Bank of Canada Rate Hold: What Mortgage Holders Need

Quick Answer

The Bank of Canada’s rate hold at 2.25% keeps variable mortgage rates stable, but it doesn’t lower your fixed rate. Fixed rates are set by bond markets, not the Bank, and bond yields have risen in recent months due to Middle East tensions and trade uncertainty. If you’re renewing a pandemic-era mortgage this year, expect a meaningful payment increase regardless of the hold. The question isn’t whether rates will drop in time to save you. For most renewing homeowners in 2026, the question is how to manage the new number as smartly as possible.

🎧 Pressed for time? This summary covers what the Bank of Canada rate hold means for mortgage holders in 2026, and whether your renewal payment is about to change.

Glenn has been doing the math on the back of envelopes for six months. Not dramatic calculations, just the ordinary kind. He sits at his kitchen table in Regina after dinner, the kids in their rooms, a cup of coffee going cold beside him, and he pulls up a mortgage calculator on his phone. He types in the numbers. He stares at the number it spits back. He puts the phone face-down.

His five-year fixed mortgage is coming up for renewal this summer. He locked in at just under two percent in 2021, when that kind of rate felt almost too good to believe. Now the Bank of Canada has held its overnight rate again, and Glenn is trying to figure out whether that is good news or just more waiting.

Glenn isn’t panicking. He’s 47, careful with money, practical about his expectations. But he’s tired of being patient.

What the Headlines Miss for Renewing Homeowners

When people hear “rate hold,” they often hear “things are staying the same.” That’s understandable. The Bank of Canada interest rate staying at 2.25% sounds like neutral territory, like treading water. But for the more than one million Canadian households facing mortgage renewal in 2026, the hold is not neutrality. It’s confirmation.

It confirms that the deep rate cuts people were quietly hoping for, the ones that would soften the renewal blow, aren’t coming. Bay Street analysts and financial markets largely expect the Bank to remain on hold through 2026. Glenn had been watching the rate announcements like a man watching weather forecasts before a camping trip. He kept thinking the next one might change things. The March hold didn’t. The Bank of Canada’s April 29 announcement confirmed the same direction: rates are steady, but mortgage relief has not arrived.

The confusion isn’t hard to understand. The Bank cut rates aggressively in 2024 and into early 2025. Canadians watched the overnight rate fall from five percent to 2.25% over roughly eighteen months. That felt like progress, like real relief was close. Then it stopped. And what most people didn’t fully grasp is that variable and fixed mortgages respond to completely different forces.

The Bank of Canada’s overnight rate directly shapes variable mortgage rates. Fixed rates follow a different signal altogether: Government of Canada bond yields. Fixed rates may drift modestly higher as 5-year Government of Canada bond yields stay in the 3.0% to 3.5% range. So even when the Bank holds or cuts, fixed rates can move in the opposite direction. That’s exactly what’s been happening since late 2025.

Fixed vs Variable: Regina’s Real Numbers

For someone like Glenn, the fixed versus variable mortgage Canada question feels less like a philosophical debate and more like choosing between two uncomfortable realities.

Borrowers renewing their fixed mortgage rate in April 2026 can expect to pay an average of $622 more per month, a 24% increase. That figure is based on a mortgage balance of roughly $537,000 at today’s best renewal rate. Glenn’s balance is smaller than that, but the percentage math still stings.

The prime rate in Canada as of late April 2026 sits at 4.45%. Variable rates are currently running lower than fixed, somewhere in the 3.55% to 3.65% range depending on the lender and the borrower profile. Fixed rates currently sit approximately 85 to 95 basis points higher than variable rates. On a $400,000 renewal, that spread translates to a real difference in monthly cash flow, easily $150 to $200 per month.

The catch is risk. Some economists, particularly at Scotiabank, are predicting rate hikes in the second half of 2026, with the key policy rate potentially climbing to three percent by year-end. If that happens, a variable rate that looks comfortable today gets more expensive fast. Most other economists think a hold is more likely than a hike, but the divergence in forecasts is itself the story. Nobody really knows.

