The Ontario Car Insurance Survival Guide 2026: What Every Driver Actually Needs to Know

Quick Answer

Ontario car insurance is mandatory, and Statistics Canada reported that Ontario and Alberta had the highest auto insurance premiums in Canada as of December 2024. FSRA’s October 2025 data shows an average annual premium of $2,164 across Ontario, $2,810 in the GTA, and $1,740 in rural Ontario, though individual premiums can vary widely by postal code, vehicle, coverage, and driving history. Every policy contains four mandatory coverages set by provincial law, plus optional add-ons that most drivers have never reviewed. Understanding what you are actually paying for, and what you can change, is the first step to taking control of your premium.

🎧 Pressed for time? Listen to a summary of the heart of this story. Full data and guidance are detailed in the article below.

Tariq was still sitting in his car in the driveway of his North York semi when he ended the call with his insurer. He’d phoned to ask a simple question about his renewal, something about a code on the paperwork he didn’t recognize. The agent had asked him three follow-up questions he couldn’t answer: what his liability limit was, whether he carried the Family Protection endorsement, and which drivers were currently listed on his policy. He’d been paying this bill faithfully for fourteen years. He couldn’t answer a single one.

He sat there with the engine off, staring at the renewal notice in his lap. There were line items he’d never read. Endorsement codes that meant nothing to him. A total that had gone up again, for reasons he could not explain to himself or to his wife, Amira, who would ask about it at dinner. He felt something close to embarrassment. Not anger. Just a quiet, private sense that he should know this by now.

That feeling, that slow realisation that you’ve been writing cheques for something you don’t fully understand, is more common than most people will ever admit. This Ontario car insurance survival guide is going to close that gap.

The Four Things Your Ontario Policy Must Cover By Law

Every auto insurance policy sold in Ontario must include four coverages. Not three. Not five. Four. They are set by provincial law, and no insurer can sell you a policy without them. If you understand what these four things do, you already know more than most drivers on the road.

Third Party Liability protects you if you cause an accident that injures someone else or damages their property. The legal minimum in Ontario is $200,000. That sounds like a lot until you see what happens in a courtroom. In Marcoccia v. Ford Credit Canada Limited, a jury awarded $16 million, with $13.9 million for future care costs alone.

In Pye v. Di Trapani, a 2023 verdict exceeded $1.07 million, plus another $1.1 million in legal costs and interest. A driver carrying only $200,000 in either case would have been personally responsible for the rest, potentially facing bankruptcy. Insurance professionals in Ontario almost universally recommend $1 million to $2 million in liability, and the premium difference between $200,000 and $1 million is often surprisingly small.

Statutory Accident Benefits provide medical care, rehabilitation, income replacement, and caregiver support after an accident, regardless of who caused it. This is the “no-fault” part of Ontario’s system: even if you’re the one who caused the collision, you still receive these benefits through your own policy. The structure of this coverage is changing significantly on July 1, 2026, with several benefits moving from mandatory to optional. For a detailed look at what these changes mean and why the system works the way it does, see our full breakdown: Why Your Ontario Car Insurance Went Up Again in 2026.

Direct Compensation Property Damage covers the damage to your vehicle when another driver is at fault for a collision, as long as the accident happens in Ontario and involves at least one other insured vehicle. Here’s where Ontario works differently from what most people assume. You don’t go after the other driver’s insurance company to get your car repaired. You go to your own insurer. That’s what “direct compensation” means: your insurer pays for your repairs, then settles with the other driver’s insurer behind the scenes.

This system speeds up the repair process, but it also means the quality of your own policy matters even when someone else hits you.

Uninsured Automobile Coverage protects you if you’re injured by a driver who has no insurance at all, or by a hit-and-run driver who can’t be identified. Picture this: you’re stopped at a red light on Hurontario Street, and a vehicle rear-ends you and drives off. No plate number. No way to find them. This coverage is what ensures you’re not left paying for your own medical bills and vehicle damage when the person who caused it has vanished.

