Private Health Insurance in Canada For Families Without Workplace Benefits

Quick Answer: Is Private Health Insurance Worth It Without Workplace Benefits?

For Canadian families without workplace benefits, private health insurance may help when the household has recurring prescriptions, ongoing dental needs, therapy or paramedical appointments, children’s health expenses, or very limited savings to absorb a surprise bill.

It may be less useful when premiums are high relative to what the family actually spends on health care, when annual limits and co-payments reduce the real payout, or when public programs like the Canada Dental Care Plan or provincial drug coverage already reduce the risk.

The right answer depends on the family’s actual health spending, not on fear alone.

🎧 Pressed for time? This summary covers the private health insurance for families without workplace benefits.

Leila closes the kids’ bedroom door and walks back to the kitchen table. The house is finally quiet. Her laptop is open to a private health insurance quote, and beside it sits a dentist’s treatment plan for her seven-year-old, a receipt for her own eye exam, and a pharmacy printout for her husband Omar’s blood pressure medication. None of those costs is being softened by an employer benefits plan. No employer plan, no group benefits, no dental card tucked into a wallet.

Leila runs a small bookkeeping practice from home in Kitchener. Omar picks up contract carpentry work. They file taxes, pay into the system, and take their kids to the doctor when they need to. The big stuff, the hospital visits and the walk-in clinic appointments, those are covered by OHIP. It’s everything else that adds up quietly.

The insurance quote on her screen says $287 a month. That’s $3,444 a year. For a family already watching every dollar, that number needs to justify itself. And tonight, Leila isn’t sure it can.

This is where a lot of Canadian families find themselves when they start looking at private health insurance in Canada for families without workplace benefits. Not panicking over surgery bills, but quietly doing math on dental cleanings, new glasses, prescription refills, and therapy appointments, wondering whether paying a monthly premium will actually protect them or just become one more fixed cost that’s hard to cancel.

Why does public healthcare in Canada still leave families with bills?

Canada’s public health system covers medically necessary hospital and physician services. If your child breaks an arm, you go to the emergency room and you don’t get a bill. Many medically necessary tests ordered by a doctor are covered, depending on the province and setting. That part works.

What catches families off guard is everything outside that boundary. Dental care, prescription drugs, eyeglasses, contact lenses, physiotherapy, massage therapy, mental health counselling, ambulance fees, and private or semi-private hospital rooms generally fall outside basic provincial health coverage. These aren’t luxuries. For most households, they’re regular costs that show up two, three, or four times a year.

Coverage also varies by province. Ontario covers annual eye exams for children under 20 and adults over 65 through OHIP, but working-age adults pay out of pocket. British Columbia’s MSP does not cover routine dental or optical care. Quebec requires every resident to carry prescription drug coverage, either through a private group plan or the public RAMQ plan. Alberta offers a provincial Non-Group Coverage program administered by Alberta Blue Cross. The patchwork matters, because where you live changes what you’re exposed to.

On April 1, 2026, a new federal policy under the Canada Health Act took effect. Under the CHA Services Policy, patient charges for medically necessary services provided by nurse practitioners, pharmacists, or midwives will be treated as extra-billing when those same services would be covered if delivered by a physician. The policy does not expand the basket of insured services. It is designed to prevent patients from being charged for care that should already be covered. That is a meaningful step. But it does not close the gap on prescriptions, dental work, glasses, or therapy.

How many Canadian families are missing workplace health benefits?

According to Statistics Canada, 66.8% of Canadian employees had access to workplace medical or dental benefits through their main job in 2024. For full-time workers, that number was 76.1%. For part-time employees, it dropped to 20.7%.

Those numbers tell a clear story. If you work full-time for a mid-size or large employer, benefits probably came with the job. But if you’re self-employed, working contracts, picking up part-time shifts, or running a small business, there’s a strong chance you have no group coverage at all.

For families like Leila and Omar’s, losing access to employer benefits, or never having them in the first place, makes visible every health cost that a workplace plan would have quietly absorbed. The dental cleaning, the kid’s cavity filling, the new prescription, the physiotherapy session after a back injury. These were never free. They were just hidden inside someone else’s compensation package.