What Glenn is actually weighing isn’t just the rate. It’s his own capacity to absorb a surprise. He has two kids heading toward university. His wife works part-time. His household cash flow has some room, but not unlimited room. For people in his position, mortgage rate stability isn’t just a preference, it’s a budget tool.

For a deeper look at the payment shock itself, read our guide to Mortgage Renewal Canada 2026: Why Payments Jump $835.

What Canadians Are Actually Doing at Renewal

Across the country, renewing homeowners are making quiet, practical decisions. Over 28% of homeowners are switching to a better deal at renewal, up about 46% from a year ago. That’s a significant shift. Many of these people spent years renewing with the same bank out of habit or convenience. The new rate environment has finally made shopping around feel urgent enough to actually do.

Since November 2024, OSFI has removed the stress test for uninsured straight switches at renewal, meaning if you keep the same balance and amortization, you can switch to another federally regulated lender without re-qualifying. That change quietly opened a door that many homeowners didn’t know existed.

Brokers are also reporting a noticeable shift away from the standard five-year fixed. Many clients are now choosing a variable rate or a short-term fixed rate, such as a 2- or 3-year fixed rate, more often than the popular 5-year fixed. The logic is practical: if rates are genuinely expected to stay flat, or if there’s any realistic chance of cuts in 2027, a shorter term lets you re-enter the market sooner without being locked into today’s numbers for half a decade.

Glenn finds this genuinely useful to think about. He’d always assumed five years was just what you did. His parents did five years. His brother does five years. But the renewal conversation in 2026 looks different, and accepting the default term without at least pricing out a three-year fixed is leaving money on the table.

The other thing people are learning, sometimes too late, is the break penalty difference between fixed and variable. Variable mortgages charge three months’ interest if you break early; fixed mortgages use the Interest Rate Differential, which can cost five figures at a big bank. If there’s any chance your life changes in the next few years, that penalty calculation matters more than the rate itself.

Why This Isn’t About Bad Luck

The mortgage renewal stress Glenn is feeling isn’t personal failure, and it isn’t bad financial planning. It’s structural.

Many Canadian homeowners have already renewed into higher rates, while others still face payment pressure as their mortgage terms come due. Glenn’s situation is not unusual. It’s the expected outcome of what happened when rates hit record lows during the pandemic and then had to rise sharply to control inflation. Those pandemic-era rates were policy tools, not permanent features of the market. The people who took them out weren’t wrong to take them.

The Bank of Canada is holding rates now because it’s stuck between two competing pressures. The tension between inflation and economic growth is complicating the Bank’s decision-making. On the one hand, you might want to raise rates to tamp down on inflationary pressures, but you’d also potentially want to lower rates to stimulate demand. With the uncertainty reigning and the stagflation environment, holding is the prudent measure.

What that means for ordinary Canadians is that the central bank is managing its own risks, not yours. Its mandate is inflation control. Your mortgage renewal is not part of its calculation.

The labour market in Canada remains soft, with employment gains in the fourth quarter of 2025 largely reversed in the first two months of 2026, and the unemployment rate rising to 6.7% in February. A weaker economy normally creates pressure for rate cuts. But geopolitical disruption has pushed energy prices higher, and the sharp increase in global energy prices has led to increases in gasoline prices, which will push up total inflation in the coming months. The Bank can’t cut into rising inflation without risking its credibility. So it holds.

Glenn is living in the middle of that policy tension, paying for it in loonie terms every month.

The Weight of Waiting

There’s a particular kind of exhaustion that comes from watching and waiting on something you can’t control. Glenn has been doing it for over a year. He checked the Bank of Canada’s January announcement. He checked March. He’ll check April 29. Each time, he reads the same kind of careful language, inflation is broadly on track, uncertainty remains elevated, the Governing Council will be monitoring.

That is why a rate hold can still feel heavy inside the broader cost-of-living squeeze.

The mental load of this is real. It’s not dramatic, it doesn’t announce itself loudly, but it sits there. Every grocery run, every hydro bill, every time he fills up the car, Glenn is quietly aware that his mortgage payment is about to go up regardless of what the Bank does. The hold doesn’t prevent the shock. It just means the shock is baked in now. Even when one cost eases, like fuel, pump relief hasn’t solved broader household pressure.

