With Inflation Down, Why Is Everything So Expensive in Canada?

I’m not a financial advisor. This article shares personal stories and general information only. For advice specific to your situation, consult a qualified professional.

Late in the evening, Daniel sits at the dining table with his phone, checking the family account before the next round of payments clears. Nobody booked a trip. Nobody bought a new appliance. There was no reckless spending this month. Still, groceries ran high again, the insurance payment went up, and there never seems to be as much breathing room as there should be. So he ends up asking the same question many households are asking now: why is everything so expensive in Canada?

Then he sees another headline saying inflation has cooled. His reaction is immediate. If inflation Canada headlines are sounding calmer, why does ordinary life still feel so heavy?

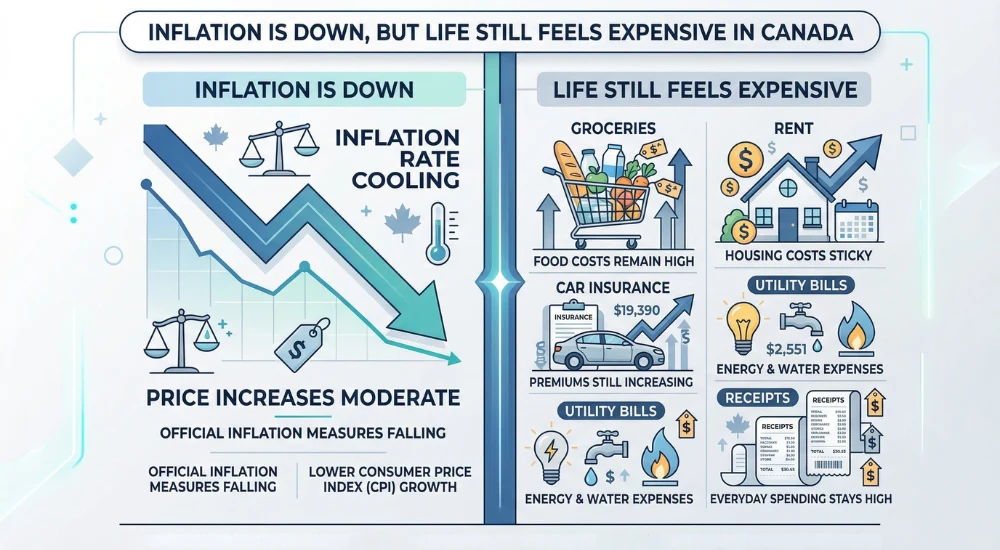

That confusion is not irrational. According to Statistics Canada CPI data, Canada’s all-items CPI rose 1.8% year over year, but several essentials were still climbing faster than that. Food purchased from stores was up 4.1%, rent 3.9%, restaurant food 7.8%, and passenger vehicle insurance premiums 8.2%. Grocery prices were also 30.1% higher than they were in February 2021. That is the gap between the headline and the household budget.

You are not imagining it

A lot of people hear that inflation is down and assume life should already feel easier. That sounds reasonable. But headline inflation and lived financial pressure are not the same thing.

People do not live inside one national number. They live inside grocery receipts, rent payments, insurance notices, pharmacy counters, school costs, and monthly deductions. The clearest correction from the research is simple: inflation is a rate of change, not a rewind button. What households are actually living with is a higher price level plus whatever is still rising faster than income and fixed obligations.

That is why the question is not only what the inflation rate is. The deeper question is why the cost of living in Canada still feels out of sync with the calmer tone of the headlines.

This is the misunderstanding at the heart of the problem.

What inflation in Canada actually tells you

As Bank of Canada’s inflation explainer makes clear, when inflation falls, it usually means prices are still rising, just more slowly than before. It does not mean prices went back down to where they were a few years ago. The research explicitly warns against treating lower inflation like relief already delivered. The safer, truer framing is that headline inflation slowed, but that mainly means prices rose more slowly than they did during 2021 to 2023, not that life became cheap again.

That difference matters because households are still carrying the effects of the earlier jump. Grocery prices did not quietly return to older levels. Rent did not reset to what many families used to think of as normal. Insurance did not suddenly become light again. So when people say inflation is down but life still feels expensive, they are not contradicting the data. They are reacting to what the data actually means in real life.

The real damage was already done when prices reset higher

Daniel stood in the meat aisle of his local grocery store, staring at a pack of chicken breasts that cost nearly double what it did just a few years ago. He adjusted his mask, checked his banking app, and sighed. Daniel is not reacting to one bad week. He is reacting to the accumulation of the last few years.

That is why so many people feel worn down even when this month’s inflation number looks more moderate. The pressure is less about one fresh spike and more about a higher baseline that settled into ordinary life. The research describes this as a price-level reset, especially in groceries, where the real pressure is less about today’s monthly change and more about the 30%+ step-up since 2021 becoming the new normal.