Self-employed readers can also read our separate guide to personal health insurance Canada for self-employed workers before comparing premiums, tax rules, and self-funding.

What does private health insurance actually cover in Canada?

Private health insurance Canada plans typically offer some combination of prescription drug coverage, dental care, vision care, paramedical services like physiotherapy, massage therapy, and mental health counselling, ambulance fees, hospital room upgrades, and emergency travel medical coverage. Family plans usually include dependent children.

The key word is “some.” Coverage does not mean full reimbursement. Most plans apply annual limits per category, co-payments where the family pays a percentage of each claim, and deductibles that must be met before the plan starts paying. A dental plan might cover 70% of a cleaning but cap total dental claims at $500 or $750 a year. A drug plan might reimburse 80% of a prescription but only up to $1,500 annually.

Reading the plan details matters more than reading the marketing.

What is the difference between private health insurance and extended health benefits?

These terms show up everywhere when families start researching: private medical insurance, personal health insurance, supplemental health insurance, extended health benefits. They mostly describe the same thing, coverage for health costs not included in your provincial plan.

“Extended health benefits” usually refers to coverage provided through an employer as part of a compensation package. “Private health insurance” or “supplemental health insurance” typically means a plan purchased individually or as a family on the open market. “Family health insurance Canada” can mean either, depending on context.

The label matters less than the details. What does the plan actually pay for? What does it exclude? What are the annual caps? That is the real question, regardless of what the plan is called.

Are monthly premiums actually worth it for most families?

This is where the math gets uncomfortable, and it’s the part families like Leila’s wrestle with most.

A monthly premium is a fixed cost. It leaves the household budget every month whether the family uses the plan or not. Claims, on the other hand, are uncertain.

A healthy family might go through an entire year using only routine dental cleanings, a couple of prescriptions, and one eye exam. In that scenario, the total value of the claims may be well below what the family paid in premiums.

Consider a family paying around $250 to $300 a month for a standard plan. That’s roughly $3,000 to $3,600 a year. If the plan caps dental at $750 per person, drug coverage at $1,500, and vision at $200 every two years, the maximum the family could possibly claim in a routine year might not come close to what they’ve paid.

On the other hand, a family with one member on an expensive maintenance medication, two kids needing orthodontic assessments, and a parent attending regular physiotherapy could easily exceed what they pay in premiums. The math shifts depending on the household’s actual health needs.

Private insurance can help some families. But it does not automatically pay back more than it costs. The value depends on the family’s likely claims, annual limits, exclusions, and whether the plan truly reduces financial exposure or simply spreads it into monthly instalments.

What Families Should Check Before Buying

Annual limits

A plan may list a category as “covered,” but coverage might be capped at a modest yearly maximum. A $500 annual dental cap won’t cover much beyond two cleanings and a filling.

Deductibles and Co-Payments’

Some plans require the family to pay a deductible before coverage kicks in. After that, the insurer may cover only 70% or 80% of the cost, leaving the family responsible for the rest.

Waiting periods

Dental coverage, major dental work, and some paramedical categories may have waiting periods of several months before claims are accepted. A family buying insurance to cover an upcoming procedure may find it isn’t covered right away.

Pre-existing conditions

Plans purchased on the open market may exclude conditions that existed before the policy started, or they may apply a higher premium. Families leaving an employer plan should ask about conversion options within the typical 60-to-90-day window after group benefits end, as conversion plans often waive medical underwriting.

Dental and prescription caps

These are the categories families claim most often, and they’re usually the most tightly capped. A plan with a $500 dental maximum per person and a $1,000 drug cap may not cover much beyond the basics.

Children’s coverage

Most family plans cover dependent children, but age limits vary. Some plans cover dependents up to age 21 or 25 if they are full-time students. Families should confirm the cut-off.

Cancellation and renewal rules

Understand how to cancel, whether premiums increase at renewal, and whether the insurer can change coverage terms from year to year.

