RRSP vs TFSA Canada: Which Is Right for You?

Quick answer

The RRSP vs TFSA Canada question doesn’t have a single correct answer. The better account depends on your current income, your expected income later in life, how much flexibility you need, whether your employer matches contributions, and how stable your cash flow actually is. For most households, the real question isn’t which account is better in theory. It’s which account makes sense given what’s actually happening right now.

🎧 Pressed for time? Listen to a summary of the heart of this story. Full data and guidance are detailed in the article below.

The RRSP deadline notice sat on the kitchen counter for three weeks. Farah kept moving it from one spot to another, not because she’d forgotten about it, but because she wasn’t sure what to do.

She and Imran were doing reasonably well by most measures. He worked in construction management in Calgary. She ran a small bookkeeping practice from home, mostly for local tradespeople and small shops. Between them, they brought in a solid income. But solid didn’t mean there was room for everything at once.

The mortgage renewal was coming up in the spring. Their daughter’s daycare had just gone up by eighty dollars a month. The furnace had made a sound in January that cost eight hundred dollars to fix. And every trip to the grocery store felt like it ended with more bags left in the car than were carried inside.

There was some money available. Maybe five or six hundred dollars a month, if they were careful. The question was what to do with it. RRSP, TFSA, a bit more on the mortgage. Or just keep it liquid, because life felt unpredictable lately.

The Real Question Behind the Search

When most people search “RRSP vs TFSA,” they aren’t looking for textbook definitions. They already know, roughly, that one gives a tax deduction and the other doesn’t. What they’re really asking is something harder: if I have a limited amount of money and I can’t do everything at once, where should the next dollar go?

It’s a fair question, and it deserves a clear answer rather than a chart of features. Not a brochure version of these accounts, but an honest look at how they work, when each one fits, and why the right choice looks different depending on your actual life.

What Each Account Actually Does

Both an RRSP and a TFSA are account types, not investments. The money you put inside either account can be invested in mutual funds, GICs, ETFs, savings deposits, and other eligible products. The account itself is the tax wrapper. The investments inside it are a separate decision.

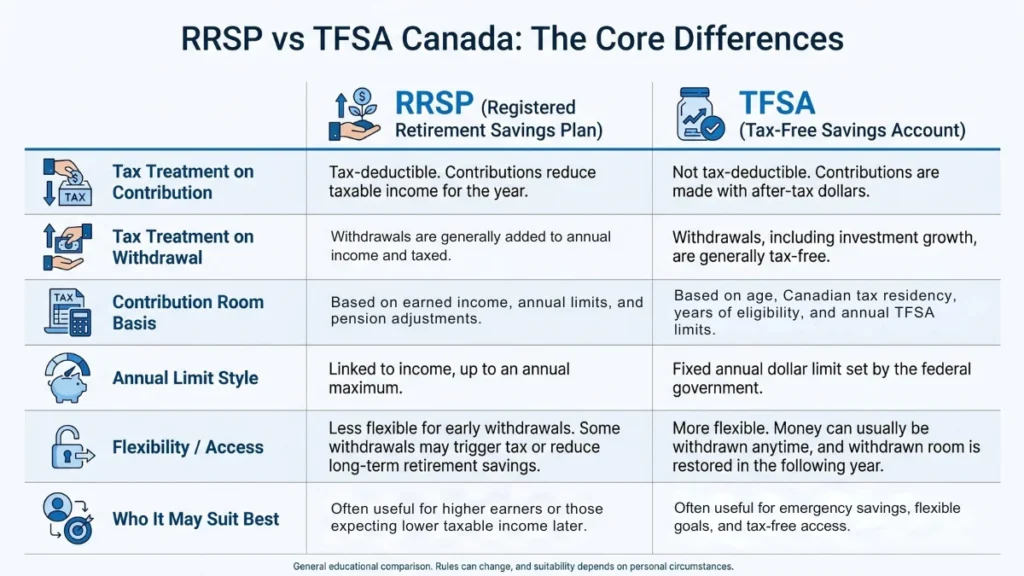

An RRSP, or registered retirement savings plan, works on a deferred-tax model. When you contribute, you may be able to deduct that amount from your taxable income for the year. That can reduce what you owe at tax time, or increase your refund. The investments inside the RRSP grow without being taxed year by year. When you eventually withdraw the money, those withdrawals are treated as income and taxed at your rate at that time.

Your RRSP contribution room is generally based on 18 percent of your earned income from the previous year, up to the annual dollar limit, and adjusted for any pension factors from a workplace plan. Unused room carries forward, so if you haven’t contributed much in past years, you may have more room available than you think. By the end of the year you turn 71, you’ll need to convert your RRSP, most commonly into a RRIF, a registered retirement income fund that pays out taxable income over time.

