How to Recover Financially in Your 50s in Canada

Quick Answer:

Financial recovery in your 50s in Canada isn’t about catching up to some imaginary savings target. It’s about using the tools already built into the Canadian system, like CPP deferral, the TFSA, and strategic housing decisions, to turn a late start into a focused ten-year sprint. You have more leverage than you think, and the math is more forgiving than the anxiety.

The 3:00 AM Ceiling Stare: How Elena Found Her Financial “Second Wind” in Canada

Elena lay awake in her Coquitlam home, staring at the popcorn ceiling. It was 3:14 AM. She wasn’t counting sheep; she was counting how to recover financially in your 50s while the clock ticked loudly in the dark. In her head, the lack of loonies felt louder than the relentless British Columbia rain drumming against the window, a rhythmic reminder of the damp chill she felt in her own bones every time she looked at her bank balance.

At 54, Elena felt like she was stuck in a “Sandwich Generation” panini press. Her youngest, Marcus, was finishing his undergrad and eyeing a master’s degree at UBC, a dream that came with a five-figure price tag. Meanwhile, her 86-year-old mother in Nova Scotia was starting to need more than just a weekly phone call; she needed home care that the provincial system didn’t fully cover.

Elena’s RRSP statement, which arrived in the mail that afternoon, looked more like a grocery receipt from Loblaws than a retirement fund. “I’m behind,” she whispered to the dark. “I’ve spent twenty years building a life for everyone else, but I forgot to build the exit strategy for me.”

If that 3:00 AM panic feels familiar, you’re in good company. In Canada, we’re often told the “Golden Years” require a magic million-dollar pile and a clear path to Florida for the winter. But for those of us hitting our mid-50s with more memories than math on our side, the urgent need to recover financially in your 50s can feel like an impossible climb.

The good news? Canada has some unique levers, hidden in our housing, our pensions, and our tax codes, that can turn a “behind” into a “win” faster than a Zamboni clears the ice after a rough period.

The “Sandwich” Trap: Why Elena’s Bank Account Was Deflating

Before Elena could fix her future, she had to look at the leaks in her present. She realized she had become the family’s “Chief Financial First Responder.” Every time Marcus needed help with his car insurance or her mother needed a new specialized chair, Elena reached into her line of credit.

“I felt like I was failing everyone if I said no,” Elena admitted over coffee with a friend. “But every time I swiped that card, I felt a piece of my future retirement disappearing.”

She realized she was falling for the “Sandwich Trap.” It wasn’t a personal failure; it was a systemic reality. In fact, I’ve written before about why even the most responsible Canadians feel this intense financial pressure in their 50s, and how this trap is designed to feel almost impossible.

The “Sandwich Trap” is a uniquely Canadian struggle in 2026. With the cost of living in hubs like Vancouver and Toronto skyrocketing, adult children are staying home longer, and aging parents are living longer. Elena had to learn the “Oxygen Mask Rule”: You cannot pour from an empty cup.

For some parents, the pressure does not stop in their fifties. It follows them into their sixties, when they may start earning new income to support adult children.

For many people, recovery in midlife also means learning to set financial boundaries with adult children without drowning in guilt.

She had the “Real Talk” with Marcus. She didn’t cut him off, but she set boundaries. They sat down and looked at the UBC tuition together, finding grants and student loan options she hadn’t known existed. By stopping the “leak” of small $50 and $100 transfers, Elena suddenly found an extra $400 a month. In the world of compound interest, that $400 was a seed that needed planting.