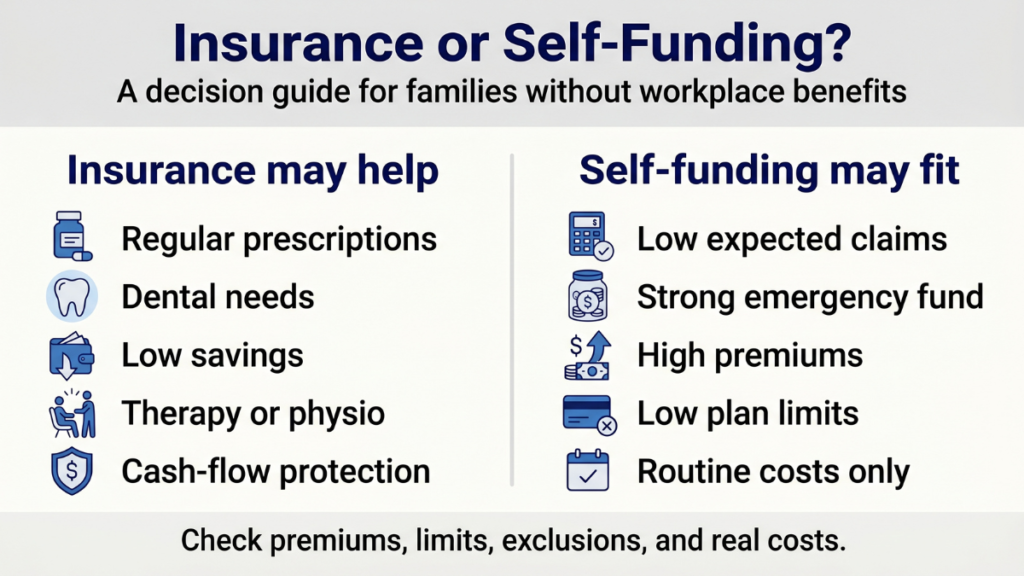

Should families self-fund health costs or buy private insurance?

| Family situation | Private insurance may help when | Self-funding may work when |

|---|---|---|

| Regular prescriptions | Medication costs are high and predictable | Prescriptions are occasional and inexpensive |

| Children’s dental needs | Multiple children need ongoing dental work | Dental needs are limited to routine cleanings |

| Low expected claims | The family wants cash-flow smoothing | Annual premiums exceed likely claims |

| Limited emergency savings | A surprise $2,000 dental bill would be a crisis | The family can absorb a moderate unexpected bill |

| Therapy or paramedical care | A family member attends regular sessions | Sessions are occasional or short-term |

| High premiums with low limits | May not provide enough value | May be worth comparing carefully |

This isn’t about being clever with money or gambling on health. It’s about matching the tool to the household’s real situation. A family with predictable, recurring costs may get genuine value from a well-chosen plan. A healthy family with modest needs may do better setting aside those premium dollars into a dedicated savings account and paying providers directly. If the money is being kept for near-term health costs, it should stay accessible rather than being treated like long-term savings.

What public programs should families check before buying private insurance?

Before spending on private coverage, families should check what public programs already reduce their risk.

Canada Dental Care Plan (CDCP)

The federal CDCP provides dental coverage for Canadian residents with an adjusted family net income under $90,000 who do not have access to dental insurance. Families with income under $70,000 pay no co-payment on covered services. Those earning between $70,000 and $89,999 pay a co-payment of 40% or 60%, depending on income. Having access to private dental insurance can make a household ineligible for the CDCP, so families should check the official rules before buying dental coverage. Before buying private dental coverage, families should check the Canada Dental Plan eligibility rules.

Provincial drug programs

Most provinces offer income-based prescription drug programs that can significantly reduce out-of-pocket costs. Ontario’s Trillium Drug Program, British Columbia’s Fair PharmaCare, Alberta’s Non-Group Coverage through Alberta Blue Cross, and Quebec’s RAMQ prescription drug insurance each work differently, but all provide some level of support for families without private drug coverage. Eligibility rules, deductibles, and co-payment structures vary by province. Families should check their own province’s program before purchasing private prescription coverage.

Ontario families can read our separate guide to private health insurance Ontario for families without workplace benefits before comparing premiums and public programs.

