RRSP Canada Explained: What It Means for Your Money

Quick Answer

An RRSP (Registered Retirement Savings Plan) is a Canadian account designed for retirement savings. Contributions can lower your taxable income now, and the money inside grows without being taxed until you take it out. But it’s not free money, and it’s not always the right first move. Before contributing, it helps to understand your contribution room, your tax bracket, and whether your household cash flow can absorb locking money away.

🎧 Pressed for time? Listen to a summary of the heart of this story. Full data and guidance are detailed in the article below.

Sonia sat at the kitchen table in Ottawa with her laptop open and a cup of tea going cold beside it. Her two kids were finally asleep. Her husband, Ravi, was on a late shift. She had her Notice of Assessment pulled up on the CRA website, and the number beside “RRSP deduction limit” stared back at her like a question she wasn’t sure how to answer.

It was early February, and the RRSP Canada deadline was coming. She’d heard her coworker say she was “maxing out” her contribution to get a big refund. She’d seen posts online calling it the smartest move a Canadian can make. But Sonia’s mortgage payment had gone up after renewal last year, groceries for the four of them were running close to $1,200 a month, and the car needed brakes. Putting thousands of dollars somewhere she couldn’t easily touch felt risky. Not putting it anywhere felt worse.

If you’ve ever felt caught between the pressure to save for retirement and the pressure to survive the month, this article is for you. Understanding how an RRSP in Canada actually works, not just the headlines but the mechanics and the trade-offs, can make tax season feel a lot less like a guessing game.

What an RRSP actually is

There’s a common misunderstanding that trips up a lot of people right at the start. The Registered Retirement Savings Plan (RRSP) is not an investment. It’s a type of registered account, a container approved by the Canada Revenue Agency. Inside that container, you can hold different kinds of eligible investments: savings deposits, GICs, mutual funds, ETFs, bonds, and certain stocks, among others.

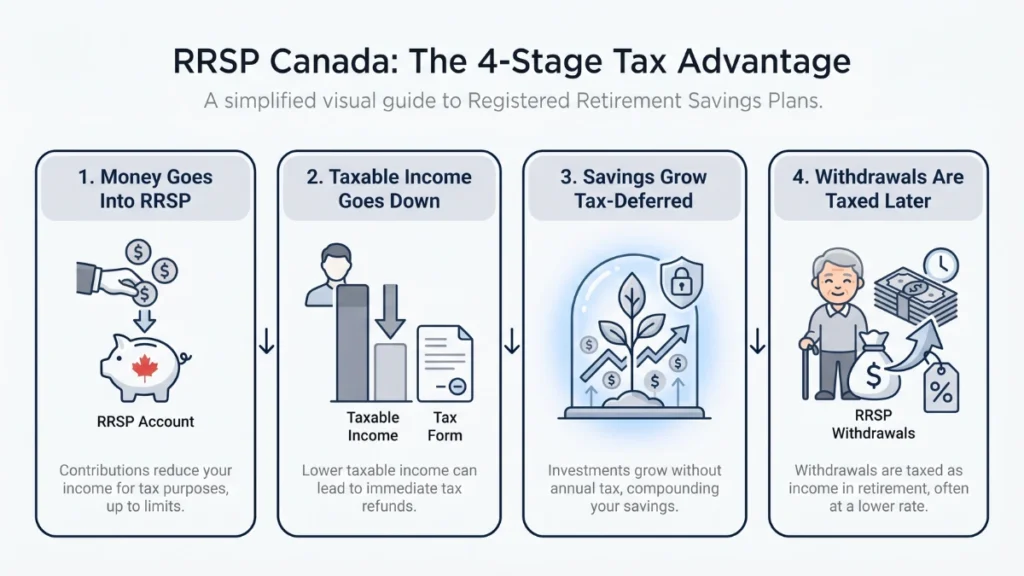

The reason people use it is the tax treatment. When you put money into an RRSP, you can deduct that amount from your taxable income for the year. If you earned $75,000 and contributed $5,000, your taxable income drops to $70,000. That means you owe less tax, and the difference often comes back as a refund.