Everything beyond these four is optional, and that is where most drivers are either overpaying or underprotected without ever realizing it.

What the Optional Add-Ons Actually Do

Once the four mandatory coverages are in place, the rest of your Ontario auto insurance policy is made up of optional add-ons. These are the parts most drivers have never consciously chosen. They were either bundled in when the policy was first written or quietly removed at some point to lower the premium. Understanding what each one does is how you stop guessing and start deciding.

Collision coverage pays to repair or replace your vehicle when you’re at fault, or when you collide with an object like a guardrail or a pothole. It doesn’t cover mechanical failure. It makes clear financial sense when your vehicle carries significant value, whether because it’s newer, financed, or leased. If your vehicle is older and fully paid off, there is a separate calculation worth doing, and we cover it in detail here: Car Insurance in Ontario: What Actually Lowers Your Premium (2026).

Comprehensive coverage handles threats that aren’t collisions: theft, vandalism, hail, a tree branch on your hood, a deer strike on Highway 7, or a cracked windshield. One thing worth knowing is that modern windshield replacement often involves recalibrating cameras and sensors built into newer vehicles. Auto-parts, maintenance, and repair costs rose 22.3% between 2019 and 2024 (Statistics Canada), and windshield replacements with ADAS sensor recalibration can cost significantly more than a simple glass swap on an older model.

Loss of Use or Rental coverage, known formally as the OPCF 20 endorsement, reimburses you for a rental vehicle, taxi, or transit costs while your car is in the shop after a covered claim. The annual cost is typically between $60 and $80, depending on the daily limit you select. This is one of the most commonly dropped optional coverages and one of the most commonly regretted, especially in households with only one vehicle. If your car is off the road for two or three weeks after a collision and you need to get to work or pick up kids from school, the cost of renting out of pocket adds up fast.

Accident Forgiveness prevents your first at-fault accident from triggering a premium increase at renewal. What it doesn’t do is travel with you. It’s not transferable between insurers. If you switch companies after using it, the new insurer will still see the collision on your driving record and price accordingly. This nuance surprises most people.

The Family Protection endorsement, OPCF 44R, is the add-on Ontario insurance professionals talk about more than any other. It extends your own policy’s liability limits to protect you and your family if you’re hit by an uninsured or underinsured driver. Concretely: you carry $2 million in liability. The driver who hits you only carries $200,000. Your damages total $1 million. Without OPCF 44R, you’re stuck with an $800,000 shortfall. With it, your own insurer covers the gap. The annual cost is nominal, often cited as less than the price of a daily cup of coffee. Insurance professionals widely consider it the highest-value endorsement available in Ontario.

Broker, Direct Insurer, or Comparison Website: Which One Actually Serves You

One of the most genuinely useful things you can understand about Ontario car insurance is the difference between the people and platforms selling it to you. They are not all the same, and the distinction matters more than most drivers realize.

A broker is an independent professional licensed by the Registered Insurance Brokers of Ontario, known as RIBO. Brokers represent multiple insurance companies, not just one. RIBO says brokers have a duty to provide consumers with professional advice and are expected to be well informed about the products they sell, meaning they can’t just sell you whatever pays the highest commission. RIBO also requires brokers to carry professional liability insurance and maintains a fidelity bond to protect client premiums.

You can verify any broker’s registration at ribo.com. If someone tells you they’re a broker and they’re not in RIBO’s registry, that’s a red flag worth paying attention to.

A direct insurer agent is different. They are employed by one insurance company and sell only that company’s products. They are not brokers and are not regulated by RIBO. This doesn’t make them untrustworthy, but it does mean their advice is naturally limited to a single market. If their employer’s rate for your postal code is high, they can’t show you a better option elsewhere. They simply don’t have access to one.