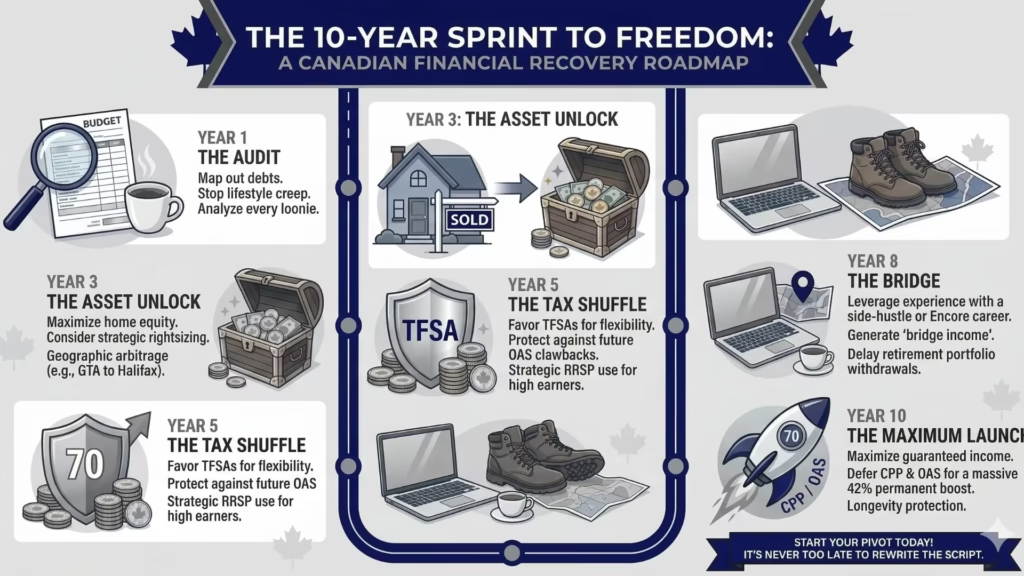

The Big Pivot: Trading the “Forever Home” for Forever Freedom

For Elena, the breakthrough didn’t come from a hot stock tip; it came from looking at her backyard. Her four-bedroom house was worth nearly $1.6 million. But the property taxes were creeping up, the heating bill for those empty bedrooms was astronomical, and the cedar deck was begging for a $10,000 renovation.

She was “house rich and cash poor.” She was living in a piggy bank she couldn’t open.

She began researching “B-Towns”, smaller, vibrant Canadian cities where life was slower and cheaper. She took a weekend trip to Kingston, Ontario, and another to the Annapolis Valley in Nova Scotia. She realized that by selling her Coquitlam home and buying a charming two-bedroom bungalow in a secondary market for $700,000, she could clear her mortgage and put nearly $900,000 in cash into her retirement fund.

She also knew that a real recovery plan could not ignore housing costs, especially mortgage decisions after the Bank of Canada rate hold.

The “Rightsizing” Reality Check

| Current Situation (The Grind) | The Big Pivot (The Recovery) | The Result |

| Home: 4-BR in GVA ($1.6M) | Home: 2-BR in Kingston/Kelowna ($700k) | $900,000 Cash Injection |

| Monthly Costs: $4,500 (Mortgage/Tax/Maint) | Monthly Costs: $2,200 | $2,300/mo Savings |

| Stress Level: High (The 3 AM Stare) | Stress Level: Low (The Lake View) | Peace of Mind |

“I wasn’t losing my home,” Elena realized. “I was trading four walls I didn’t use for a life I could actually afford to live.”

The Debt Snowball in the Great White North

With the house sale in progress, Elena turned her sights on her “silent wealth killers”: a $12,000 credit card balance at 21% interest and a $22,000 SUV loan.

“I was paying the CRA and the banks more in interest than I was paying myself,” she noted. She used the Debt Avalanche method. Since she knew her credit card was costing her the most, she attacked it with every spare loonie she saved from Marcus’s new independence.

Once that 21% interest was gone, she felt like she’d given herself a massive pay raise. In Canada, debt is the primary obstacle to a late-stage recovery. By clearing those balances in her mid-50s, she ensured that her “Ten-Year Sprint” would be spent building wealth, not just treadmilling against interest rates.

The “Encore Career”: Elena’s Digital Side-Hustle Bridge

This is where Elena really took control. She knew she couldn’t just “save” her way to a comfortable retirement in ten years, she needed to earn her way there. But she didn’t want to stay in her stressful corporate 9-to-5 until she was 70.

She decided to launch an Encore Career. She took her 25 years of experience in administrative logistics and turned it into a high-end consulting business she could run from her laptop.