The investments inside the RRSP grow without being taxed along the way. No capital gains tax, no tax on dividends or interest, as long as the money stays inside the account. This is what’s meant by tax-deferred savings. The tax doesn’t disappear. It waits. When you eventually withdraw the money, usually in retirement, it gets added to your income and taxed at whatever rate applies then.

For someone like Sonia, whose household earns a decent combined income now but expects to live on less in retirement, that deferral can work in her favour. She pays less tax now, at a higher rate, and more later, at a lower one. The gap between those two rates is where the real benefit lives.

Why the tax refund confuses people

This is the part that causes the most trouble, and almost nobody talks about it clearly enough.

When Sonia’s coworker said she was contributing to get a “big refund,” she wasn’t wrong exactly. But the refund isn’t a bonus. It’s a return of tax you’ve already paid, triggered by the deduction your RRSP contribution creates. Think of it less as the government giving you money and more as the government adjusting the bill because you’ve agreed to pay later.

The problem comes when people treat the refund like a windfall. If you contribute $8,000 and get a $2,800 refund, then spend that refund on a trip or a new TV, you’ve weakened the long-term power of the RRSP. The math behind the plan assumes you’ll reinvest the refund or use it in a way that strengthens your financial position. Spending it casually turns a smart deferral into a partial loss.

This isn’t about shaming anyone. Life is expensive. Sometimes a refund goes straight to the credit card or the furnace repair, and that’s reality. But it helps to know what the refund actually is before deciding what to do with it. It’s not a reward for saving. It’s the other side of a future tax bill.

How contribution room works

Your RRSP contribution room isn’t a fixed number that applies to everyone. It’s personal, and it changes every year.

In general, your new room for any given year is 18% of your earned income from the previous year, up to an annual dollar limit set by the CRA. For the 2025 tax year, that limit is $32,490. For 2026, it rises to $33,810. Most people won’t hit those ceilings. If you earned $65,000 last year, your new room would be around $11,700, minus any pension adjustment if your employer runs a workplace pension or group plan.

Unused room carries forward. If you didn’t contribute in past years, that space accumulates. Some people find they have $40,000 or $60,000 of unused RRSP contribution room waiting for them. That can feel exciting, but it doesn’t mean you should rush to fill it all at once. The room is yours. It doesn’t expire. It waits for a year when the deduction helps you the most.

The safest way to check your limit is your most recent Notice of Assessment from the CRA, or your CRA My Account online. Don’t guess this number. Contributing more than your available room, beyond a $2,000 lifetime buffer, triggers a 1% per month penalty on the excess. That adds up fast.

For Sonia, this was the first useful step. She logged in, found her number, and suddenly the decision felt more concrete. She didn’t have to figure out the whole retirement plan tonight. She just needed to know how much space she had and whether using some of it made sense this year.

When an RRSP can help

RRSPs tend to work best in certain situations, and it’s worth knowing whether yours fits.

If you’re earning a solid income now and expect to earn less in retirement, the RRSP tax deduction available in canada offers is genuinely valuable. You’re deferring tax from a high-rate year to a low-rate year. The wider that gap, the more the math works in your favour.

Employer matching is one of the clearest wins. If your employer offers to match RRSP contributions through a group plan, that’s an immediate return on your money before any investment growth even happens. Turning that down is, in most cases, leaving compensation on the table.

For families with children, the effect can go further. RRSP contributions lower your net income, and your net income is what determines your Canada Child Benefit. A well-timed contribution can increase your CCB payments for the following year. For some middle-income households with children, this can mean a noticeable increase in benefit payments, depending on income, family size, and the exact contribution. It’s not a trick. It’s how the benefit formula works. But it does mean the effective return on an RRSP contribution can be higher than the tax refund alone suggests.