Comparison websites aggregate quotes from multiple insurers and present them side by side. They’re useful as a starting point, but they don’t cover the full market. Many large direct insurers don’t participate on comparison platforms. The quotes are real-time estimates, but the final premium is only confirmed after full underwriting. For a driver with a clean record and a simple history, a comparison site may surface everything they need. For more complex situations, it’s a starting line, not a finish line.

A driver with multiple vehicles, a recent claim, a young driver in the household, or a less-than-perfect record will almost always be better served by a RIBO broker who can access non-standard markets and advocate on their behalf.

Most Ontario drivers who find meaningfully lower premiums do so through a broker with access to multiple markets. The comparison site gets you started. The broker gets you across the finish line.

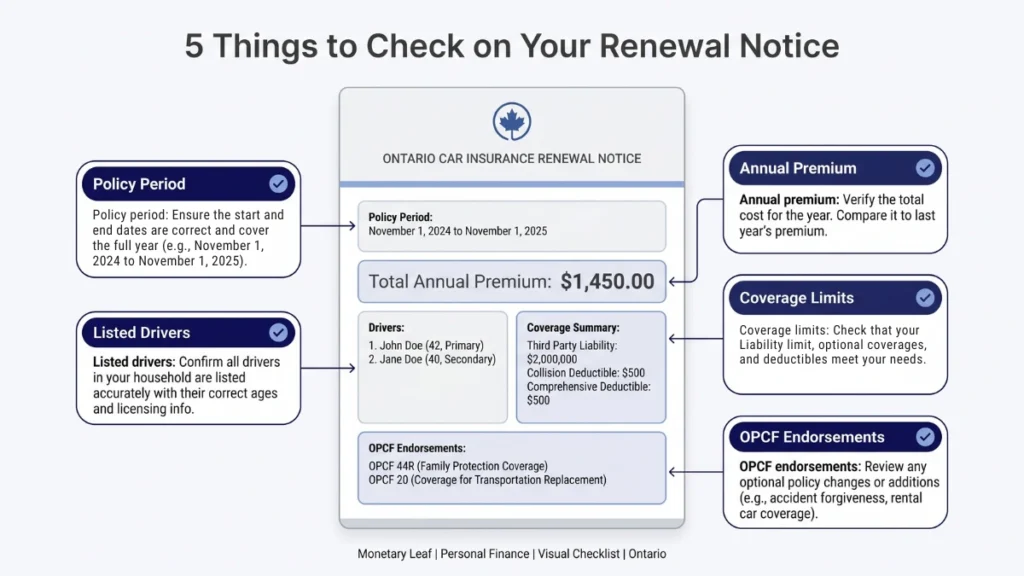

How to Read Your Renewal Notice Without a Translator

This is the section you’ll probably come back to. The next time your renewal arrives in the mail or in your inbox, open it beside this article. We’re going to walk through it together.

The declarations page is the summary sheet at the front of every renewal package, sometimes called the “dec page.” If you read nothing else, read this. It contains five numbers that matter: your policy number, the coverage period, the total annual premium, the vehicle description, and the primary listed driver. If any of these are wrong, everything that follows could be wrong too.

Coverage limits and deductibles are two separate numbers that control two completely different things, and confusing them is common. Your coverage limit is the maximum your insurer will pay. Your deductible is what you pay first before the insurer pays anything. If you have comprehensive coverage with a $1,000 deductible and your car suffers $4,000 in hail damage, you pay the first $1,000 and the insurer covers the remaining $3,000.

The premium breakdown shows how the total is divided among your different coverages. You should be able to see roughly what you’re paying for mandatory coverages separately from optional ones. If your comprehensive coverage alone costs $400 a year and your vehicle’s market value has dropped to $5,000, that’s a conversation worth having with your broker.

