habits through an app or device. If you drive calmly and consistently, you can earn discounts based on your actual behaviour behind the wheel. It’s not for everyone, but safe drivers often see real savings.

Do winter tires actually lower your car insurance premium in Ontario?

Yes. Ontario insurers are required to offer a discount for certified winter tires. The amount varies by company, but it’s a discount you should always confirm is being applied to your policy during the winter months.

How much can you realistically save on car insurance in Ontario?

It depends on your situation, but a GTA driver paying over $2,000 a year could potentially save $300 to $600 annually by combining strategies like switching insurers, raising the deductible, bundling policies, and confirming all eligible discounts. The key is making several small, deliberate moves rather than looking for a single fix.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.