Spousal RRSPs are another tool worth mentioning. If one spouse earns significantly more than the other, the higher earner can contribute to a spousal RRSP. They get the deduction at their higher marginal tax rate, and when the money is withdrawn in retirement, it’s taxed in the hands of the lower-earning spouse. Over time, this form of income splitting can reduce a household’s total tax burden considerably. There’s a three-year attribution rule to be aware of: if the lower-earning spouse withdraws within three calendar years of a contribution, the withdrawal gets taxed back to the contributor. It’s designed for long-term planning, not short-term manoeuvres.

When a TFSA may come first

Not everyone should prioritize the RRSP first, and that’s not a failure of planning. It’s common sense.

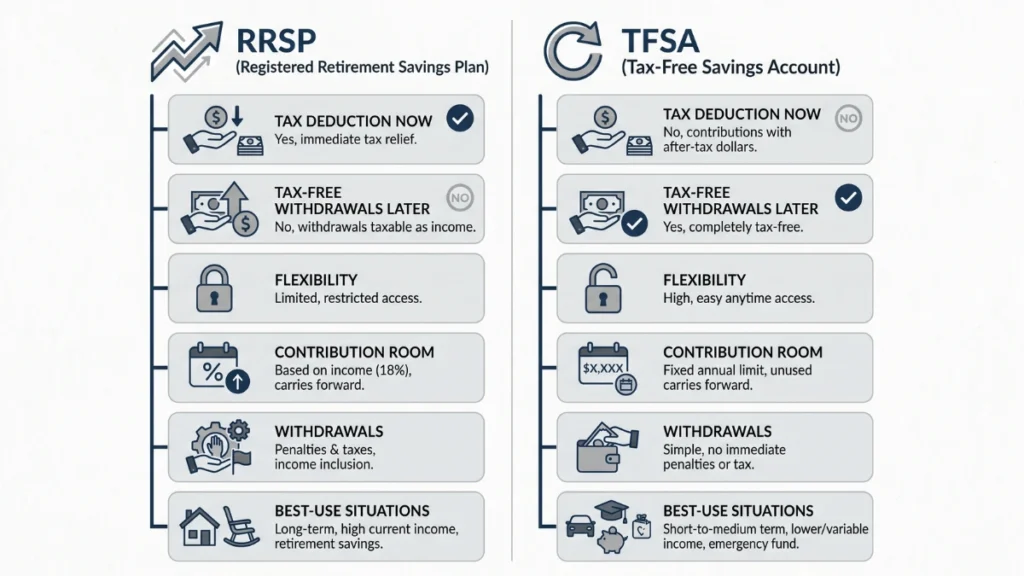

A TFSA (Tax-Free Savings Account) works differently. You contribute with after-tax dollars, so there’s no deduction and no refund. But the money grows tax-free, and when you take it out, you owe nothing. No tax on withdrawal. No impact on government benefits. And here’s a detail that matters more than people realize: if you withdraw from a TFSA, the contribution room comes back the following January. With an RRSP, that room is gone permanently once you withdraw.

For someone with an unstable income, or someone early in their career earning under $50,000 or so, the TFSA is often the better first move. The RRSP deduction is less powerful at a lower tax rate, and preserving that room for higher-earning years can pay off more later. If you don’t yet have a solid emergency fund, the TFSA’s flexibility matters more than the RRSP’s tax break, especially when monthly bills are already quietly draining the household budget.

For people whose cash flow is tight, the TFSA also avoids a psychological trap. The RRSP refund can feel like a reward that tempts you to spend, while the TFSA simply lets your money sit quietly and grow without drama.

This isn’t an either-or forever. Many households use both. The question is which one deserves the next dollar right now.

| Situation | RRSP may fit better | TFSA may fit better |

|---|---|---|

| Higher income now, lower income expected later | Yes | Sometimes |

| Lower or unstable income | Not always | Often |

| Need flexible emergency savings | Usually not | Yes |

| Employer offers matching | Often yes | Not for that match |

| New to Canada with no RRSP room yet | No | Often yes |

| Saving strictly for retirement | Often yes | Also possible |

If you are trying to decide whether an RRSP or a TFSA fits your life better right now, read our RRSP vs TFSA Canada guide.