“I didn’t realize how much the world wanted ‘Canadian experience,'” she laughed. She started exploring specific platforms tailored to her skills and the Canadian market:

- Consulting & Project Management: She set up a profile on Upwork and Freelancer.ca, targeting Canadian small businesses that needed part-time operations help but couldn’t afford a full-time executive.

- Specialized Tutoring: Because she was great with numbers, she joined Paper.co and TutorMe, helping Canadian high schoolers with their business studies.

- The “Workforce.ca” Pivot: She kept an eye on Indeed Canada and Workforce.ca for “fractional” roles, positions that only required 15 hours a week but paid a professional hourly rate.

- Canadian Creative Hubs: For those with a creative bent, she recommended Fiverr or 99designs, but specifically looking for “Shopify Experts” or “E-commerce Consultants,” roles that are booming in the Canadian tech landscape.

By earning just $2,000 a month through this gig work, Elena did something brilliant: she covered her basic living expenses without touching her savings. This allowed her RRSP to sit in the market and grow completely undisturbed for another decade.

Playing the Long Game with Uncle Sam (and Aunt Ottawa)

Elena’s next move was about extreme patience. Most of her friends were counting down the days until they could take their Canada Pension Plan (CPP) at age 60. “Get it while you can!” they’d say over bridge games.

But Elena did the math with a planner. In Canada, taking your CPP at 60 results in a permanent 36% reduction in your monthly check. However, if she used her “Encore Career” income to bridge the gap and waited until age 70, her check would be 42% higher than the standard age-65 amount.

“If I live to be 90,” Elena calculated, “that’s an extra $150,000 in my pocket just for being patient.”

She also learned about the Old Age Security (OAS) boost. At age 75, the government automatically increases your OAS by 10%. By planning for her “Older Self,” Elena was ensuring she would have a massive, inflation-protected “raise” right when she might need it most for healthcare or support.

RRSP vs. TFSA: The Late-Stage Tax Shuffle

One afternoon, Elena sat down with her tax software and realized she was falling into a common Canadian trap. She was dumping money into her RRSP to get a tax refund now, but she wasn’t thinking about the “tax bill” waiting for her at age 71.

“If my RRSP is too big,” she realized, “the CRA will take a huge chunk of it in taxes, and it might even trigger an OAS Clawback.”

In 2026, the OAS Minimum Income Recovery Threshold is $95,323. If Elena’s total income in retirement went over that, the government would start taking 15 cents of every OAS dollar back.

She pivoted her strategy:

- The TFSA First: She maximized her Tax-Free Savings Account (with the 2026 limit of $7,000). Since withdrawals from a TFSA don’t count as “income,” she could take out money for a trip to Italy and it wouldn’t affect her OAS eligibility.

- The RRSP “Meltdown”: She planned to start taking small, strategic amounts out of her RRSP (using her 2026 contribution room of up to $33,810) while her income was lower, “melting it down” slowly to avoid a massive tax hit at age 71.

The “Cash Wedge”: Elena’s Sleep-at-Night Strategy

The final piece of the puzzle was protecting her nest egg from market jitters. Elena didn’t want a bad month on the TSX to ruin her plans.

She adopted the Cash Wedge Strategy. She didn’t put all her money in the “scary” stock market. Instead, she divided her “Recovery Fund” into three buckets:

- Bucket 1 (The Loonie Bin): One year of cash in a High-Interest Savings Account (HISA). This was for groceries and gas, no matter what the market did.

- Bucket 2 (The Safety Net): Two years of income in safe Guaranteed Investment Certificates (GICs).

- Bucket 3 (The Growth Engine): The rest went into low-cost ETFs and dividend-paying Canadian stocks.

This meant that even if the world went sideways, Elena had three years of “safe” money to live on while she waited for her stocks to bounce back. For the first time in years, she stopped checking the news with a knot in her stomach.

Health as Wealth: The Final Pivot

Finally, Elena realized that the best financial plan in the world is useless if you aren’t around to enjoy it. She started investing in her “Physical Capital.” She traded her expensive gym membership for daily hikes on the local trails and joined a community garden.

She also used a small portion of her “house profit” to make her new home “future-proof.” She installed a walk-in shower and wider doorways now, while she was healthy.