For many Canadian families, the math simply does not add up when they realize why protein prices in Canada 2026 still feel expensive despite the headlines claiming the “crisis” is over

This is also why broad reassurance can fall flat. You can tell people inflation is cooling, but if their household has already been reset at a much more expensive level, they will not feel that message as relief.

The costs that still shape daily life

Canadians do not experience inflation as a theory. They experience it through the categories they cannot avoid.

Why are groceries so expensive in Canada?

If families are asking why are groceries so expensive in Canada or why is food so expensive in Canada, the emotional answer is easy to understand. Food is not a bill people see once a year. It is something they confront every week, often several times a week.

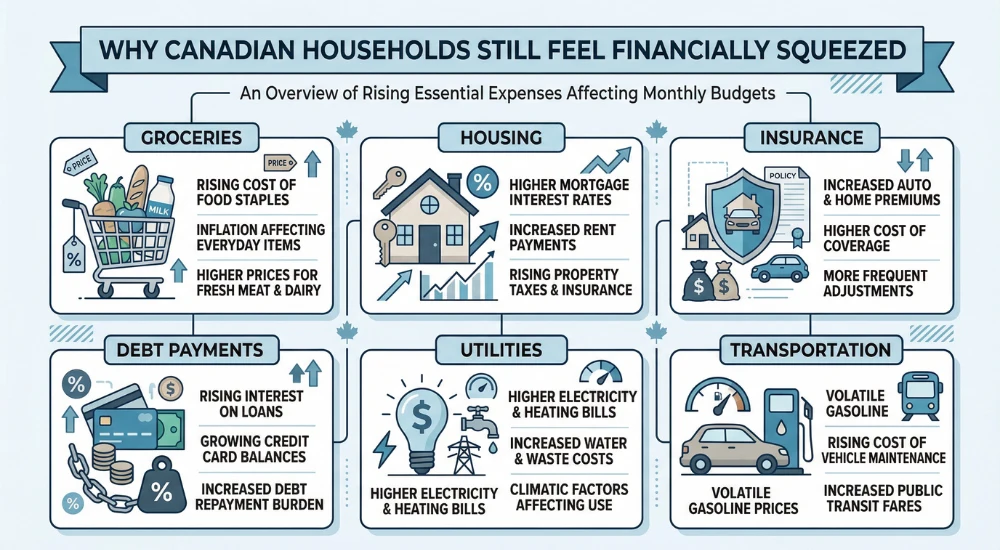

And the numbers support that feeling. Statistics Canada food price data shows that food purchased from stores rose 4.1% year over year in February 2026, while grocery prices had risen 30.1% since February 2021. Meat remained especially painful, with meat up 8.2% year over year and fresh or frozen beef up 13.9%.

That pressure becomes even clearer in higher-protein shopping, a pattern we see in protein prices across the country. That helps explain why food keeps punching above its weight in people’s emotional picture of the economy.

For Daniel, this is where the disconnect feels most obvious. He does not need an inflation chart to tell him life is expensive. He feels it in the grocery aisle, where even a normal weekly shop no longer feels normal.

Even when overall inflation cools, families still feel squeezed because they are making repeated trade-offs in a grocery aisle that no longer feels routine.

Why is housing so expensive in Canada?

The same thing happens when people ask why is housing so expensive in Canada. They are not only asking about home prices. They are asking about monthly pressure.

When Daniel thinks about why housing still feels so heavy, he is not thinking like an economist. He is thinking about how one large monthly cost quietly shapes every other decision the family makes.

Housing cashflow stress is still one of the clearest ways the household reality differs from the headline. Rent is still rising faster than all-items CPI, and the mortgage side is better described as a multi-year payment-shock wave than as one dramatic cliff. Recent mortgage renewal pressure research suggests that many Canadian households renewing in 2025 and 2026 are still likely to face higher monthly payments versus December 2024 payments.

That matters because housing is the bill that shapes the rest of the month. If too much income disappears into rent or housing costs, the rest of the budget starts feeling tight before groceries, fuel, childcare, debt payments, or school expenses even arrive.

Insurance and recurring bills quietly drain cash flow

One reason people keep wondering why is everything so expensive in Canada is that the pressure often comes from boring bills, not flashy spending.

When Daniel saw the insurance notice, the feeling was not panic so much as quiet frustration. It was another reminder that ordinary bills keep rising without making life feel any better in return.

Insurance is a good example. The safest framing from the research is not that “everything is exploding,” but that premiums are rising materially even in low-inflation months. Passenger vehicle insurance premiums were up 8.2% year over year, and homeowners’ home and mortgage insurance was up 6.5%. The better-supported drivers are repair costs, theft claims, and catastrophe losses, not just vague inflation.