What makes this harder is that the math is easy enough to do but uncomfortable enough that people avoid it. A $300 to $600 increase in monthly mortgage payments on a Canadian household budget is not a rounding error. By the end of 2026, approximately 33% of Canadian mortgage holders are expected to face higher monthly mortgage payments, and approximately 75% of borrowers facing a payment increase have 5-year fixed-rate mortgages.

Glenn is not in a minority. He’s in the quiet majority of Canadians who did everything reasonably right and are still facing a meaningful payment increase because the rate environment they bought into no longer exists. For many households, the hardest part is not one bill but how monthly bills quietly drain a household budget.

Key Facts

- The Bank of Canada’s overnight rate has been 2.25% since late 2025, with many forecasters expecting a hold through much of 2026.

- Fixed rate renewers in April 2026 face an average payment increase of $622 per month, a 24% jump, compared to their pandemic-era rates.

- The lowest available 5-year fixed rate in Canada sits around 4.04% to 4.09% for high-ratio mortgages as of early April 2026, while big bank rates run closer to 4.29%.

- Inflation rose to 2.4% in March 2026, pushed higher by energy prices tied to Middle East conflict, up from 1.8% in February.

- Over one million Canadian mortgages are up for renewal in 2026, many locked in at pandemic-era rates below 2.50%.

What Comes Next: The Honest Forecast

Most forecasters expect the overnight rate to stay at 2.25% through the end of 2026, with some possibility of a hike in late 2026 or early 2027. The C.D. Howe Institute’s monetary policy council suggests the Bank should hold the overnight rate until at least October and then raise it to 2.5% by this time next year. That’s a modest move, but it points in one direction.

Canada’s GDP is forecast to grow just 1.1% in 2026 and 1.5% in 2027, held back by trade uncertainty and slow population growth. Weak growth normally argues against rate hikes. But the inflation dynamic tied to energy prices complicates that argument, and nobody at the Bank wants to repeat the mistake of cutting too soon.

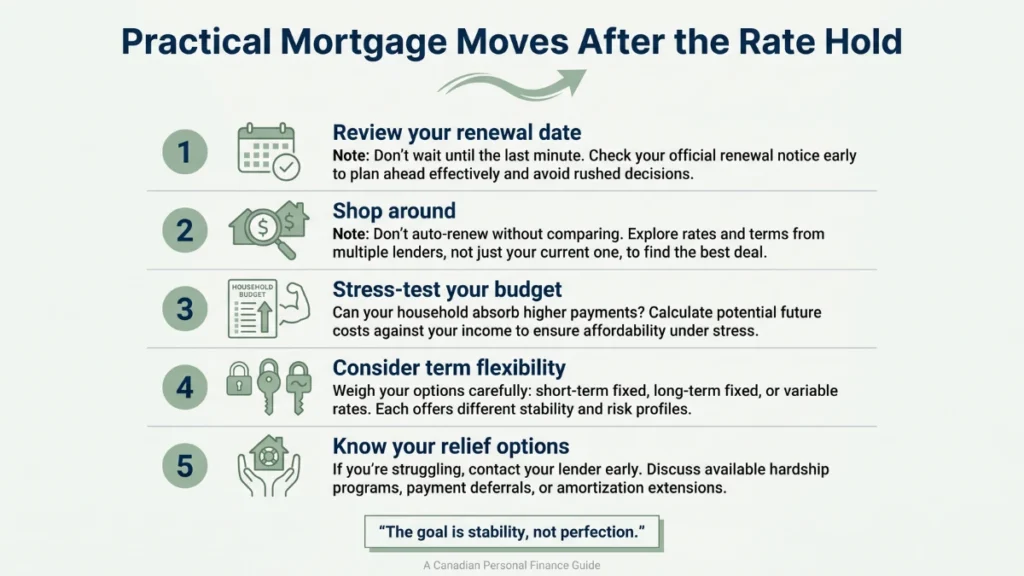

For Glenn, that means the window for meaningful rate relief before his renewal has likely closed. The practical task now is making the best decision available, not waiting for a better one that probably won’t arrive in time. Shopping multiple lenders, asking about a 3-year versus 5-year fixed, and discussing a 120-day rate hold with a lender or broker are the kinds of levers Glenn can actually examine.