“In 2026, a retirement home in Ontario can cost $5,000 a month,” she noted. “By spending $15,000 now to stay in my own home longer, I’m saving myself hundreds of thousands in the long run.”

She knew that for people rebuilding without strong workplace benefits, private health insurance in Canada for families without workplace benefits may need to be compared carefully against actual health spending and emergency savings.

Key Facts: Key Numbers for Late-Stage Recovery in Canada

- The TFSA annual contribution limit for 2026 is $7,000 (Canada Revenue Agency). Withdrawals from a TFSA are not counted as income and will not affect Old Age Security eligibility.

- The RRSP dollar limit for 2026 is $33,810, or 18% of the previous year’s earned income, whichever is lower (Canada Revenue Agency). Unused contribution room carries forward from previous years.

- Taking CPP at age 60 results in a permanent 36% reduction, while deferring to age 70 increases the monthly benefit by 42% over the standard age-65 amount (Service Canada).

- The OAS pension recovery tax (clawback) begins when net world income exceeds $95,323 for the 2026 tax year (Canada Revenue Agency). For every dollar above this threshold, 15 cents of OAS is repaid.

- Canadians aged 75 and over receive a 10% increase to their OAS pension, with the full clawback threshold set higher for this group (Service Canada).

The Verdict: It’s Never Too Late to Rewrite the Script

Elena still stares at the ceiling sometimes, but now it’s because she’s planning a summer trip to see her mom in Nova Scotia, not because she’s worried about the hydro bill.

Financial recovery in your 50s isn’t about finding a magic wand or winning the Lotto Max. It’s about being brave enough to change the plan. It’s about realizing that in Canada, we have the tools, the TFSA, the CPP deferral, the rightsizing opportunities, to build a beautiful second act.

The “Ten-Year Crunch” isn’t a life sentence; it’s an invitation to pivot. So, put the kettle on, grab your latest statement, and start your own sprint. Your 65-year-old self is waiting to thank you for what you do today.

Frequently Asked Questions:

Is 55 really “too late” to start saving in Canada?

Honestly? No. While you might not have forty years of compound interest on your side, you likely have your highest earning years ahead of you. In Canada, a decade of aggressive saving, combined with “rightsizing” your home and delaying your CPP, can create a massive swing in your favor. It’s not about how long you’ve been saving; it’s about how strategically you use the next ten years.

Should I prioritize my RRSP or my TFSA if I’m behind?

It depends on your “tax bracket” today versus tomorrow. If you’re a high earner now, the RRSP gives you an immediate tax refund you can reinvest. However, if you’re worried about the OAS Clawback (which starts if your income hits $95,323 in 2026), the TFSA is your best friend. TFSA withdrawals are “invisible” to the CRA, meaning they won’t trigger that clawback.

What exactly is a “B-Town” move?

It’s a strategic move to a city that’s one tier below the major hubs like Vancouver or Toronto. Think Kingston, Kelowna, or even Halifax. By selling a high-value home in a “Tier A” city and buying in a “B-Town,” you can often pocket $500,000 to $900,000 in cash while still enjoying a great lifestyle.

Why wait until 70 to take CPP? I might need the money now.

The math is hard to ignore: waiting until 70 gives you a 42% permanent increase over the standard age-65 amount. If you’re healthy, that extra monthly “pay raise” is the best inflation-protected insurance you can buy. Use an “Encore Career” or a side-hustle to bridge the gap if you can, your 85-year-old self will thank you.

How much can I actually save in 2026?

For the 2026 tax year, the TFSA limit is $7,000, and the RRSP maximum is $33,810 (or 18% of your previous year’s income). If you have “carry-forward” room from years you didn’t contribute, you might be able to put away even more. Check your “My Account” on the CRA website to see your exact “secret” savings room.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice.

Tax laws and government thresholds, such as the 2026 OAS clawback limit of $95,323 and the RRSP limit of $33,810, are subject to change by the Canada Revenue Agency and Service Canada. Every individual’s financial situation is unique.

Individual circumstances vary, so please consult with a Certified Financial Planner (CFP) or qualified tax professional before making significant financial decisions.