A TFSA, or tax-free savings account, works differently. You contribute with after-tax dollars, so there’s no deduction and no effect on your tax return when you put money in. But the growth inside the account is tax-free, and when you take money out, it’s also tax-free. There’s no income requirement to build TFSA room. Even someone with no earned income can accumulate TFSA room if they meet the age and residency requirements. Withdrawals generally create new contribution room the following January, so the room isn’t permanently lost when you use it.

The Tax Timing Question

The plain-English logic behind the rrsp vs tfsa canada decision comes down to one thing: tax timing.

If your income is higher now than it’s likely to be in retirement, an RRSP contribution lets you claim a deduction at today’s higher tax rate and pay tax on withdrawals later at a potentially lower rate. The money effectively moves from a high-tax period of your life into a lower-tax one.

If your income is lower now, or you’re early in your career, or you expect to earn significantly more in the coming years, then the RRSP deduction may not be especially powerful right now. A TFSA contribution means you’re putting in after-tax dollars at a lower rate and taking out tax-free money later, which can work out similarly or better, depending on your circumstances.

When current and future tax rates are roughly the same, the two accounts can produce similar results, particularly if the RRSP refund is handled thoughtfully. The RRSP’s advantage tends to weaken when the refund gets spent on ordinary expenses rather than reinvested or applied to debt.

Before going deeper, it may help to step back and think about what your next dollar needs to do. This RRSP vs TFSA decision helper does not calculate tax, refunds, contribution room, or investment returns. It simply helps you think through which account may fit your current household situation better.

RRSP vs TFSA Real-Life Fit Calculator

RRSP vs TFSA Real-Life Fit Calculator

Answer ten practical questions to see whether an RRSP, TFSA, both, or basic financial stability may deserve your attention first.

Your result

Three questions worth sitting with

If you’ve only recently arrived and still need to set up basic banking, our guide to the best bank for newcomers in Canada can help you compare first-account options more clearly.

When an RRSP May Fit Better

There are situations where directing money into an RRSP tends to make more sense.

If you're in a higher income bracket now and expect your income to be lower in retirement, the RRSP deduction is doing real work. You're shifting taxable income from an expensive tax year into a cheaper one. For people in peak earning years, especially mid-career professionals or dual-income households earning above the median, this logic can be worth taking seriously.

Employer RRSP matching changes the calculation significantly. If your employer matches your RRSP contributions up to a certain percentage, that match is part of your compensation. Not capturing it is leaving earned pay on the table. For many households, this tends to override most other considerations, unless you genuinely have no RRSP room yet.

Some families with children may also find the RRSP particularly useful. RRSP contributions can reduce your adjusted family net income, which affects income-tested benefits including the Canada Child Benefit. Depending on income, family size, and contribution amount, this can add meaningful value beyond the tax deduction alone. The details vary, and it's worth checking your specific situation rather than assuming the benefit will be substantial.

Farah and Imran, for instance, are both earning reasonably well. If Imran's income puts him in a bracket where the deduction genuinely reduces his tax by a meaningful amount, and their RRSP room is there, this may be a year where an RRSP contribution deserves serious consideration, particularly if there's already some emergency cushion in place.

For people who know they tend to dip into savings under pressure, the RRSP's relative lack of flexibility can also be useful. It creates a barrier. That's not weakness. It's self-knowledge, and it's a legitimate reason to prefer one account over another.

When a TFSA May Fit Better

The TFSA is often described as the simpler account, and it sometimes gets treated as the lesser one. It isn't. For many households, it's the smarter first choice.

If your income is lower or unstable, the TFSA wins on flexibility alone. There's no deduction to lose if your income drops. You can access the money if you need it. You don't have to guess what your future tax rate will be.

If you don't have emergency savings yet, a TFSA is generally the right place to build them. Keeping three months of essential expenses accessible and growing tax-free gives you a financial floor. Without that floor, a single unexpected bill, a car repair, a medical expense, a sudden income gap, can push you onto credit cards, which erodes everything else you're trying to do.

People concerned about benefit clawbacks in retirement can also benefit from TFSA withdrawals. Because TFSA withdrawals aren't counted as taxable income, they don't affect Old Age Security or Guaranteed Income Supplement calculations the way RRSP or RRIF withdrawals do. For lower-income retirees in particular, this can matter quite a bit.

The TFSA is also genuinely useful for medium-term goals, things that aren't quite retirement but aren't immediate either. A down payment addition. A car you know you'll need. A business cushion. Money that needs to grow and stay accessible.