Medical Expense Tax Credit

The CRA allows families to claim eligible medical expenses, including out-of-pocket health costs and private insurance premiums, on their tax return. The credit applies to expenses exceeding the lesser of 3% of the lower-income spouse’s net income or the federally indexed threshold $2,834 for 2025 and $2,890 for 2026. Families can choose any 12-month period ending in the tax year, which allows grouping of expenses across calendar years.

Some self-employed individuals may be able to deduct eligible private health services plan premiums as a business expense, depending on their situation. This should be checked against CRA rules or with a tax professional. The CRA medical expenses guide explains which eligible medical expenses may be claimed and how the threshold works.

Spouse’s workplace benefits

If one partner has access to benefits through an employer, even partial coverage, this should be explored before purchasing a separate plan.

What should newcomer families know about health coverage gaps in Canada?

Newcomer families should not assume provincial health coverage starts on the day they arrive. Some provinces enforce a waiting period of up to three months before a new resident’s health card is activated. During that gap, routine physician visits, lab tests, and non-emergency care may not be covered.

For some international newcomers, public health coverage may not begin immediately, depending on the province, immigration status, and eligibility rules. In that situation, a short-term emergency medical or travel insurance policy, sometimes called a “Visitors to Canada” policy, can protect against catastrophic hospital costs during the transition. This is different from routine dental and vision insurance, which is unlikely to provide much value over a short coverage gap.

Each province handles this differently, so newcomer families should check the rules for the specific province where they plan to settle.

Before arrival, families may also want to review basic banking setup, because health coverage, emergency savings, and first-month settlement costs often land at the same time.

The Emotional Side of Buying Insurance

What doesn’t show up in the math is the weight of the decision. Families without workplace benefits carry a specific kind of anxiety. It’s the worry that one dental bill will throw off the month. It’s the frustration of paying a premium every month and then discovering the plan won’t cover what you actually need. It’s the guilt of putting off your own glasses because the kids’ teeth come first.

For self-employed families, contract workers, and gig workers, there’s also the feeling of being outside a system that seems designed for people with stable, full-time jobs. When your neighbour’s employer covers 80% of their dental and drug costs and you’re covering 100% of yours, it’s hard not to feel like you’ve fallen through a crack.

Leila felt this sitting at her kitchen table. The insurance quote wasn’t just a number. It was a question about whether her family could afford to be protected, and whether “protection” would actually protect them.

That feeling is real. And it’s shared by a lot of Canadian households right now.

Key Facts: Private Health Insurance In Canada

- In 2024, 66.8% of Canadian employees had access to workplace medical or dental benefits through their main job, according to Statistics Canada. Only 20.7% of part-time employees had similar access.

- Canada’s public healthcare system generally covers medically necessary hospital and physician services, but dental care, prescription drugs, vision, therapy, and many paramedical services are not included in basic provincial coverage.

- The Canada Dental Care Plan provides dental coverage for residents with adjusted family net income under $90,000 who do not have access to dental insurance. Having active private dental insurance disqualifies a household from the program.

- Private health insurance plans may include premiums, deductibles, co-payments, annual limits, waiting periods, and exclusions that reduce the real value of coverage.

- Provincial drug programs such as Ontario’s Trillium Drug Program, BC’s Fair PharmaCare, Alberta’s Non-Group Coverage, and Quebec’s RAMQ plan offer income-based prescription support.

- Some provinces may have waiting periods or different eligibility rules before provincial health coverage begins for new residents.

A Practical Checklist Before Paying

- List your family’s health expenses from the past 12 to 24 months, including dental, prescriptions, vision, therapy, and paramedical visits.

- Add up what you actually spent out of pocket.

- Get a quote for a private plan and compare the annual premium to your likely annual claims.

- Check the annual limits for each coverage category, especially dental and prescriptions.

- Check for waiting periods on dental, major dental, and other services.

- Review the pre-existing condition rules carefully.

- Confirm whether buying private dental insurance would disqualify your family from the Canada Dental Care Plan.

- Check whether your province offers an income-tested drug program that already covers your prescriptions.

- Check whether a spouse or partner has access to workplace benefits, even partial.

- Consider whether a dedicated health savings fund in a high-interest savings account might cover your routine costs more efficiently.