Household Tactical Table: Mortgage Renewal Scenarios for 2026

| Scenario | Mortgage Balance | Old Rate (2021) | New Rate (2026) | Monthly Payment Old | Monthly Payment New | Monthly Increase |

|---|---|---|---|---|---|---|

| Mid-size renewal, 5-yr fixed | $400,000 | 1.99% | 4.04% | ~$1,693 | ~$2,118 | ~$425 |

| Larger renewal, 5-yr fixed | $537,000 | 2.00% | 4.04% | ~$2,275 | ~$2,870 | ~$622 |

| Mid-size renewal, 3-yr fixed | $400,000 | 1.99% | 3.74% | ~$1,693 | ~$2,052 | ~$359 |

| Mid-size renewal, variable | $400,000 | 1.99% | 3.60% | ~$1,693 | ~$1,992 | ~$299 |

| Mid-size renewal, switch lender | $400,000 | 1.99% | 3.89%* | ~$1,693 | ~$2,059 | ~$366 |

You’re Not Failing. The Equation Changed.

Glenn will make his renewal decision over the next few weeks. He’ll probably call a mortgage broker, something he’s never done before, after reading that his bank’s renewal offer rarely reflects their best available number. He might choose a three-year fixed and revisit the question in 2029 when the rate picture may look different. He might go variable if he decides he has enough cash cushion to absorb a modest hike.

What he won’t do, hopefully, is read the Bank of Canada rate decision as a message about his own financial competence. It isn’t. The Bank of Canada interest rate is a policy tool. It’s being held because inflation and growth are pulling in opposite directions and the Bank is buying time to see how things settle.

You bought a house. You took a mortgage rate that was available to you and reasonable at the time. The pandemic made those rates exceptionally low. The inflation that followed made them impossible to maintain. You’re now managing the transition between those two realities, and so is almost everyone else on your street.

The renewal wall is real. The payment increase is real. But Glenn has options, and so do you. Shop early, price every term length, understand the penalty math before you sign anything, and don’t let your bank’s auto-renewal letter be the last word on what you pay.

That is why responsible people can still feel squeezed, even when they have made careful decisions for years. The financial reality of 2026 is harder than it looked in 2021. Your judgment hasn’t changed. The equation has.

Frequently Asked Questions

What does the Bank of Canada rate hold mean for my mortgage renewal?

If you have a variable mortgage, the hold keeps your rate and payment stable for now. If you’re renewing a fixed mortgage, the hold doesn’t help much because fixed rates are driven by bond yields, not the Bank’s overnight rate. Bond yields have risen in recent months, which has kept fixed rates elevated even as the Bank stands still.

Should I lock in a 5-year fixed rate or choose a shorter term in 2026?

There’s no universal right answer, but many brokers are seeing more Canadians choose 2- or 3-year fixed terms in 2026. The logic is that locking in for five years means you’re committing to today’s higher rates for a long time. A shorter term costs slightly more per month in some cases, but it gives you a chance to renew again in a few years if rates have moved.

Is it worth switching lenders at renewal?

In many cases, yes. Since November 2024, OSFI removed the mortgage stress test for uninsured borrowers doing a straight switch at renewal, meaning you can shop around without re-qualifying as long as you keep the same balance and amortization. Brokers often find rates 20 to 50 basis points lower than what your current bank offers at renewal, which adds up to real money over a five-year term.

Will the Bank of Canada cut rates before my 2026 renewal?

After the April 29 hold, many economists still expect the Bank to stay cautious through much of 2026. That does not mean cuts are impossible, but it does mean homeowners should be careful about building a renewal plan around a quick cut.

What is a 120-day rate hold and should I use one?

A rate hold locks in a quoted mortgage rate with a lender for up to 120 days. If rates rise during that window, you’re protected. If rates fall, most lenders will match the lower rate at closing. Getting a rate hold as soon as your renewal window opens, often six months before your maturity date, is one of the few zero-cost steps you can take to manage the uncertainty of renewing in a volatile rate environment.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.