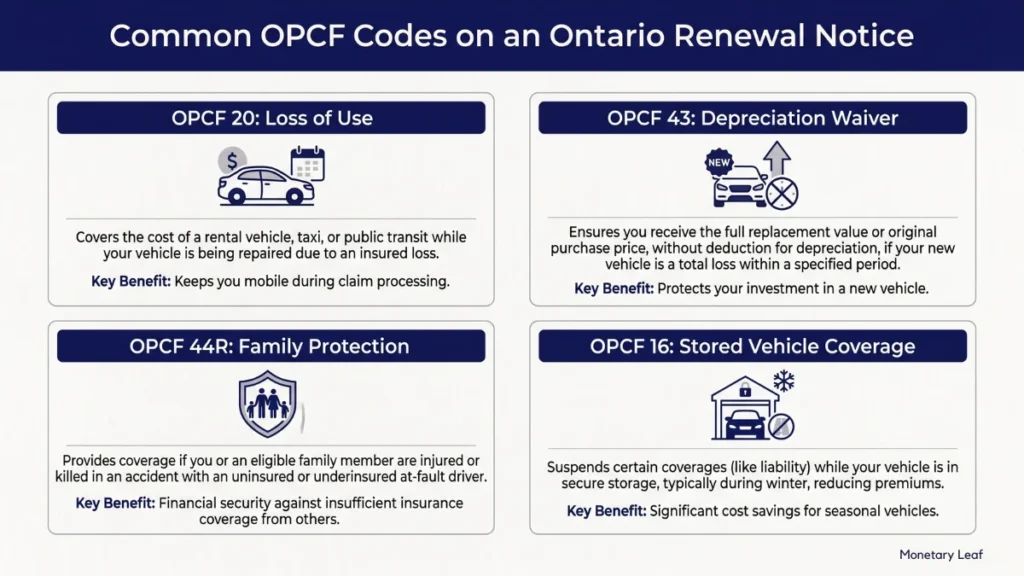

OPCF endorsement codes are the alphanumeric labels on your renewal that most people skip past without a second thought. They modify your standard policy. OPCF 20 is the Loss of Use endorsement that covers a rental car while yours is being repaired. OPCF 43 is the Limited Waiver of Depreciation, which protects the full purchase price of a newer vehicle if it’s totalled.

| OPCF Code | Plain-English Meaning | Why It Matters |

|---|---|---|

| OPCF 20 | Loss of Use | Helps cover a rental car, taxi, or transit while your vehicle is being repaired after a covered claim |

| OPCF 43 | Limited Waiver of Depreciation | Helps protect the purchase value of a newer vehicle if it is written off |

| OPCF 44R | Family Protection Endorsement | Helps protect you and your family if the at-fault driver has no insurance or too little insurance |

| OPCF 16 | Suspension of Coverage | Lets you pause certain parts of coverage when a vehicle is being stored and not driven |

OPCF 44R is the Family Protection endorsement described above. OPCF 16 is the Suspension of Coverage endorsement, which lets you pause parts of your policy when a vehicle is being stored. If any of these codes appear on your renewal and you don’t know what they mean, that’s a conversation to have with your broker before the renewal date passes.

The renewal versus new policy distinction is something most people never think about. The price on your renewal is not necessarily the best available price for your profile at that moment. Insurers don’t automatically reprice a policy to match what a new customer with identical details would pay. The renewal is an offer. Getting quotes elsewhere is how you find out whether it’s a good one.

Why Your Postal Code Changes Everything

This might be the most surprising section in this entire article.

Ontario car insurance rates in 2026 vary more by location than most drivers realize, and the mechanism behind this is the rating territory system, which divides the province by postal code. Each territory carries a base rate reflecting the historical claims experience in that area: collision frequency, theft rates, and how often claims are filed. Your postal code sets the floor before personal factors like your driving record are applied.

The gap between territories is enormous. According to FSRA data from October 2025, the average GTA premium was $2,810, while drivers in rural Ontario paid an average of roughly $1,740. That’s a baseline difference of more than $1,000 a year, before driving history enters the equation. Within the GTA, the numbers get sharper. Brampton’s average annual premium reached $3,802 by early 2026. Mississauga followed at $3,708. Toronto proper averaged $3,997 in 2025. Meanwhile, mid-sized cities like Barrie sat around $2,148, and a specific profile of a 40-year-old male driver with a clean record in Ottawa could find rates as low as $1,027.