Closing: Protection Should Still Make Sense

Leila is still at the kitchen table. The insurance quote is still open. But now she’s also pulled up the Canada Dental Care Plan eligibility page, her province’s drug assistance program, and a spreadsheet where she’s been adding up the family’s actual health costs from the past year.

The number she lands on is smaller than the premium quote. Not dramatically smaller, but enough to make her pause. Enough to make her wonder whether a dedicated savings account, combined with the public programs her family already qualifies for, might do more than a plan with $500 dental caps and a six-month waiting period on major work.

Private health insurance in Canada for families without workplace benefits can be a useful tool. But it should be bought because the numbers support it, not because the anxiety demands it. The right choice is the one that fits the family’s real expenses, their cash flow, the public programs they’re eligible for, and their comfort with absorbing a surprise bill.

A family without workplace benefits isn’t careless. They’re simply facing costs that most workplace plans quietly absorb. Making those costs visible, understanding what’s actually at risk, and choosing the response that fits the household’s real life: that’s not a compromise. That’s good financial thinking.

Frequently Asked Questions

Is private health insurance worth it in Canada for families without workplace benefits?

It depends on the family’s actual health spending. Families with recurring prescriptions, ongoing dental needs, therapy costs, or limited savings may benefit. Families with modest, predictable health expenses and access to public programs may find that self-funding is more cost-effective.

What does private health insurance cover in Canada?

Most private plans cover some combination of prescription drugs, dental care, vision care, paramedical services like physiotherapy and massage, mental health counselling, ambulance fees, and hospital room upgrades. Coverage levels, annual limits, and exclusions vary by plan.

What is the difference between private health insurance and extended health benefits?

Extended health benefits usually refer to coverage provided through an employer as part of a compensation package. Private health insurance refers to plans purchased individually on the open market. The coverage categories can be similar, but employer plans are typically more generous because they benefit from group pricing and risk pooling.

Do Canadian families need private health insurance if healthcare is public?

Public healthcare covers hospital stays and physician services, but not dental, prescriptions, glasses, therapy, or most paramedical care. Many families face real out-of-pocket costs in these areas. Whether private insurance is the right way to manage those costs depends on the household’s situation.

How much does private health insurance cost in Canada for a family?

Premiums vary widely depending on the plan, the insurer, the family’s age, location, and health history. As a general reference, basic individual plans may start around $100 to $175 per month, while more comprehensive family plans can run $250 to $450 or more. These ranges are based on publicly available quote examples gathered in 2025 and 2026 and should be treated as rough estimates. Families should request quotes from multiple insurers based on their own details.

Does private health insurance cover dental and prescriptions?

Most plans include dental and prescription drug coverage, but with annual caps, co-payments, and waiting periods. A dental plan might cover 70% of a cleaning up to a $500 or $750 yearly maximum. A drug plan might reimburse 80% of a prescription up to an annual limit. Families should read the plan details carefully.

Can self-employed workers get health insurance in Canada?

Yes. Self-employed workers can purchase individual or family health insurance plans on the open market. Premiums may also be deductible as a business expense or claimable under the Medical Expense Tax Credit. Self-employed workers should also check provincial drug programs and the Canada Dental Care Plan before purchasing.

What should families check before buying private health insurance?

Annual limits by category, deductibles, co-payment percentages, waiting periods, pre-existing condition exclusions, dependent age limits, cancellation terms, and whether buying the plan affects eligibility for public programs like the Canada Dental Care Plan.

Can private health insurance affect Canada Dental Care Plan eligibility?

Yes. The CDCP requires that applicants have no access to dental insurance. Purchasing a private plan with dental coverage, even a basic one, disqualifies the household from the federal program. Families with adjusted net income under $90,000 should check CDCP eligibility before buying private dental coverage.

Should newcomer families buy private health insurance before provincial coverage starts?

Newcomer families should confirm the rules for the specific province where they are settling. Some provinces have a waiting period of up to three months. During that gap, a short-term emergency medical policy may be more appropriate and cost-effective than a full retail health and dental plan. Routine dental and vision insurance is unlikely to provide significant value during a short coverage gap.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial, legal, tax, or investment advice. Individual circumstances vary, so please use your own judgment and consult a qualified professional when appropriate.