And if you're earlier in your career or expect your income to rise significantly, preserving your RRSP room for higher-earning years while building TFSA savings now can be a reasonable approach.

The Refund Trap

The RRSP refund is one of the most emotionally powerful features of the registered retirement savings plan, and one of the most misunderstood.

When you make an RRSP contribution, you may receive a tax refund or pay less at tax time. That can feel like found money. It isn't. It's a deferral. The government is returning tax you overpaid during the year because you've now deducted your RRSP contribution. But the money inside the RRSP will be taxed when you eventually withdraw it. The refund is not a bonus. It's an advance on future tax savings.

The RRSP tends to work best when the refund is reinvested, used to pay down high-interest debt, or applied in a way that strengthens the household's financial position. When the refund goes toward regular spending, the long-term advantage of the RRSP narrows. This isn't meant to judge anyone. Sometimes bills are real and the refund genuinely helps with immediate pressure. But it's worth understanding what you're actually working with.

The Flexibility Question

For Farah and Imran, the flexibility issue is real. Their income is decent but not immune to disruption. A slow quarter for Farah's bookkeeping clients. A project delay for Imran. A child who gets sick and needs one parent home for a week. These things happen.

In households where cash flow can shift, having money locked into an RRSP can feel genuinely stressful. It's possible to withdraw from an RRSP early, but those withdrawals count as taxable income, and the contribution room doesn't come back. You've essentially cashed out a piece of your future tax savings.

TFSA withdrawals don't carry that cost. The room comes back the following January. You're not penalised for using money you've saved when you actually need it.

This is one reason why financial flexibility matters as much as tax efficiency for many ordinary households. Efficiency on paper doesn't help much if the plan requires carrying a credit card balance because you can't touch your registered savings.

Newcomers and Contribution Room

The contribution room rules work differently for newcomers to Canada, and it's worth understanding them clearly before putting money anywhere.

RRSP room is tied to Canadian earned income from the previous tax year. If you arrived in Canada in 2024 and started working, you generally won't have RRSP room until after you file your 2024 tax return in 2025. Contributing to an RRSP before you have the room creates an over-contribution, which CRA can penalise.

TFSA room doesn't work the same way. It begins to accumulate based on Canadian tax residency, age, and eligibility. Newcomers don't automatically receive all the room that has accumulated since 2009. The room starts building from the year you become an eligible Canadian tax resident.

This makes the TFSA especially practical during the settlement stage. Housing deposits, furniture, transportation, remittances to family abroad, and the general financial unpredictability of a first year in a new country make flexibility genuinely valuable. A TFSA can hold those emergency savings without the complications of managing RRSP room you may not have yet.

If you've recently joined an employer offering a group RRSP with matching, it's worth checking your actual contribution room before assuming you can participate fully. Employer plans can be valuable, but over-contributing can create tax problems that take time and paperwork to resolve.

Mortgage, Debt, and Cash Flow Pressure

Sometimes the real question isn't RRSP versus TFSA. It's whether the next dollar should go into a registered account at all.

For households facing mortgage renewal at higher rates, carrying credit card balances, or managing a tight monthly budget, registered savings contributions may not be the most urgent priority. Paying down high-interest debt offers a guaranteed return equal to the interest rate you're avoiding. That's often better math than a modest investment return, particularly after tax.

At the same time, if your employer offers RRSP matching and you're not capturing it, that's worth reconsidering even in tighter months. Matching is compensation, and not taking it has a real cost.

The answer for households under cash flow pressure isn't always "save less." For some, it's "save differently," keeping money flexible and accessible while still directing something toward the future. A modest TFSA contribution that stays accessible can serve a household better than a larger RRSP contribution that triggers a taxable withdrawal a few months later.

Common Mistakes Worth Knowing

Choosing an RRSP primarily for the refund, without thinking about what happens to that refund, can weaken the account's purpose over time.

Using RRSP contributions before building any emergency savings can create a situation where a single unexpected expense forces a taxable RRSP withdrawal, which costs more than the original deduction was worth.

Assuming the TFSA is only for short-term savings undersells it. It can hold long-term investments just as effectively as an RRSP, with different tax treatment.

Over-contributing to either account carries penalties. CRA charges one percent per month on excess RRSP contributions above the $2,000 buffer, and similar penalties apply to TFSA over-contributions. The TFSA buffer doesn't work the same way the RRSP buffer does. Re-contributing to a TFSA too soon after a withdrawal in the same calendar year is a common mistake that can trigger an over-contribution penalty.

CRA My Account contribution room figures can also lag in early months of the year, because financial institutions take time to report. Checking carefully rather than guessing is always the safer approach.