What newcomers to Canada should know

If you’ve recently arrived in Canada, the RRSP can be confusing for a specific structural reason: your contribution room usually depends on earned income you reported in Canada during the previous year. If 2025 is your first year working here, you likely have zero RRSP room right now, regardless of what you earned elsewhere.

If you’re newly arrived and still setting up your first Canadian account, start with our guide to the best bank for newcomers in Canada before worrying about larger savings decisions.

This catches some newcomers off guard, especially those enrolled in employer group RRSP plans. If your employer starts matching contributions through a group plan before you’ve filed a Canadian tax return, you could end up over-contributing without realizing it. The penalty is 1% per month on anything beyond the $2,000 buffer, and it’s not forgiving.

The practical steps are straightforward. File a Canadian tax return as soon as you can, even if your income for the year was small. This activates your CRA file and begins building RRSP room for the following year. In the meantime, the TFSA is available to any Canadian resident 18 or older, regardless of income history, and it’s a solid place to start saving while your RRSP room catches up.

Withdrawals, age 71, and the future tax bill

One of the most overlooked parts of the RRSP conversation is what happens when money comes out.

Every dollar you withdraw from an RRSP is added to your income for that year and taxed accordingly. There’s also a withholding tax applied at the time of withdrawal: 10% on amounts up to $5,000, 20% on amounts between $5,001 and $15,000, and 30% on amounts above $15,000 (rates differ slightly in Quebec). This withholding isn’t the final tax bill. It’s a deposit toward it. If your actual tax rate is higher, you’ll owe more at filing time. If it’s lower, you may get some back.

There are two exceptions where early withdrawals don’t trigger immediate tax. The Home Buyers’ Plan lets first-time buyers withdraw up to $60,000 per person (up from the former $35,000 limit) to help with a down payment. The Lifelong Learning Plan allows up to $10,000 per year, to a maximum of $20,000, for full-time education. Both require repayment over time, and missing a repayment means that year’s amount gets added to your taxable income.

The other deadline that matters is age 71. By December 31 of the year you turn 71, your RRSP must be closed. The most common options are converting it to a RRIF (Registered Retirement Income Fund), purchasing an annuity, or withdrawing the balance. A RRIF forces minimum annual withdrawals that increase with age, and every withdrawal is taxable. For people with large RRSP balances, this can push them into higher tax brackets in their 70s and may trigger clawbacks on Old Age Security benefits.

Some retirees plan for this by drawing down their RRSP gradually in their early 60s, while their income is still low, to reduce the balance before the RRIF rules kick in. It’s not something to figure out alone, but it’s worth knowing about long before you’re 70.

Common RRSP misunderstandings

A few beliefs about RRSPs come up again and again, and they can quietly steer people in the wrong direction if nobody corrects them early enough.

The most basic one is thinking the RRSP itself is an investment. It isn’t. It’s a registered account, a container. The investments are what you choose to hold inside it, whether that’s GICs, mutual funds, ETFs, or something else. The account just provides the tax treatment.

The refund causes its own confusion. Many people treat it as a bonus from the government, but it’s really the present value of a future tax bill. You’ll pay tax on that money when you eventually withdraw it. Closely related is the assumption that withdrawals are tax-free. They aren’t. Every dollar that comes out of an RRSP is added to your taxable income for the year, unless it’s taken under the Home Buyers’ Plan or Lifelong Learning Plan with proper repayment.

There’s also a widespread belief that everyone should fill their RRSP before putting a dollar into a TFSA. For some households that’s true, but it depends entirely on your current tax bracket, your expected retirement income, your cash flow, and whether you might need flexible access to your savings before you retire. The TFSA is the better first step for a lot of people, and that’s not a lesser choice.

On the contribution side, some people assume they can put in whatever amount they want. They can’t. Room is capped annually and carries forward from previous years, and contributing beyond your limit, past a small $2,000 lifetime buffer, triggers monthly penalties. Newcomers to Canada face a version of this problem too. RRSP room is generally built on Canadian earned income from the previous year, which means someone who has just arrived may have no room at all, even if they’re already enrolled in a workplace plan.