Here’s what makes this real. Two identical drivers, same age, same vehicle, same driving record, same insurer, can pay $600 or more in annual premium difference based solely on where their car is parked overnight. Within the same city, the difference can be striking. In Brampton, the L6Z postal code averages $3,976 a year, while the L6P area in the same municipality averages $3,621, a difference of nearly 10% between neighbourhoods.

The location your insurer cares about is called the garaging address. It’s not where you work. It’s where the vehicle is kept overnight. If you’ve moved and haven’t updated this, you may be paying for a territory that no longer reflects your actual situation. It’s one of the most commonly forgotten policy details.

If you relocate within Ontario, always request a new quote before assuming your rate will stay the same. Moving from Mississauga to Hamilton, or from Toronto to Barrie, can produce a significant premium change in either direction. It’s also the right moment to shop across multiple insurers, since some companies price certain territories more competitively than others.

When Someone Else Drives Your Car: What Ontario Drivers Get Wrong

If you’re a parent in your 40s or 50s with adult children who sometimes borrow the family vehicle, this section is for you. It’s also one of the most misunderstood parts of Ontario auto insurance.

Ontario recognizes three driver classifications. The listed principal driver uses the vehicle most. The listed occasional driver uses it regularly but less often, such as a spouse or a university student who borrows it during holidays. An unlisted driver is anyone not on the policy. The classification affects your premium, and it can affect whether a claim is paid.

When a listed secondary driver causes a collision, that accident can affect the primary policyholder’s claims history and rating, depending on the insurer and the circumstances. This is one of the most misunderstood parts of family insurance in Ontario. It doesn’t always happen, and the specifics vary by insurer and by how the claim is categorized. But the possibility is real, and it’s worth understanding before you add a young or high-risk driver to your policy.

The risk with unlisted drivers is more direct. If a vehicle is regularly driven by someone not on the policy and a collision occurs, the insurer may deny the claim or reduce the payout, treating the omission as material misrepresentation. All licensed drivers living at the same address must be disclosed, even if they have their own vehicle and separate policy.

Many parents occasionally lend their car to an adult child who lives at home or visits regularly. If this is a recurring pattern, even a few times per month, that adult child may need to be listed as an occasional driver. The line between “occasional use” and “regular unlisted use” isn’t always clear, and insurers don’t draw it the same way. A brief conversation with a broker about your specific situation is the right first step.

If you need to add a young driver and you’re bracing for the premium increase, which industry data suggests can be 41% or more, there are legitimate ways to manage the cost. In a multi-car household, listing the young driver as the primary driver on the lower-value vehicle can help. Accurate classification matters: if they truly are an occasional driver, list them as one. And a telematics program specifically for the young driver can lower their contribution over time. We cover the full telematics approach here: Car Insurance in Ontario: What Actually Lowers Your Premium (2026).

What FSRA Does, and How to Use It If You Have a Problem

The Financial Services Regulatory Authority of Ontario (FSRA) regulates auto insurance in the province. It approves all rate changes, licenses insurers and brokers, and sets the rules for how policies must be written. It doesn’t sell insurance or mediate individual disputes, but it holds insurers accountable for following provincial law.

If you have a complaint, start with the insurer’s own internal complaint handling process. Every licensed Ontario insurer is required to have one. Ask for it in writing when you first raise an issue and document everything. If the insurer can’t resolve your concern, they must provide a final position letter.

Once you have that letter, your next step is the General Insurance OmbudService, known as the GIO. It’s an independent, not-for-profit dispute resolution service that handles complaints about claims, coverage decisions, and broker conduct. It is free for consumers. You can reach them at giocanada.org.