Treating the RRSP vs TFSA choice as a values question, as if one signals financial seriousness and the other doesn't, is a distraction. It's a timing and tax question. There's no hierarchy of virtue between the two accounts.

2026 Reality Check

- The 2026 RRSP annual dollar limit is $33,810. This is the national ceiling, not a personal guarantee. Your actual room depends on earned income from the previous year, adjusted for pension factors.

- The 2026 annual TFSA contribution limit is $7,000.

- For eligible Canadian residents who were 18 or older since 2009 and have never contributed to a TFSA, the cumulative TFSA room in 2026 can reach $109,000.

- RRSP room is generally calculated as 18 percent of previous-year earned income up to the annual limit, adjusted for any workplace pension plan factors.

- TFSA room does not depend on earned income, but it does require Canadian tax residency and meeting age and eligibility requirements.

Making the Decision: A Practical Framework

| Situation | RRSP may fit better | TFSA may fit better | Why |

|---|---|---|---|

| Higher income now, lower expected income in retirement | Often | Sometimes | The RRSP deduction may be more valuable now, while withdrawals may be taxed at a lower rate later. |

| Lower or unstable income | Not usually | Often | The RRSP deduction may be less powerful, while TFSA flexibility can matter more. |

| No emergency fund yet | Not usually | Often | Accessible savings may be more important than locking money away. |

| Employer RRSP matching available | Often | Sometimes | Matching is part of compensation and can make RRSP contributions more valuable. |

| Newcomer to Canada with limited RRSP room | Not usually | Often | TFSA room may begin with residency, while RRSP room takes time to develop through earned income. |

| Mortgage renewal or significant debt pressure | Sometimes | Sometimes | Cash flow protection or debt repayment may matter more than tax optimization. |

| Families with children and income-tested benefits | Sometimes | Sometimes | RRSP contributions may affect benefit calculations, depending on income and family size. |

| Concerned about future OAS or GIS calculations | Not usually | Often | TFSA withdrawals do not count as taxable income in retirement. |

| Expecting significantly higher income later | Not usually | Often | Preserving RRSP room for higher-earning years may make sense. |

| Credit card debt with high interest | Not usually | Not usually | Paying down high-interest debt may need attention before either account. |

Which Account Gets the Next Dollar

Farah eventually made a decision. She put three months of household expenses into a TFSA they'd been keeping too low, because the furnace incident had reminded both of them what an empty emergency cushion actually feels like. Then they made a modest RRSP contribution in Imran's name, enough to move his taxable income down slightly without locking away more than they could reasonably afford.

It wasn't optimised. It wasn't the textbook answer. But it fit what their life actually looked like in 2026.

The RRSP vs TFSA canada decision is ultimately about matching an account to your real circumstances, not finding a universally correct answer. Your tax bracket now, your expected income later, your cash flow, your employer's plan, your contribution room, your family situation, and your honest sense of how soon you might need access to the money all shape which account deserves priority.

Neither account is superior in the abstract. The TFSA is not just for small goals, and the RRSP is not automatically the more responsible choice. They solve different problems, and most Canadians will use both over the course of their working years. The question is which one makes sense given where you are right now.

Here are a few common questions Canadians ask when comparing RRSPs and TFSAs.

Frequently Asked Questions

Is it better to put money in a TFSA or RRSP if I'm not sure what my income will be?

If your income is uncertain or likely to change, a TFSA often makes more practical sense as a starting point. The flexibility to withdraw money without tax consequences gives you room to respond to whatever happens. You can always build RRSP contributions once your income and tax situation are clearer.

Can I contribute to both an RRSP and a TFSA in the same year?

Yes, if you have room in both accounts. Many households do contribute to both, sometimes in different proportions depending on what their income and cash flow allow that year. The key is knowing your actual contribution room in each account before you put money in.

What happens to my TFSA room if I withdraw money?

The room generally comes back the following January 1st. So if you withdraw $5,000 from your TFSA in August, you'll have that $5,000 of room restored when the new year begins. Putting it back in the same calendar year can create an over-contribution, so it's worth tracking carefully.

Should I use my RRSP refund to contribute to my TFSA?

Using an RRSP refund to fund a TFSA contribution is one way to make both accounts work together in the same year. It lets you benefit from the RRSP deduction while building tax-free savings at the same time. Whether it's the right move depends on your cash flow and whether other priorities, such as debt repayment or emergency savings, deserve the refund first.

If I'm new to Canada, which account should I use first?

For most newcomers, the TFSA is the more practical starting point. Your RRSP room may be limited or nonexistent in your first years in Canada, and the TFSA doesn't require earned income to accumulate room. It also gives you accessible savings during a period when settlement costs, housing transitions, and income unpredictability tend to be highest.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.