Questions before you contribute

Before putting money into an RRSP, it helps to sit with a few honest questions. Not to overthink the decision, but to make sure the timing fits your life right now.

| Question | Why it Matters |

|---|---|

| Do I actually have contribution room? | Your Notice of Assessment or CRA My Account shows your personal limit. |

| Am I in a higher tax bracket now than I expect later? | RRSPs work best when today’s deduction is worth more than tomorrow’s withdrawal tax. |

| Do I have basic emergency savings? | If not, a TFSA might serve you better first, because you can access it without penalty. |

| Does my employer offer RRSP matching? | Matching can make a contribution much more valuable. |

| Will I need this money soon? | RRSP withdrawals are taxable, and the room usually does not come back. If flexibility matters, consider the TFSA. |

| Will I use the refund wisely? | The long-term benefit is stronger when the refund is saved, invested, or used to improve cash flow. |

| Could a spousal RRSP help our household? | If one partner earns significantly more, splitting future retirement income through a spousal plan can reduce overall taxes. |

Key Facts

Here are a few verified reference points worth keeping in mind this tax season.

- The RRSP annual dollar limit for the 2025 tax year is $32,490. For the 2026 tax year, it rises to $33,810.

- The deadline to make RRSP contributions that count toward your 2025 tax return is March 2, 2026.

- RRSP room is generally based on 18% of your previous year’s earned income, up to the annual limit, adjusted for pension factors.

- Your RRSP must be converted, withdrawn, or used to purchase an annuity by December 31 of the year you turn 71.

- The TFSA contribution limit for 2025 is $7,000. It is expected to remain $7,000 for 2026 based on current indexation.

What this really comes down to

Sonia didn’t end up making a decision that night. She closed the laptop, reheated her tea, and sat with what she’d learned. She checked her contribution room. She looked at what her employer matched. She thought about the mortgage, the kids, and whether the refund would actually get reinvested or quietly absorbed by the next round of bills.

That’s not indecision. That’s thinking clearly about money under real pressure, which is harder than any formula.

Understanding RRSP Canada doesn’t mean committing to a number tonight. It means knowing how the account works, what the refund really is, when the TFSA might make more sense, and what happens when the money eventually comes out. Those are the things that help turn tax-season pressure into a calmer money decision.

If you’re sitting at your own kitchen table running numbers while the house is quiet, you’re not behind. You’re doing the thing that actually matters. You’re paying attention.

Frequently Asked Questions

What is an RRSP in Canada and how does it work?

An RRSP is a registered account that holds eligible investments for retirement. Contributions reduce your taxable income for the year, and growth inside the account isn’t taxed until you withdraw. When you take money out, usually in retirement, it’s added to your income and taxed at your rate that year. The benefit comes from deferring taxes from higher-earning years to lower-earning ones.

What is the RRSP contribution limit for 2025 and 2026?

The annual RRSP dollar limit for the 2025 tax year is $32,490. For 2026, it’s $33,810. Your personal limit may be lower, depending on your earned income and any pension adjustments. Check your CRA My Account or your most recent Notice of Assessment for your exact number.

Should I contribute to an RRSP or a TFSA first?

It depends on your income, tax bracket, and whether you might need the money before retirement. If you’re in a higher tax bracket now than you expect to be later, the RRSP deduction is more valuable. If your income is lower, your cash flow is tight, or you need flexible access to savings, the TFSA is often a better starting point. Many households eventually use both.

Do newcomers to Canada have RRSP contribution room?

Usually not right away. RRSP room is generally based on Canadian earned income reported in the previous tax year. If you’ve just arrived, you likely have no room yet. Filing a tax return as soon as possible starts building your room for the following year. In the meantime, a TFSA is available to any Canadian resident aged 18 or older, regardless of income history.

What happens to my RRSP when I turn 71?

By December 31 of the year you turn 71, your RRSP must be closed. The most common options are converting it to a RRIF, purchasing an annuity, or withdrawing the full balance. A RRIF requires minimum annual withdrawals that are taxable. Planning for this transition well in advance can help avoid unexpected tax bills or benefit clawbacks later in retirement.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.