FSRA itself is the appropriate contact when you believe an insurer or broker has broken provincial law or regulation, not simply made a decision you disagree with. If you believe the issue involves regulatory non-compliance, unfair business practices, or unapproved rate changes, you can file a complaint directly with FSRA.

The 10-Question Renewal Checklist

This is the section that ties everything together. Before your next renewal date, sit down with your policy documents and work through these ten questions. You don’t need to answer them all in one sitting.

If even three or four make you pause, you’re not behind. You’re exactly where most Ontario drivers are. The difference is that now you know where to look.

- Have I gotten at least two competing quotes this renewal cycle? Renewal pricing is not automatically the market’s best offer. According to industry data from 2023, shoppers who compared quotes and switched insurers reported average annual savings of $882. Getting quotes from two other insurers or a broker takes less than a day and regularly reveals savings that more than justify the effort.

- When did I last review my deductible amount? Many drivers set their deductible when they first insured their vehicle and never revisit it. If your financial situation has changed since then, whether you have more savings now or less, your deductible level may no longer reflect the right risk-cost balance for your household.

- Am I bundling home and auto with the same provider, and is that combination actually cheaper? Bundling doesn’t always produce the lowest total cost. It’s worth getting a disaggregated quote, pricing home and auto separately from different providers, to confirm the bundle is genuinely saving money rather than just assumed to be.

- Do I have a telematics discount available that I haven’t explored? Telematics programs use a device or smartphone app to track your driving habits and can offer discounts of up to 30% based on how you actually drive.

- Is my vehicle listed at the correct garaging address? This should reflect where the car is kept overnight, not where you work. If you’ve moved or your household situation has changed, this may need to be updated. As we covered in the postal code section above, the garaging address directly determines your territory rating.

- Are all drivers in my household correctly listed on my policy? An unlisted regular driver creates real risk. If someone who lives with you and drives your vehicle regularly isn’t on your policy, a claim involving that person could be denied or reduced. Accurate classification, principal versus occasional, matters just as much as being listed at all.

- Does my vehicle’s current market value still justify carrying collision and comprehensive coverage? If your car’s market value has dropped significantly and you’re still carrying full coverage, you may be paying more in annual premiums than the insurer would ever pay out. For a practical way to think through this calculation, see: Car Insurance in Ontario: What Actually Lowers Your Premium (2026).

- Am I carrying the Family Protection endorsement (OPCF 44R)? This is one of the highest-value, lowest-cost endorsements available in Ontario. If the answer is no or “I’m not sure,” it’s worth a five-minute conversation with a broker. The annual cost is nominal, and the protection it provides against underinsured and uninsured drivers is substantial.

- Do I understand which of my Statutory Accident Benefits will become optional on July 1, 2026, and have I made a decision about what to keep? Benefits like income replacement, caregiver support, and death and funeral coverage are moving from mandatory to optional. The estimated savings for opting out are roughly $100 per year total, while the potential loss runs into tens of thousands. We explain exactly what is changing and why here: Why Your Ontario Car Insurance Went Up Again in 2026.

- Have I asked specifically about group or alumni discounts through my employer, union, or professional associations? These discounts exist at many insurers but are rarely volunteered. You almost always have to ask about them directly. A two-minute question during your next renewal call could save a meaningful amount.

What to Ask Before You Renew

- Before accepting your renewal, ask:

- “Can you show me what changes if I raise or lower my deductible?”

- “Do I have OPCF 44R on this policy?”

- “Are all household drivers correctly listed?”

- “Is my garaging address correct?”

- “Are there group, alumni, employer, or telematics discounts available?”

If you answered “I’m not sure” to more than three of these, a conversation with a RIBO-registered broker is overdue. For a full guide to what each of these levers does and what they typically save, see our detailed premium-lowering breakdown: Car Insurance in Ontario: What Actually Lowers Your Premium (2026).