Then there are the recurring bills that rarely feel dramatic in isolation: electricity, water, telecom, subscriptions, school fees, parking, app renewals, and the many small charges that chip away at flexibility. The research warns against pretending utilities are a simple “everything up” story, because some components rise while others fall. But it also makes clear that the household experience is often one of unpredictability and steady drain.

Debt payments reduce breathing room

Another reason many people still feel broke is that income may still cover life, but it no longer creates margin.

The deeper household story in the research is that Canadians are managing a high fixed-cost base, a still-expensive essentials basket, and increasing reliance on credit as a shock absorber. That does not mean every household is in crisis. It means many are using credit cards and other borrowing to smooth the monthly strain of ordinary life.

That is a very different emotional reality from the one suggested by a calm inflation headline.

Why a decent income no longer feels like enough

This is where the frustration becomes more personal.

Many households are still working. They are still paying their bills. They are still trying to act responsibly. But essentials now absorb too much of their income, and the earlier price shock has not been repaired.

The research says affordability depends on income growth, housing tenure, and fixed debts, not CPI alone. It also stresses that CPI weights do not match each household’s real basket. That matters. A renter with children, a commuter with rising insurance, or a homeowner facing renewal stress will feel the economy very differently from the national average.

So, when people say a good income no longer feels like enough, they are often describing something real. Not always collapse. Not always poverty. But erosion. That same pattern shows up in city life too, especially among hardworking single professionals in Toronto who still keep falling behind financially.

Daniel and his wife are not in open financial disaster. That is exactly what makes the squeeze so disorienting. The family is functioning, working, and paying its way, yet the stability that used to come with that effort feels thinner than it should. It is the same quiet strain we see in many responsible people who still feel financial pressure in their 50s in Canada.

Why so many Canadians still feel broke even when they are managing

Being broke is not always a technical condition. Sometimes it is a feeling of having no breathing room.

It means one surprise expense can throw off the month. It means groceries go on the card once, then again. It means there is no satisfying sense of recovery, only constant recalculation. It means the household may still be functioning, but it no longer feels secure.

This is the point in the article where the emotional and financial realities meet. The question why is everything so expensive in Canada is not just about prices. It is also about mental load. It is about the exhaustion of living in a version of ordinary life that feels permanently more expensive than it used to.

That is why so many Canadians still feel broke even when they are technically managing.

Why inflation in Canada and real life can feel like two different stories

None of this means the inflation data is fake. It means the data and the lived experience answer different questions.

Headline inflation tells you something important about the pace of price change. But it does not tell you whether households feel relief. Relief depends on whether wages caught up, whether rent or mortgage pressure eased, whether groceries stopped dominating weekly life, and whether insurance and fixed bills stopped quietly rising in the background.

That is why the most useful way to explain inflation Canada right now is not with a triumphant headline about things returning to normal. It is with a calmer truth: headline inflation cooled, but essentials still rose faster than the headline, and many households are still living on top of a much higher price base than they were a few years ago.

You are not failing. Life really did get more expensive

Daniel’s confusion was reasonable. The headline told him one thing, but his monthly life told him another.

Why is everything so expensive in Canada is not just a feeling

That is where many Canadian households are living now. Groceries are still far above where they were a few years ago. Housing still shapes the whole budget. Insurance and recurring bills still eat into the month before a family gets a chance to feel secure. The household reality is slower to heal than the headline.

So if you have been asking why is everything so expensive in Canada, the answer is not that you failed to understand your budget. It is that lower inflation is not the same as a cheaper life.

Canada may be past the worst inflation headlines, but many households are still living with the bill.

Why does inflation say it’s cooling, but my bills keep going up?

Inflation measures how fast prices are rising. When it cools, prices are still rising—just more slowly. What households feel is the cumulative effect of years of increases. The 30% jump in grocery prices since 2021 is permanent; the new baseline is simply higher.

Are grocery prices the only thing making life feel expensive?

No. Housing, insurance, and recurring bills have also reset to a higher level. Rent is still climbing faster than the overall CPI, and many homeowners face payment shocks when mortgages renew. These fixed costs quietly consume more of the monthly budget before a family even reaches the grocery aisle.

Why does a decent income no longer feel like enough?

Because essentials now absorb a larger share of that income, and the price shock of the last few years has not reversed. Many households are still working and paying their bills, but the margin for error—savings, flexibility, breathing room—has eroded, even for those earning what used to be a comfortable salary.

Is it my fault that I’m struggling to keep up?

No. The financial math changed dramatically for everyone. When prices reset higher across essential categories and wages didn’t catch up, the pressure became structural, not personal. The fact that you’re managing at all under these conditions is a sign of resilience, not failure.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.