Key Facts: Ontario Car Insurance 2026

- Ontario average annual premium: $2,164 (October 2025), source: FSRA

- GTA average vs rest of Ontario gap: approximately $1,070 per year (GTA average $2,810 vs rural Ontario average $1,740), source: FSRA

- FSRA approves all Ontario rate changes. Filings are based on claims data from 12 to 24 months prior.

- July 1, 2026: Ontario statutory accident benefits restructured from a mandatory bundle to a modular opt-in system, source: FSRA

- RIBO registers all Ontario insurance brokers. Verify any broker at ribo.com.

- Family Protection endorsement (OPCF 44R): a nominal annual cost, widely considered the highest-value add-on in Ontario relative to its price

Frequently Asked Questions

Tariq still has the same car. He still lives in North York. But the next time his renewal arrived, he read the declarations page first. He checked his endorsement codes against the list he’d bookmarked. He called a RIBO-registered broker and asked three questions he’d never thought to ask before. The premium didn’t magically halve. But for the first time in fourteen years, he understood what he was paying for, and he could explain it to Amira at dinner without hesitating. That clarity won’t make the bill smaller on its own. But it’s the thing that makes every other decision possible.

What is an Ontario insurance survival guide?

An Ontario insurance survival guide is a plain-language resource that helps drivers understand what their auto insurance policy covers, how the system works, and what decisions to make at renewal time, without requiring any prior insurance knowledge.

How do I lower my car insurance in Ontario in 2026?

The most effective strategies include comparing quotes from multiple insurers or through a RIBO broker, reviewing your deductible, confirming your garaging address is correct, and checking whether you qualify for group or telematics discounts. For the complete breakdown of every tactic that actually works, including specific savings ranges for each one, see our full guide: Car Insurance in Ontario: What Actually Lowers Your Premium (2026).

Why is car insurance so expensive in Ontario?

Ontario premiums are driven by a combination of rising repair costs, high auto theft rates in urban corridors, increasing healthcare expenses, and a regulatory system where approved rate changes are based on claims data from 12 to 24 months earlier. For the full structural explanation of why car insurance is so expensive in Ontario, including repair costs, theft data, and the built-in delay in rate approvals, see our full guide.

What is the minimum car insurance required in Ontario?

The mandatory minimum in Ontario includes four coverages: Third Party Liability at $200,000, Statutory Accident Benefits, Direct Compensation Property Damage, and Uninsured Automobile Coverage. While $200,000 in Third Party Liability is the legal minimum, most insurance professionals recommend carrying $1 million to $2 million because modern court awards regularly exceed $200,000 by a wide margin.

How do I file a complaint about my car insurance in Ontario?

Start with your insurer’s internal complaint handling process; they must issue a final position letter if unresolved. Then escalate to the General Insurance OmbudService at giocanada.org, which provides free, independent dispute resolution for contract and claims disputes. If you believe provincial law has been broken, contact FSRA directly at fsrao.ca/submit-complaint-fsra.

What does a car insurance broker do in Ontario?

A broker represents multiple insurance companies, is regulated by the Registered Insurance Brokers of Ontario (RIBO), and has a legal duty to find a product suitable for the client. Unlike a direct insurer agent who sells for one company, a broker can compare across the market. Verify any broker’s registration at ribo.com.

What is OPCF 44R?

OPCF 44R is the Family Protection endorsement in Ontario auto insurance. It extends your own policy’s liability limits to protect you and your family if you’re hit by a driver who is uninsured or carries insufficient liability coverage. Its annual cost is nominal, often described as less than the daily price of a cup of coffee, and it fills one of the most significant gaps in the standard Ontario policy.

Why is car insurance so expensive in Ontario for new drivers?

New drivers statistically have higher collision rates, which insurers reflect in higher base premiums. Adding a young occasional driver under 25 can increase household premiums by 41% or more (industry data). The rate drops with each clean year of driving history. For practical steps to reduce new driver premiums in Ontario, see: Car Insurance in Ontario: What Actually Lowers Your Premium (2026).

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.